Buy this stock tomorrow

Cintas Keeps Beating Expectations—And the Story Isn’t OverWritten by Thomas Hughes on July 16, 2026

Key Points

- Cintas reported a beat-and-raise quarter on July 15, with revenue up 9% to $2.91 billion and adjusted EPS growing 18.3%.

- The pending Unifirst acquisition awaits FTC approval and could serve as either a growth catalyst or a setback, leaving Cintas to keep gaining market share on its own.

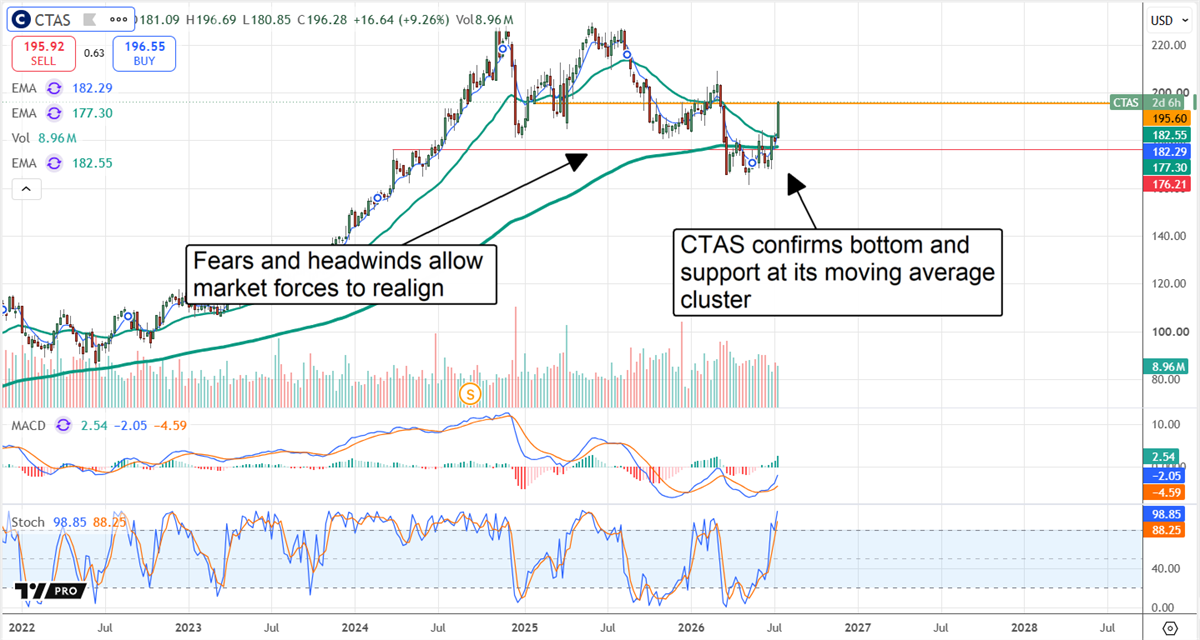

- Institutions own 63% of CTAS shares and have been buying aggressively, while price charts suggest the stock has bottomed and could retest all-time highs within a year.

- Special Report: My top 3 AI picks for the next decade

Cintas (NASDAQ: CTAS) share price isn’t low, trading at 37x current-year earnings, approximately 65% more expensive than the average S&P 500 company, but this is about as cheap as it's going to get. While valid concerns have weighed on the share price, fears about the Unifirst (NYSE: UNF) acquisition, regulatory scrutiny, and energy cost headwinds have failed to derail the business. Cintas is the leading player in uniform services, outperforming in fiscal year 2026 and on track to sustain strength in 2027. Unifirst could be both a hurdle and a catalyst this year. UNF shareholders have approved the merger, but the Federal Trade Commission has not. On the one hand, the merger would enable numerous proven synergies that Cintas has unlocked through past acquisitions, while expanding its footprint and cross-selling opportunities—good for growth and margin. On the other hand, a blocked deal would mean Cintas can continue chugging along as it is, outpacing competitors, gobbling up market share, driving cash flow, and returning capital to its investors—good for its share price.

Financial forecaster Porter Stansberry says Trump is planning to replace the U.S. dollar - not with crypto or gold, but something far more unusual. He claims the reset is already backed by a coalition of 13 nations and signed without Congress.

The last time America went through a monetary shift like this, in 1974, it triggered decade-long gains of 6,000%, 9,700%, and 14,400% in the companies best positioned for it. Porter has identified a specific group of stocks he believes sit at the center of this one.

He's releasing a free broadcast that includes the name and ticker of one asset with immediate exposure to what's unfolding. Watch Porter Stansberry's free broadcast and get the ticker now

Cintas Advances After Beat-and-Raise QuarterCintas reported another fantastic quarter on July 15, with revenue and earnings outperforming expectations despite the impact of acquisition-related expenses. Revenue grew by 9% to $2.91 billion, outpacing the consensus by approximately 140 basis points. Strength was underpinned by the core Uniform Services segment, which grew by 8.2%, and driven by the Other segment, which grew by more than 11%. The Other segment includes safety, fire, and first aid, all high-margin cross-sells and upsells. Margin news was also good. The company widened its gross and operating margins, increasing gross margin by 11.6% and operating margin by 12.7%, leaving earnings up at more than double the pace of revenue growth. Adjusted earnings per share (EPS) increased by 18.3%, outperforming by 5 cents, including the 3-cent impact from acquisition expenses. More importantly, full-year cash flow came in at $2.28 billion, more than 5% year-over-year (YOY) and sufficient to cover capital expenditure and acquisition costs while paying the dividend. Cintas' fiscal year-end balance sheet highlights reflected the strength of its model and position. Current and total assets were up on cash, receivables, and inventory, while long-term debt and liabilities declined, dividends were paid, and shares were bought back. The net result was a 9.7% increase in equity and a 1% YOY reduction in share count, with a dividend yield of about 1%. The takeaway is that CTAS shares paid 1%, while investors gained 1% in share-count leverage and nearly 10% in equity, metrics that underpin share-price increases over time. Analysts and Institutions Show Confidence in CTAS's Long-Term PotentialCintas’ Q4 results and guidance update may not inspire a robust round of analyst revisions, but it should be enough to end the downtrend in price targets. The downtrend aided the fall in share prices and masked an otherwise favorable market. The current analyst consensus is Hold, not surprising given the execution risks involved with the Unifirst merger, and price targets suggest modest upside from recent lows. The opportunity is that analyst sentiment will unstick in the upcoming quarters, triggering more bullish activity in the market. Institutions, on the other hand, are more actively bullish than the analyst trends suggest. The group owns a considerable 63% of the stock and has been buying aggressively over the trailing 12 months. Activity was subdued ahead of the release but reflected a robustly bullish market, with them accumulating at a $4-to-$1 pace. The likely outcome is that, given the low price and technical setup, institutions will continue to accumulate CTAS shares and limit downside risk.

The charts suggest that CTAS hit a bottom over the past year and is in a rebound mode as of mid-2026. Price action moved above critical support ahead of the release and then accelerated in its wake, showing support at a cluster of exponential moving averages (EMAs), including both long- and short-term indicators. Market forces are bullishly aligned, with the price positioned to sustain a rally over the coming quarters. In this scenario, CTAS is on track to retest the existing all-time high within the next 12 months and potentially continue higher afterward. Fundamentally, Cintas is perfectly positioned to benefit from economic tailwinds. This year’s labor market data isn’t robust but reveals growth and stability, including improvements in total jobless claims that point to uniform and services demand. With labor markets underpinned by business investment, deregulation, and favorable tax policies (as recently indicated by JPMorgan CEO Jamie Dimon), Cintas’ business will remain healthy in upcoming quarters and may even accelerate. Read this article online › Featured Articles

Did you find this article useful?

|

No comments:

Post a Comment