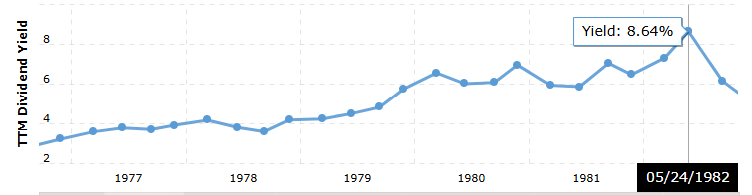

Back in the day, you could park your cash in a stock and yield hefty 8% dividend checks…

Giving you capital gains and cash flow to offset rising costs.

A standard $250k retirement account would’ve seen healthy market returns.

But in today’s market… you’re lucky to get much more than 1% in dividends.

So chasing dividends might look like a dead game… if you don’t know a smarter way to find solid stocks.

Picking the right stocks keeps you on the right track…

And gives you more shots to reap returns over time.

That’s why I had to get these 5 dividend-investing cheat sheets to you.

After more than a decade trading the markets, and having contacts which include a former hedge fund manager, a trading champion, and a former bank VP…

I believe everything you’ll see inside will give you a special look at how to go after dividend stocks.

You’ll get to see every single detail I look for before I even touch any stock for dividends…

In fact, you’ll get the two dividend stocks I personally put $50,000 of my own money into.

No reckless guarantees when it comes to trading, of course.

But before you load up on another dividend stock next…

Check out these cheat sheets… free.

By clicking the link above you agree to periodic updates from ProsperityPub and its partners (privacy policy)

Nebius' 1.2 GW Win: A $20B Bet on AI Infrastructure

By Jeffrey Neal Johnson. Published: 3/5/2026.

Key Points

- The approval of a new AI factory represents a pivotal milestone for Nebius, positioning the company as a key enabler for the entire AI ecosystem.

- This major infrastructure project directly supports the company's aggressive growth targets by meeting the overwhelming and secured customer demand for AI compute.

- This landmark project validates the company's focused strategy on AI infrastructure, earning positive notice and strong price targets from Wall Street analysts.

- Special Report: [Sponsorship-Ad-6-Format3]

Shares of Nebius Group (NASDAQ: NBIS) have risen sharply after a major announcement that cements the company's high‑stakes pivot into the center of the artificial intelligence (AI) boom.

The company has secured approval to build a large AI factory in the United States — a project with power capacity comparable to some of the world's biggest data centers. This development is more than a construction effort; it is the foundation of a new corporate identity and a strong validation of Nebius's strategy to become an essential provider of global AI infrastructure.

Missouri Milestone: Powering a Strategic Pivot

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

At the center of this plan is a 400-acre campus in Independence, Missouri, which is expected to create more than 1,300 local jobs. The most important figure for investors, however, is the facility's potential power capacity: up to 1.2 gigawatts (GW). In an industry measured by computing power, access to electricity at this scale is a strategic breakthrough — 1.2 GW is enough energy to run a large city.

For AI, electricity is the most critical and scarce resource. Over the past year the conversation has centered on high-powered GPUs, and as chip supplies begin to normalize, a new bottleneck has emerged: the physical space and massive electrical infrastructure required to operate those chips. Companies can develop the best algorithms, but without large, reliable power sources their ambitions stall. By securing this capacity, Nebius has captured a central piece of the infrastructure puzzle and positioned itself as a key enabler for the broader AI ecosystem.

This Missouri factory is the flagship of the new Nebius. The company has transitioned from its prior identity as the diversified tech conglomerate Yandex N.V. into a focused, pure‑play AI infrastructure provider, concentrating resources on what it views as the market's largest opportunity. This tangible, real‑world project is a clear proof point of that strategic shift.

From Power to Profit

Investors will want to know how this infrastructure investment converts into financial growth. The answer lies in the pronounced supply-and-demand imbalance in the AI computing market. During its fourth-quarter 2025 earnings call, Nebius management disclosed that available computing capacity was sold out for months, with customers committing to longer-term contracts at attractive prices to secure resources.

Building and powering new data centers is therefore the most direct path to revenue. Nebius has guided to an annualized revenue run rate (ARR) of $7 billion to $9 billion by the end of 2026. ARR extrapolates current monthly recurring revenue over a year and gives a forward-looking view of scale; reaching this target depends on bringing the new capacity online.

The expansion requires sizable capital: Nebius outlined a 2026 capital expenditure plan of $16 billion to $20 billion. About 60% of that funding is already secured through cash on hand, operating cash flow, and upfront payments from long-term customer agreements. With a strong balance sheet and limited existing debt, the company is positioned to finance the remainder of the build without taking on excessive risk. This appears to be a calculated expansion supported by confirmed customer demand rather than a speculative bet.

A Clear Runway for Growth

The Missouri approval is a major de‑risking event for Nebius. What was once a plan on a spreadsheet is now a tangible project with government and community backing, giving investors a visible milestone to monitor. It validates the company's aggressive strategy to establish a leadership role in high-demand AI infrastructure.

Wall Street has taken notice. The stock currently carries a Moderate Buy consensus rating from analysts, with an average price target of $143.22. That suggests significant upside from current levels and reflects confidence in the company's growth trajectory. Analyst targets range from $84 to $211, indicating differing views but a clear bullish case for substantial appreciation. The company's technology assets — including autonomous vehicle developer Avride and EdTech platform TripleTen — also provide a diversified foundation.

With its strategy validated and capacity expansion now underway, investor attention will naturally turn to execution. This landmark project gives Nebius a clear runway to move from participant to a critical pillar of the global AI infrastructure landscape.

Nebius' AI Infrastructure Rally Is Back—And the Numbers Explain Why

By Ryan Hasson. Published: 2/20/2026.

Key Points

- Nebius shares have gained more than 20% over the prior week as accelerating demand and raised contracted power guidance boosted investor confidence.

- Management reaffirmed its ambitious $7 to $9 billion ARR target for 2026, highlighting strong pricing power and long-term customer commitments.

- With analysts lifting price targets and the stock reclaiming $100, NBIS is approaching a key resistance level that could trigger a fresh breakout.

- Special Report: [Sponsorship-Ad-6-Format3]

Nebius Group (NASDAQ: NBIS) has quickly emerged as one of the market's standout performers in AI infrastructure. Shares have surged more than 21% over the past week, driven by confident forward guidance, a wave of bullish analyst upgrades and BlackRock's large stake in the company.

Just two weeks ago, the stock was testing a major support level and looked to be losing momentum. Now, after its latest earnings catalyst, Nebius is pressing up against key resistance and flirting with a potential breakout.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

With improving fundamentals and strengthening technicals, the company is increasingly positioning itself as a potential leader in the AI infrastructure space.

Shares Climb After Q4 Results

Nebius reported fourth-quarter 2025 results on Feb. 12. The headline figures looked mixed at first glance.

Revenue was $227.7 million, below estimates of $246 million, but still represented 547% year-over-year growth and 55% sequential growth. Gross margins remained strong at 70% (versus 71% in the prior quarter). Adjusted EBITDA came in at $15 million versus expectations of $40.4 million, while adjusted EBITDA margin for the core business improved to 24% from 19% in Q3. EPS was negative $0.69, missing consensus of negative $0.42.

The revenue shortfall initially raised eyebrows, but management provided important context.

Management explained that most of the new capacity came online in late November and thus contributed meaningfully only in December. That timing caused the quarter to lag consensus, but forward indicators paint a different picture.

Active power reached 170 MW, well above the previously guided 100 MW. Year-end annual recurring revenue (ARR) climbed to $1.25 billion, up 127% quarter-over-quarter. Management reiterated its ambitious year-end 2026 ARR target of $7 billion to $9 billion, signaling sustained confidence in demand.

Revenue guidance for 2026 was set at $3 billion to $3.4 billion, described as a prudent range. The company also reaffirmed its year-end 2026 connected power target of 800 MW to 1 GW and raised its contracted power guidance from more than 2.5 GW to over 3 GW.

AI Demand Accelerating, Not Slowing

On the earnings call, management emphasized that demand remains robust.

Enterprise and AI-native customers continue to outpace available supply, allowing Nebius to sell future capacity well in advance. In Q4 the company reported nearly twice as many transactions for contracts longer than 12 months compared with Q3, while average selling prices rose by more than 50%.

Management also said the company has effectively sold out of Hoppers, and renewal contracts are extending 12 months or longer at improved pricing. Those longer-term commitments and higher prices point to strengthening pricing power rather than weakening demand.

Analysts Turn More Bullish

On Feb. 18, Compass Point initiated coverage with a Buy rating and a $150 price target, implying roughly 54% upside at the time. A day earlier, BWS Financial reiterated a Buy rating and $130 price target, citing meaningful upside potential.

Both calls treated the Q4 misses as timing-related rather than demand-related, arguing that power and ARR targets are the primary drivers of the 2026 thesis. If Nebius continues converting contracted power into connected power on schedule, analysts' upside cases will be easier to defend.

Nebius now carries 11 analyst ratings, a consensus Moderate Buy, and an average price target of $143.33 — still implying considerable upside despite the stock's roughly 140% gain over the past year.

Impressive Relative Strength and Breakout Potential

While many software and AI-related names have struggled recently, Nebius has bucked the trend. Shares are up roughly 28% year to date and have reclaimed the $100 level.

If the stock can hold above $100 and build support, the next key level is the $110 resistance zone. A sustained move above that area could trigger a breakout and mark the start of another leg higher within its broader uptrend.

This email communication is a sponsored message for ProsperityPub, a third-party advertiser of MarketBeat. Why did I get this message?.

If you have questions about your subscription, please email MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Pl. #620, Sioux Falls, South Dakota 57103-7078. United States..

No comments:

Post a Comment