Sponsored content from Huge Alerts

Gold and Copper Surges Signal a Rare U.S. Mining Opportunity: Fully Permitted CK Gold Project Positions USAU for Explosive Growth with H.C. Wainwright’s $27.50 Price Target! U.S. Gold Corp. (NASDAQ: USAU) is riding the perfect storm of record-high gold prices and surging copper demand. With gold surpassing $5,500 per ounce this year and copper entering a historic supply crunch driven by electrification, renewable energy, and infrastructure needs. USAU’s CK Gold Project in Wyoming stands out as one of the few fully permitted, shovel-ready gold-copper operations in North America. The project’s 1.02 million ounces of gold and 260 million pounds of copperin proven and probable reserves, combined with an expected 110,000 ounces of annual production, gives investors leveraged exposure to the commodities fueling the 21st-century economy. Analysts are taking notice: H.C. Wainwright maintains a Buy rating on USAU with a $27.50 price target, highlighting the company’s near-term production potential, strong economics, and strategic positioning in the U.S. mining-friendly jurisdictions of Wyoming, Nevada, and Idaho. With a management team led by mining veteran George Bee, institutional backing from investors like Eric Sprott and Franklin Templeton,USAU is poised to translate its resources into revenue. Discover why USAU is a must-watch as gold and copper prices soar and domestic production takes priority

Special Report MCD and TXRH: 2 Low-Risk Restaurant Stocks With UpsideWritten by Dan Schmidt. Published: 2/17/2026.

Key Points - The restaurant industry has become a key indicator for the K-shaped economy.

- Winners and losers are beginning to emerge based on the perceived value they offer to both higher-end and lower-end customers.

- McDonald's and Texas Roadhouse continue to grow comps despite the tough environment thanks to their value-oriented focus that keeps diners coming back.

- Special Report: The Biggest Market Shift No One's Talking About, Yet (From i2i Marketing Group, LLC)

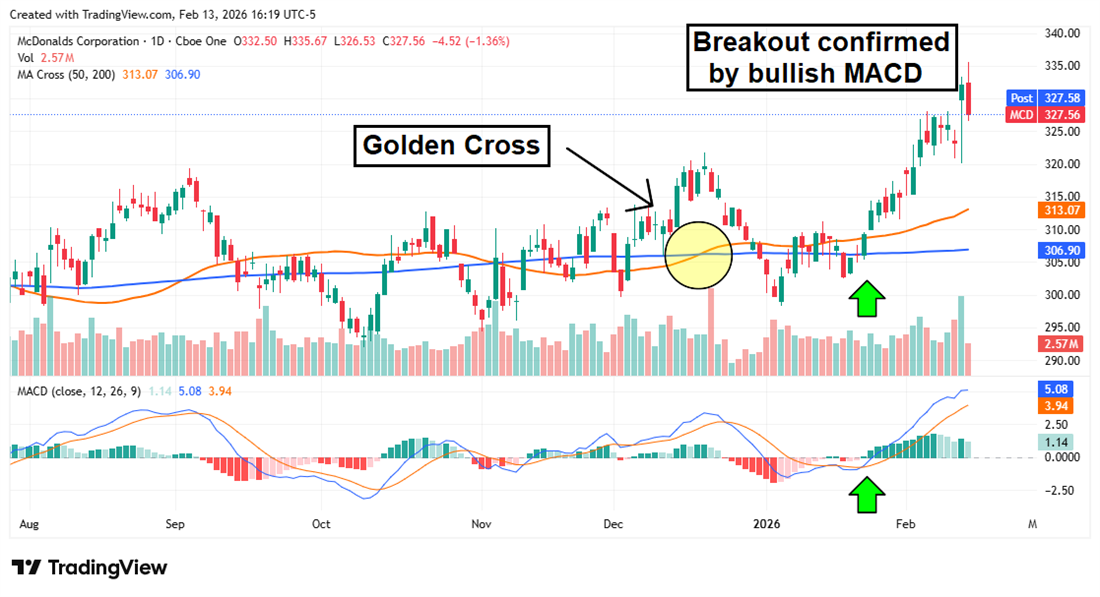

The restaurant sector is often at the center of debates about the K-shaped recovery. As consumer sentiment diverges from actual spending (especially in the retail sector), the food-service industry quickly reveals those divergent trends. While the upper end of the 'K' continues to indulge, more cost-conscious consumers at the bottom are searching for ways to stretch their dollars. In that environment, two restaurant chains are standing out for different reasons. The numbers speak for themselves: McDonald’s Corp. (NYSE: MCD) and Texas Roadhouse Inc. (NASDAQ: TXRH) continue to grow comparable sales and gain share from competitors. Below we explain why these two companies have thrived in a challenging dining market and why their stocks could outperform the industry this year. McDonald's Continues to Dominate the Fast-Food Market Earnings from McDonald’s and Wendy’s Co. (NASDAQ: WEN) last week highlighted how fast-food operators are separating themselves. McDonald’s reported Q4 2025 results, beating both EPS and revenue expectations with 9.7% year-over-year (YOY) sales growth. Global same-store sales topped forecasts with 5.7% YOY growth, including 6.8% growth in the United States. By contrast, Wendy’s Q4 2025 report showed revenue down 5.5% YOY and U.S. same-store sales falling 11.3%. How has McDonald’s managed nearly 7% U.S. sales growth while other quick-service restaurants (QSRs) struggle? The answer: consistent value. McDonald’s projects operating margins above 40% in 2026, which gives the company room to pursue a sustained Value Leadership strategy. Unlike the limited-time discounts used by Wendy’s and Burger King, McDonald’s Value Menu 2.0 is permanent. Extra Value Meals returned last September, and the company launched the McValue platform, featuring $5 Meal Deals and BOGO offers for $1. The Grinch Meal holiday promotion produced the largest single-day sales total in company history. McDonald’s app—boasting roughly 200 million active users—drives repeat visits, while a marketing emphasis on chicken items such as the McCrispy helps offset beef-price inflation. The company also plans to open about 2,600 new restaurants this year, even as some competitors close underperforming locations.

The breakout in MCD shares began before last week’s release. A bullish crossover in the Moving Average Convergence Divergence (MACD) indicator coincided with the stock moving above its 50-day and 200-day simple moving averages (SMAs), signaling strong upward momentum. If lower-income consumers continue to trade down for value, McDonald’s looks well-positioned to keep growing sales, supported by both fundamental and technical catalysts in 2026. Texas Roadhouse Gains Share Despite Commodity Headwinds Soaring beef prices have shadowed Texas Roadhouse shares for much of the past year. Beef has outpaced inflation since the pandemic, and the rapid increases over the last two years alarm many restaurant owners and investors. Rising prices are partly driven by cattle shortages that pushed live cow and steer prices to record levels—a trend likely to persist into 2027. Despite that headwind, Texas Roadhouse continues to grow same-store sales faster than many casual-dining peers. The chain’s barbell strategy delivers value for budget-conscious diners while offering premium steaks and upcharge options for guests willing to splurge. In its Q3 2025 report released in November, Texas Roadhouse posted comps of 6.1% and nearly 13% YOY revenue growth despite a 224-basis-point rise in food-and-beverage costs. Management raised prices just 1.7%—a deliberate margin sacrifice to preserve value for customers. Customer experience is central to the brand’s durability. Large portions, quick service, efficient digital kitchens, and numerous add-ons create the sense of a special night out without a hefty bill. Many diners report Texas Roadhouse feels "worth it" for date nights and family dinners because the combination of value and experience meets expectations.

TXRH performance so far this year suggests the doldrums of 2025 may be fading. The stock opened 2026 with an 11-day win streak that pushed it through the 200-day SMA, followed by consolidation as the Relative Strength Index (RSI) cooled and the 50-day and 200-day SMAs converged. With a Golden Cross appearing likely, the 50-day SMA could act as support for a new rally. That level has held once already, and the share price is approaching the 50-day average—potentially a good entry point for new investors. A fresh catalyst arrives when the company reports Q4 2025 results after the market close on Feb. 19.

|

No comments:

Post a Comment