Hey there,

Over the past week, we’ve sent you a few emails about the $5 for 5 weeks MarketBeat All Access offer.

But you haven’t jumped in yet.

And to be honest... I’m a little surprised.

We’ve had a huge response—thousands of investors have already signed up. I thought you'd be one of them.

Because here’s the thing: this isn’t a free trial with restrictions or fine print.

This is full access to the exact tools 11,000+ serious investors use every day—for just $5.

So why the hesitation?

I started thinking about what might be holding you back... and it clicked.

Maybe you’ve seen deals like this before that didn’t turn out to be what they promised.

Maybe you’re wondering if it’ll be hard to cancel. Or if it’s really worth it.

Totally fair questions.

So let me make this 100% clear:

You’ll get a reminder 7 days before your access renews. No surprises, no auto-renew “gotchas.”

You can cancel anytime—no hassle. Even after it renews, there’s a 30-day satisfaction guarantee.

You get everything. Not a teaser, not a lite version—the full platform.

We built All Access to help investors like you make smarter, faster decisions using real-time alerts, stock screeners, analyst ratings, and curated trade ideas.

Here’s a quick look at what’s inside:

-

Real-time SMS and email trade alerts for 5-day, 10-day, and long-term moves

-

Exclusive access to our MarketRank™ stock ratings, updated daily

-

Advanced screeners, heat maps, and portfolio monitoring tools

-

Premium research reports and actionable newsletters—no limits, ever

All of it—just $5 for your first 5 weeks. After that, you decide if it’s worth sticking with.

But this offer is ending in just a few days, and once it’s gone… it’s gone.

If you’ve been waiting for a sign—this is it.

Unlock 5 Weeks of All Access for $5![]()

Talk soon,

Shannon Tokheim

Associate Editor, MarketBeat

P.S. $5 gets you full access to a platform built to help you trade smarter. Not a sample. Not a trial. Just the real deal. But you only have a few days left to claim it. Confirm your access here.

3 Under-the-Radar Earnings Surprises Could Signal a New Trend

Submitted by Dan Schmidt. Date Posted: 2/17/2026.

Key Points

- Earnings season is starting to wrap up as more than 75% of S&P 500 companies have reported their latest results.

- Earnings and revenue beats are in line with historical averages, but divergences beneath the surface are creating different winners and losers than 2025's market.

- These three stocks typically fly under the earnings radar in their respective industries, but their positive recent reports deserve a closer look.

- Special Report: [Sponsorship-Ad-6-Format3]

Earnings season is winding down, and more than three-quarters of S&P 500 companies have reported their latest results. According to FactSet, about 74% of firms that have reported so far have beaten analysts' EPS estimates and 73% have beaten revenue estimates.

While those overall numbers sit near five- and ten-year averages, wide dispersion between winners and losers kept aggregate earnings growth roughly flat for the period. Several of last year's winners have underperformed in 2026, while some prior laggards have posted parabolic gains. Three companies whose reports don't usually dominate headlines still deserve attention for what showed up in their most recent filings. Are these one-time outliers or signs of a broader trend?

Applied Materials: Semiconductor Demand and Guidance Drive Double-Digit Gains

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

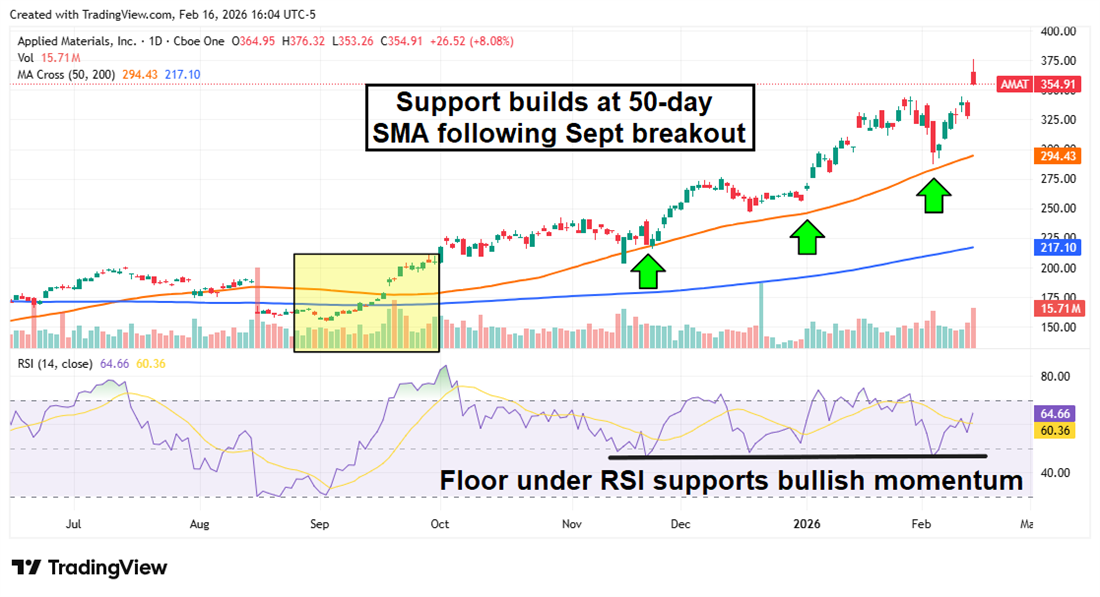

Applied Materials Inc. (NASDAQ: AMAT) is probably the most "on-the-radar" stock here, with a roughly $280 billion market cap and about $28 billion in annual sales. As a picks-and-shovels play in the semiconductor supply chain, Applied Materials often reports in the background while NVIDIA Corp. (NASDAQ: NVDA) or Alphabet Inc. (NASDAQ: GOOGL) grab headlines. Still, its most recent report warranted attention: AMAT shares surged roughly 12% after the results on strong demand and upbeat guidance.

The company reported its fiscal Q1 2026 results on Feb. 12, surpassing analysts' estimates for both EPS and revenue — with EPS beating expectations by about 7%. More important to investors was CEO Gary Dickerson's forecast of roughly 20% sales growth for calendar 2026, a number that topped even the most optimistic analyst projections. Most revenue comes from the Semiconductor Systems division, which supplies equipment for flash memory, logic manufacturing, transistors, DRAM and other chip segments. Dickerson guided Q2 revenue to about $7.65 billion and called for continued rapid growth in Applied Global Services.

Analysts moved quickly to raise targets and ratings. AMAT received upgrades from Hold to Buy at Summit Insights and KGI Securities, and the average price target among 17 analysts who raised their outlook is now $435 — roughly 20% above current levels.

AMAT shares have been in an uptrend since September, when the price crossed above both the 50-day and 200-day simple moving averages (SMAs). The 50-day SMA has acted as reliable support on pullbacks. The Relative Strength Index (RSI) remains below the overbought threshold of 70 despite the post-earnings move, suggesting the rally may have staying power.

Advance Auto Parts: Turnaround Efforts Begin to Pay Off

Advance Auto Parts Inc. (NYSE: AAP) may be creeping back onto investors' radars after losing more than 50% over the last five years. The past 12 months were particularly turbulent for the company (and the automotive sector broadly): the firm reported a loss of more than $10 per share in Q4 2024 and then faced tariff headwinds following the Trump administration's transition. CEO Shane O'Kelly has focused the company on cost cuts and a "back to basics" approach, and those efforts are starting to show results.

Advance Auto Parts' Q4 2025 results outperformed expectations. Revenue modestly beat estimates ($1.97 billion vs. $1.95 billion expected), but EPS of $0.86 was more than double the consensus. Same-store sales grew about 1% for the year, and management closed 17 underperforming locations. The 2026 guidance helped, too: management projects comps of 1–2%, roughly 45% gross margin, EPS between $2.40 and $3.10, and around $100 million in free cash flow generation.

Some profit-taking followed the release because the stock had already climbed nearly 50% year-to-date. Still, the technical picture looks constructive: the share price has broken above both the 50-day and 200-day SMAs, and the Moving Average Convergence Divergence (MACD) shows a bullish crossover with rising momentum — signals that support the continuation of the uptrend once volatility subsides.

Rivian: Narrowing Losses and Product Catalysts for 2026

Friday the 13th proved lucky for Rivian Automotive Inc. (NASDAQ: RIVN), which beat both top- and bottom-line estimates in its Q4 2025 report. Year-over-year revenue declined about 25% as EV tax credits expired, but sales still topped expectations and the company narrowed its loss to $0.66 per share.

Smaller losses were driven by a roughly $5,500 increase in average vehicle selling price and about a $9,500 reduction in average cost of vehicles sold. Rivian reported its first year with gross profit, and the more affordable midsize R2 model is slated to begin deliveries in Q2 2026. Management expects to sell 62,000–67,000 vehicles in 2026, with the low end representing roughly a 47% increase over 2025.

RIVN shares jumped about 20% in a volatile session after the report, though some gains faded from the open. The stock now sits at the 50-day SMA, which previously acted as support during late-2025 rallies. A bullish MACD crossover indicates improving momentum, but sustained upside likely depends on a successful R2 rollout and continued margin improvements.

Value or Growth: 2 Ways to Invest in the Energy Transition

Submitted by Chris Markoch. Date Posted: 2/18/2026.

Key Points

- Energy Transfer delivers stable, fee-based cash flows and high income tied to natural gas and NGL infrastructure, which remain critical to global energy demand.

- Constellation Energy is leveraging its nuclear fleet to secure long-term AI data center contracts, turning clean power into durable growth.

- Investors don’t need to choose between value and growth; the energy transition supports both hydrocarbon infrastructure and carbon-free generation.

- Special Report: [Sponsorship-Ad-6-Format3]

Energy stocks have been unpredictable for investors over the past five years, partly because of a disconnect between where consumer dollars are going and where investor capital has been flowing.

To use an energy-sector analogy, consumers are downstream in the energy markets. They experience the energy transition in tangible finished products: EV chargers, solar panels and lower-carbon power reflected on their monthly energy bills.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Most of the investment action, however, is happening upstream. That includes infrastructure and power-generation assets whose returns depend on regulatory outcomes, long-term contracts and capital discipline — factors that can take years to materialize.

Another issue has been a misunderstanding of the nature of this ongoing energy transition. It is often framed as a simple “either-or” debate between fossil fuels and renewable energy. Institutional investors, though, are playing the long game; they see this as an “all-of-the-above–and-then-some” problem.

The world needs more reliable sources of power. That was true before the surge in demand from artificial intelligence (AI) and hyperscale data centers.

That sets up an important question for investors looking to profit from the energy transition: Do you prioritize durable income from the existing hydrocarbon system, or do you lean into long-duration growth tied to carbon-free generation and data-center demand?

Two names that embody those choices are Energy Transfer (NYSE: ET) and Constellation Energy (NASDAQ: CEG). Energy Transfer is a high-yield midstream partnership whose cash flows are tied to volumes moving through pipelines and terminals. Constellation Energy is a nuclear-heavy power producer increasingly positioned as a critical supplier of 24/7 clean energy to hyperscale data centers.

Energy Transfer: Income, Scale, and Incremental Growth

Energy Transfer’s latest quarter underscored why many income-focused investors still see midstream as the most straightforward way to get paid while the energy transition plays out. For Q4 2025, ET generated approximately $4.2 billion of adjusted EBITDA, up about 7.7% year-over-year, on record transported volumes across interstate pipelines, midstream, NGL and crude segments.

Even though Energy Transfer missed consensus earnings per share (EPS) in the quarter (25 cents vs. 34 cents expected), the core story for shareholders is the stability of fee-based cash flows, improving leverage metrics and a visible project backlog focused on NGLs, refined products and intrastate gas.

Strong demand from natural-gas power generation and data centers is driving record throughput and justifying roughly $4.5 billion of organic growth CapEx in 2025, while still supporting ongoing distribution growth. In other words, ET offers ownership of the existing hydrocarbon backbone of the North American energy system, with the AI and energy-transition narrative acting as a tailwind rather than the core thesis. This outlook is supported by analysts who rate ET stock a Moderate Buy with a price target of $21.36, which would be about a 14% increase from current levels.

Constellation Energy: Nuclear, AI, and Long-Duration Growth

Constellation Energy sits at a very different point on the energy-transition spectrum. Many consumers know the company as a utility giant. However, Constellation is the largest producer of clean, carbon-free energy in the United States and is working to lead the transition.

For starters, Constellation controls the largest U.S. nuclear generation portfolio and has been methodically converting that footprint into long-term, premium-priced contracts. Deals with Microsoft Corp. (NASDAQ: MSFT) and Meta Platforms Inc. (NASDAQ: META) illustrate the company's strategy to reposition legacy nuclear assets as dedicated power hubs for AI data centers. 20-year offtake contracts can effectively turn carbon-free megawatts into infrastructure-like cash flows.

Constellation’s strategy has also expanded through mergers & acquisitions (M&A).

A recently completed $26.6 billion acquisition of Calpine broadens its generation footprint and customer reach, deepening its position as a key supplier of reliable power into constrained regions.

This dual focus — being a reliable utility today while positioning for upside growth tomorrow — is reflected in CEG stock’s consensus price target of $404.93, which would be more than a 35% gain. That upside potential, combined with its modest dividend, makes CEG a compelling name to watch in 2026.

Which Stock Fits Your Portfolio?

For investors who want a high-yield vehicle tied to the existing fossil-fuel system, Energy Transfer is a straightforward choice. You get paid to own the pipelines that move the fuel the world still needs, with AI-driven demand and export markets providing incremental upside.

For those willing to accept more volatility and policy risk in exchange for long-duration growth, Constellation offers a leveraged play on carbon-free power and the buildout of AI data-center infrastructure. The company’s upcoming earnings should shed more light on the pace of that ramp.

In that sense, ET and CEG are not direct competitors so much as complementary tools. One lets you harvest income from today’s energy system, while the other gives exposure to what the grid may look like a decade from now. Thoughtful investors in the energy transition do not have to pick a side—they can own both, with clear expectations about the role each will play in the portfolio.

MarketBeat empowers individual investors to make better financial decisions by providing up-to-the-minute financial information and best-in-class investment research.

If you have questions or concerns about your subscription, feel free to contact our South Dakota based support team at contact@marketbeat.com.

If you would like to unsubscribe or change which emails you receive, you can manage your mailing preferences or unsubscribe from these emails.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Place, Suite 620, Sioux Falls, South Dakota 57103. United States of America..

No comments:

Post a Comment