From our partners at i2i Marketing Group, LLC

AI Runs on Nuclear. We Import 99% of the Fuel. Nuclear power delivers nearly 19% of U.S. electricity. It's steady. Strategic. Essential. But here's what most investors don't realize, America imports 99% of the uranium that makes it possible. Now AI data centers are driving a surge in electricity demand, and Washington is pouring billions into rebuilding domestic supply. That's creating a rare window for a small U.S. uranium company working in the heart of Wyoming. It's positioning itself where this national gap is widest. See the U.S. Company in the 'Catbird Seat' >

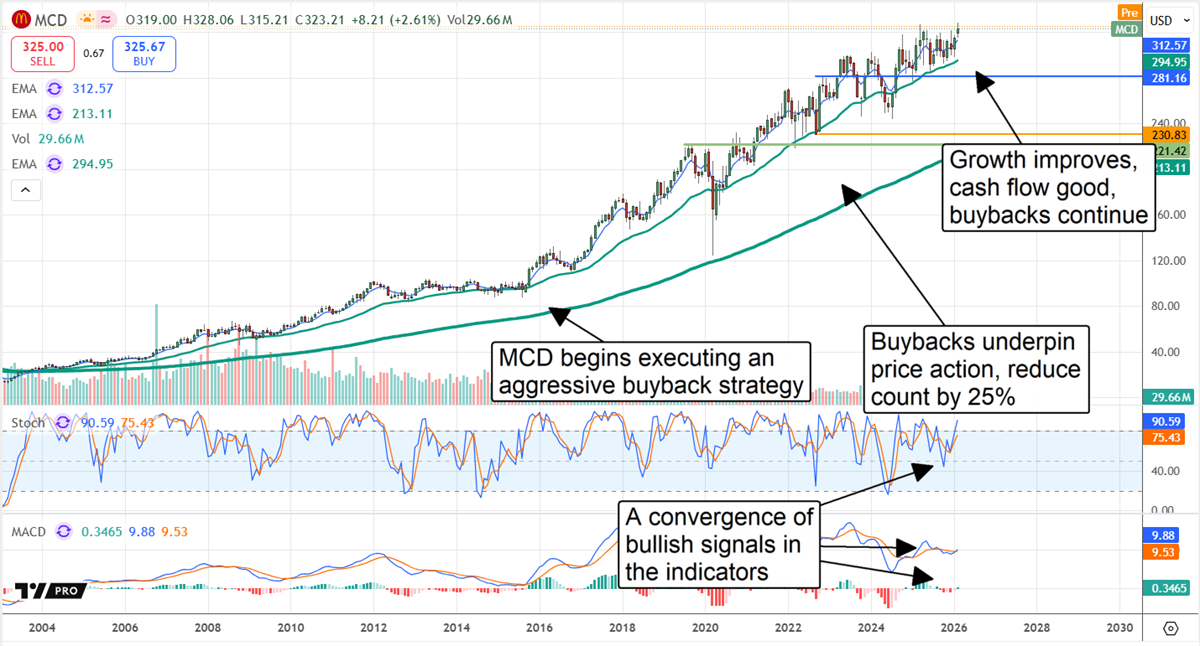

This Week's Featured Content McDonald's Serves Up Double-Sized Tailwind for GrowthAuthor: Thomas Hughes. Article Published: 2/13/2026.

Key Points - McDonald's is well-positioned to deliver growth in 2026, potentially outpacing expectations as tailwinds strengthen.

- Cash flow and capital returns are safe; growth suggests the buyback pace may increase.

- Analysts are lovin' it, boosting price targets and upgrading the stock following the report.

- Special Report: Bezos, Musk, Altman, Microsoft all betting BIG on THIS (From NXT Wave Research)

McDonald’s (NYSE: MCD) share-price uptrend appears intact, according to the Q4 earnings report. The company reported notable strengths, driven by accelerated comparable-store growth, its value proposition and continued store-count increases. McDonald’s menu tweaks and renewed focus on value resonate with consumers, who remain resilient and price-conscious. The critical takeaway is that the strong cash flow and capital returns this generates remain intact, and they continue to underpin the stock's performance. I Called Black Monday. Now I'm Calling March 26!

I predicted the 1987 crash six weeks early. I called the fall of the Berlin Wall. I pinpointed the exact bottom in 2009.

Now I'm staking my reputation on March 26, 2026 - the day I believe Elon will announce the SpaceX IPO.

Bloomberg is calling it "the biggest listing of ALL TIME."

A $1.5 TRILLION valuation... the "wealth-building" moment of the decade.

Today, I'll show you how to get in before the big announcement. Click Here to See How to Secure Your "SpaceX Access Code" McDonald’s has a long history of stock buybacks. Repurchases began reducing the share count in the early 2000s and have accelerated since. The most recent sustained price upswing began in early 2016, after a $20 billion buyback authorization that still influences today's price action. The company has cut its share count by roughly 25% since 2016. While the buyback pace slowed in fiscal 2025, Q4 strength and the 2026 outlook suggest it could pick up again. In fiscal 2025 McDonald’s reduced its share count by about 1% for the quarter and roughly 1% for the year, and it is likely to maintain a similar pace (at least) in 2026.

Analysts Praise MCD Q4 Results and 2026 Outlook McDonald’s delivered a strong Q4, with systemwide revenue up 9.5% to about $7.0 billion — 230 basis points above consensus. The gain was driven by a 5.7% increase in comps across all segments. The U.S. market led with 6.8% comps growth, while International Operated Markets grew 5.2% and International Developing Markets grew 4.5%. In the United States, strength was supported by increased headcount and higher check averages. The company’s loyalty program (rewards in the mobile app) was a growth pillar, delivering 20% revenue growth alongside a 19% increase in users. Margins held up well. Although the company faced some margin pressure, it offset those headwinds through operational execution and share-count reduction, producing 230 basis points of outperformance and 10% year-over-year growth in adjusted EPS. Cash flow — the critical metric for buybacks and dividends — was also solid. Full-year cash flow was sufficient to sustain buybacks and dividends while improving the balance sheet. Balance sheet highlights include negative equity, the result of decades of buybacks, but that deficit shrank by more than 50%, underscoring McDonald’s strong position. Debt remains on the higher side but is manageable given the company's cash flow and asset base. Analysts reacted positively to the report. Several firms issued updates immediately after the Q4 release, including price-target increases and rating upgrades. The upgrades indicate a shift in sentiment, strengthening the consensus rating to Hold. Consensus price targets imply a modest, single-digit upside — enough for a fresh high relative to the pre-release close — while higher-end targets push the market toward about $375, roughly 15% above resistance near early-February highs. McDonald’s Dividend and Institutional Interest: Investors Are Lovin’ It McDonald’s dividend and strong institutional interest are reinforcing the stock's momentum. The dividend payout ratio is relatively high at about 65%, but that is not unusual for a mature, reliable dividend payer. The company is on track to become a Dividend King in 2026, having raised its dividend for 49 consecutive years and poised to reach 50. The 2.3% dividend yield is meaningful — more than double the broad-market average — and helps keep institutions engaged. Institutions sold in Q4 2025, which capped gains late in the year, but overall they were net buyers during the year, purchasing about $2 for every $1 sold. Activity accelerated in January 2026, when institutional buying exceeded $4 for every $1 sold. That behavior reflects a solid support base and a strengthening tailwind for the stock.

|

No comments:

Post a Comment