Dear Fellow Investor,

I've been investing in technology for over 40 years.

And I've learned one thing…

The BIGGEST money gets made right before everyone realizes what's happening.

Not after.

My name is George Gilder.

In 1991, I predicted smartphones would change the world.

In 1994, I said streaming video would destroy Blockbuster.

In 1996, I called Amazon's dominance when it was "just a bookstore."

People thought I was nuts.

But early investors who listened?

- Apple: 249,900% since IPO

- Netflix: 112,700% from going public

- Amazon: 216,100% since IPO

Now I'm seeing something that could be BIGGER than all of them.

The Trump administration just secured a $200 billion investment in a new computing technology.

It's called wafer-scale processing.

And my research suggests it could make today's AI data centers obsolete.

Three companies are leading the charge by building what I call the "Trillion Dollar Triangle" capable of:

- Processing speeds up to 100X faster than current systems

- Using 90% less energy consumption

- Eliminating the need for massive data centers

This isn't theoretical.

It's already working in real-world applications.

And Wall Street is still asleep at the wheel.

>>Get the three company names before the crowd catches on <<

To the future,

George Gilder

Editor, Gilder’s Technology Report

The Last 2 Times Amazon's RSI Did This, the Stock Rallied 60%

By Sam Quirke. Article Published: 2/13/2026.

Key Points

- Amazon has slid roughly 20% from last year’s all-time high, with the selloff accelerating after last week’s earnings report.

- The stock’s RSI has now dipped below 30, a rare occurrence that previously preceded big recovery rallies.

- With analysts still overwhelmingly bullish and price targets ranging north of $300, the risk/reward profile is looking quite attractive.

- Special Report: [Sponsorship-Ad-6-Format3]

Having begun the year near $250, tech titan Amazon.com Inc (NASDAQ: AMZN) is now trading around $210.

A choppy January turned into a bruising start to February after the company reported a rare earnings miss and unveiled a sharply higher capital-expenditure forecast that rattled investors.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

The stock gapped down after the report and has shown few signs of reclaiming lost ground. What was meant to be a strong start to the year has instead become investors' first confidence test of 2026.

The stock is roughly 20% below its November all-time high, with momentum clearly swinging to the bears.

Yet beneath the surface, something notable is happening. Because selling has dominated buying, Amazon's relative strength index (RSI) has fallen below 30, placing the stock in extremely oversold territory. That reading is uncommon, but history suggests it's worth watching when it appears.

An Interesting Pattern

The last time Amazon's RSI dropped below 30 was in April 2025. The stock went on to rally roughly 60% from that low. The previous sub-30 reading occurred in the summer of 2024 and was followed by a similar rebound of about 60%.

That doesn't guarantee a repeat, but it does point to a pattern worth monitoring. When sentiment toward Amazon becomes this washed-out, it has historically preceded substantial upside more often than further downside.

Why This Setup Could Rhyme With the Past

As regular readers know, there are several reasons to be constructive on Amazon's prospects beyond this technical setup. The current weakness appears driven less by a broken business model and more by concerns about spending.

Investors were unsettled not only by the modest earnings miss but also by the scale of capital spending tied to Amazon's AI ambitions. In a market increasingly sensitive to spending discipline, that headline carried outsized weight.

Still, the company's fundamentals remain largely intact. AWS growth, for example, remains solid, and Amazon's retail business continues to perform steadily. A single earnings miss—especially one measured in single-digit cents—does not erase those trends.

Analysts Are Still Screaming Buy, Buy, Buy

Just as importantly, analyst support has barely wavered. Since the report, the consensus has been near-unanimous in backing the stock as a Buy, with firms such as Morgan Stanley, Wells Fargo and Argus setting new price targets of $300 or higher. From current levels, that implies more than 40% upside.

That may not match the roughly 60% surges after prior sub-30 readings, but it underscores the potential opportunity emerging right now.

What Could Derail the Bounce Thesis

The obvious risk is that this time is different. If capital spending keeps ballooning without visible returns, or if broader tech sentiment deteriorates further, oversold conditions alone won't trigger a sustained recovery. Stocks can remain oversold longer than investors expect, regardless of underlying fundamentals or analyst support.

There is also the technical reality that Amazon's recent attempts to rally have been underwhelming. While the stock was bought up off its post-earnings lows on Feb. 6, subsequent trading days showed little follow-through.

Watching the Ticker

For now, it comes down to short-term price action. With tech stocks generally under pressure, an immediate snapback in Amazon may be optimistic. But if selling pressure eases and buyers step back in, the oversold setup could lead to an interesting rebound.

Why eBay's Depop Acquisition Matters More Than the Earnings Beat

By Chris Markoch. Article Published: 2/20/2026.

Key Points

- eBay’s Q4 beat and GMV acceleration support a comeback narrative, even as the stock remains pressured by broader “AI trade” sentiment.

- Advertising and recommerce are emerging as durable growth engines, while Depop adds a targeted Gen Z/Millennial wedge.

- Depop integration costs, cyclical category tailwinds, and margin pressure remain the main risks to watch.

- Special Report: [Sponsorship-Ad-6-Format3]

Shares of eBay Inc. (NASDAQ: EBAY) are up about 3.8% the day after the company delivered a strong Q4 2025 earnings report. On one level, the results make sense: eBay is a pure-play on consumer spending, which has remained resilient despite mixed macroeconomic data. And eBay fits into the "discount" segment of retail stocks that has held up reasonably well in a volatile market.

There was a lot for investors to like. Revenue of $2.97 billion beat expectations of $2.87 billion. A key metric, gross merchandise volume (GMV), climbed to $21.2 billion — up almost 6% globally and nearly 10% in the United States — suggesting the platform is expanding and attracting more customers.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Another headline from the quarter was the announcement that eBay will acquire Depop, the secondhand clothing marketplace owned by Etsy Inc. (NASDAQ: ETSY), for $1.2 billion in cash. The move is a strategic attempt to capture more of the Gen Z and Millennial customer base.

Like many stocks with even minimal exposure to artificial intelligence (AI), EBAY traded lower earlier in 2026 ahead of the report. One strong quarter won't erase that trend, but there are several reasons to believe in eBay's comeback.

Ads, Fashion, and the Recommerce Angle

The Q4 report highlighted three specific engines doing the heavy lifting. The first is advertising. On an annualized basis, eBay is approaching $2 billion in ad revenue — a line of business that was almost non-existent five years ago.

Total advertising revenue was $544 million in Q4, representing GMV penetration of nearly 2.6%, with first-party ads growing over 17% to $517 million. About 4.8 million sellers adopted at least one promoted listing product during the quarter. The takeaway is that advertising is becoming an embedded behavior on the platform, not just an optional feature for power sellers.

The second growth engine is recommerce (pre-owned and refurbished merchandise). This category accounted for over 40% of the company's GMV in 2025 and grew roughly 10% during the year. Recommerce is an area where eBay is distinct from Amazon.com Inc. (NASDAQ: AMZN), and one that Amazon will be hard-pressed to replicate at meaningful scale.

The third engine is the Depop acquisition. In 2025, Depop generated about $1 billion in gross merchandise sales for Etsy. Nearly 90% of Depop's 7 million active buyers are under 34 — a demographic eBay has historically struggled to attract. Depop also specializes in private-label fashion, one of the fastest-growing segments in retail. If those shoppers migrate to eBay, the platform could gain a credible foothold that drives revenue growth.

A Marketplace Revamp With Real Teeth—or Temporary Tailwinds?

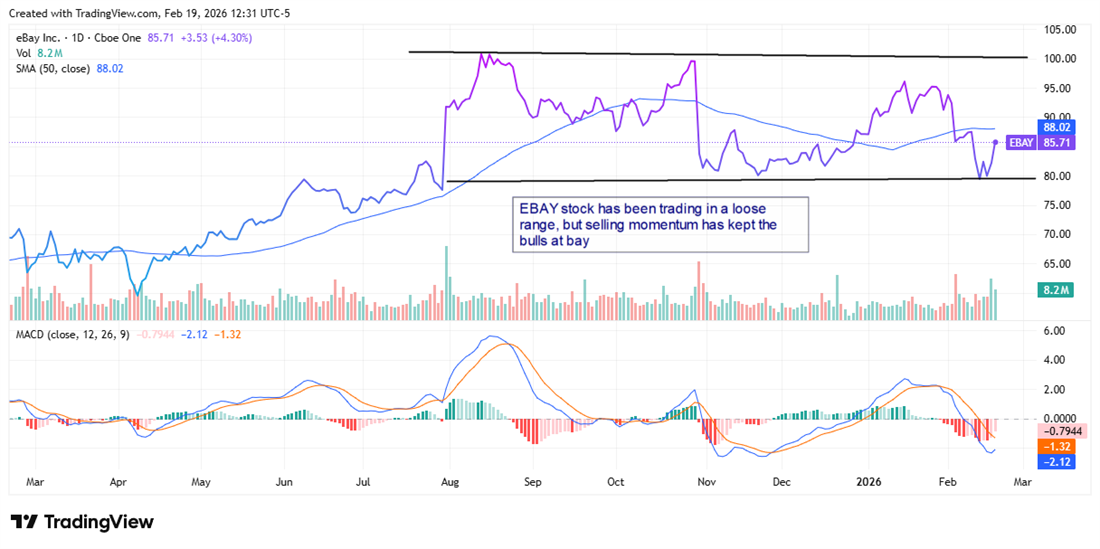

Institutional sentiment on EBAY has been bearish over the past three quarters, with selling outpacing buying by roughly $2 billion. Some of that selling followed the stock's run to an all-time high in August 2025. Since then, EBAY has traded in a loose range with support near $80 and resistance around $100.

eBay analyst forecasts on MarketBeat show analysts have been quick to raise price targets after the quarter. Several new targets sit above the consensus price of $96.52, about 12% above the stock price at the time of writing. Needham & Company raised its target to $122 from $115 — the highest among recent revisals.

Investors should also consider the company's dividend. A dividend alone isn't the right reason to buy EBAY; investors should want to see the company investing in growth, as it is with the Depop deal. Still, the 1.35% yield is above the S&P 500 average, and the company has increased the dividend to $1.16 at an average rate of more than 14% over the last three years. With a payout ratio just above 25%, the dividend appears sustainable and not a drain on cash.

Risks That Investors Shouldn't Ignore

Despite the bull case, several risks merit attention. First, some of Q4's GMV growth was commodity-driven. Management acknowledged on the earnings call that bullion, collectible coins, and Pokémon trading cards provided meaningful tailwinds in late 2025. Those categories are cyclical and are unlikely to repeat at the same rate.

Second, while strategically sensible, the Depop deal brings near-term costs. eBay expects the acquisition to be a low single-digit headwind to non-GAAP operating income growth and to dilute EPS growth in the near term, with accretion not expected until 2028.

Third, non-GAAP gross margin slipped nearly 80 basis points year over year. Sustainable margin expansion remains a central question, given Amazon's logistics muscle and Shopify's (NASDAQ: SHOP) seller ecosystem. Management said the margin dip was primarily due to scaling managed shipping and the Authenticity Guarantee programs — necessary investments that underscore the real costs of protecting trust on a peer-to-peer marketplace.

This email content is a sponsored email from Eagle Publishing, a third-party advertiser of MarketBeat. Why was I sent this message?.

If you have questions or concerns about your subscription, please feel free to email MarketBeat's U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Pl., Suite 620, Sioux Falls, SD 57103. U.S.A..

No comments:

Post a Comment