Hi, Tim Plaehn here.

Silver has become one of the best investments for both growth AND income.

I've just found one tiny fund that is now delivering up to 20% in annualized cash distributions….

And could deliver $1,170 every month for you.

However that's not all….

The share price has jumped 68% in just 5 months.

This is one of the rarest combinations I've seen in 20 years of analyzing investments.

Click here to see how this works.

But hurry: the next monthly payout hits soon.

To your income,

Tim Plaehn

Lead Income Strategist

P.S. This isn't physical silver. It's a simple ETF that trades like any stock. Buy once, collect monthly income.

Buy the Dip? Broadcom's AI Moat Is Wider Than Ever

Reported by Jeffrey Neal Johnson. Article Posted: 6/5/2026.

Key Points

- Broadcom benefits from massive capital investments by major technology partners seeking to aggressively expand their custom artificial intelligence hardware capabilities.

- The shift toward custom silicon perfectly positions Broadcom to capture immense revenue streams through long-term hardware and networking supply agreements.

- Strong operational efficiency allows Broadcom to scale operations rapidly while maintaining exceptional profitability and generating substantial free cash flow.

- Special Report: Elon’s “Hidden” Company

When a technology leader beats earnings estimates, reports 143% growth in its core AI segment, and generates more than $10 billion in free cash flow in a single quarter, a sharp stock decline is not the obvious next move.

Yet that is exactly the situation investors in Broadcom Inc. (NASDAQ: AVGO) are facing.

SpaceX will crumble without these 5 companies (Ad)

The SpaceX IPO is drawing near, but the real opportunity may lie in 5 lesser-known companies providing the critical infrastructure SpaceX depends on to operate.

Goldman Sachs and Morgan Stanley are reportedly already building positions in one of these names. Another is a resource miner that Elon Musk's broader empire - including Tesla - relies on. Lance Ippolito has detailed all five inside his free SpaceX Investing Blackbook.

Download the free SpaceX Investing Blackbook before these names go mainstreamThe market's puzzling reaction points to a deeper misreading of Broadcom's strategic position.

That disconnect creates an opportunity for investors to look past short-term noise and focus on the powerful catalysts shaping the next decade of artificial intelligence (AI).

Wall Street's fixation on a single gross margin figure obscures a historic demand supercycle backed by the world's largest technology companies. The recent selloff looks like a classic case of missing the forest for the trees, because Broadcom's long-term growth drivers remain intact.

Alphabet's $80 Billion Blank Check

The most immediate and powerful tailwind for Broadcom is the unprecedented capital deployment by its key customers.

On June 1, 2026, Alphabet Inc. (NASDAQ: GOOGL) announced a staggering $80 billion equity capital raise specifically aimed at funding investments in AI infrastructure and global compute capacity.

For investors, that is a major demand signal for the very hardware Broadcom designs, develops, and supplies. An investment of this scale translates into fleets of new data centers that could require substantial chip and networking capacity.

Broadcom's multi-year agreement to supply multiple generations of Google's Tensor Processing Units (TPUs) supports long-term visibility into Google's AI infrastructure needs. Alphabet's capital raise may also support broader demand for suppliers tied to Google's AI build-out.

As hyperscalers scramble to build the computational power needed for next-generation AI, Broadcom serves as a leading pick-and-shovel provider, turning massive capital expenditures into direct revenue. That was on full display in the recent quarter, when Broadcom reported record AI semiconductor revenue of $10.8 billion and pointed to more than $30 billion in AI semiconductor bookings, giving investors another sign that hyperscaler demand remains strong.

The Great Margin Miscalculation

The post-earnings pullback in Broadcom's stock was primarily driven by concerns over margin compression. Broadcom's consolidated gross margin fell to 77.1% and is guided to dip further to roughly 74% in the next quarter. On the surface, that may look like a sign of weakening profitability.

This view, however, overlooks a more important metric: Broadcom's operating margin expanded by 200 basis points year over year to a record 67.3%. The dip in gross margin is not the result of pricing pressure or operational weakness, but of a deliberate shift in product mix. As Broadcom accelerates shipments of its custom AI accelerators, the lower-margin, high-volume hardware naturally makes up a larger share of revenue than its high-margin infrastructure software.

That is a sign of Broadcom's success, not its failure. It is strategically giving up a few points of gross margin to capture a tidal wave of AI revenue and reinforce its dominance. Think of it like a retailer selling a hugely popular gaming console at a slim margin to attract customers who then buy high-margin games and accessories.

In this case, Broadcom's custom XPUs are the consoles, and its broad ecosystem of networking and software is the high-value add-on. The proof is in the operating leverage, where revenue is growing far faster than costs, a hallmark of an efficient enterprise benefiting from a secular growth trend.

Private-Credit Talks Could Support Future AI Infrastructure Demand

Another pivotal, and perhaps underappreciated, development was the expansion of Broadcom’s XPU and AI networking deployments across major customers. Apollo Global Management and Blackstone are reportedly in discussions with Broadcom over roughly $35 billion in financing tied to its AI chip expansion. If finalized, a deal of that scale could provide another source of support as customers race to fund larger AI infrastructure projects, though the timing, terms, and final structure remain uncertain.

This innovative structure could become an important support mechanism for Broadcom’s AI growth story. If private-credit financing moves forward, it may help Broadcom and its customers fund the large upfront costs required to scale custom AI chips, networking systems, and related infrastructure.

That would not eliminate execution risk, but it could improve visibility into future AI demand. Broadcom has already disclosed multi-year AI relationships with major customers, including Google and Anthropic, and outside financing could make it easier for large customers to turn long-term compute plans into actual deployments.

For investors, the key takeaway is not that Broadcom is insulated from semiconductor cyclicality. It is that the company's AI business is increasingly tied to multi-year infrastructure projects, rather than short-lived chip demand cycles alone.

The Shareholder Shield: A Fortress of Cash Flow

While the market focused on margins, it appeared to overlook the financial fortress Broadcom has built to protect and reward shareholders.

Broadcom produced $10.3 billion in free cash flow in the second quarter alone. This exceptional cash generation is not just an accounting figure; it is the fuel for a robust capital return program that provides meaningful downside protection for the stock.

Broadcom's board has authorized a $10 billion share repurchase program and maintains a consistent dividend that has grown for 15 consecutive years. These programs may support shareholder returns and give Broadcom flexibility to buy back shares during periods of market volatility.

The recent disconnect between Broadcom's stock price and its strong operating performance presents a compelling setup. While sector-wide anxiety about AI valuations is understandable, Broadcom's direct, contractual ties to the world's largest infrastructure projects provide a level of demand certainty that many peers lack. Cautious investors looking for durable exposure to the AI hardware build-out may find that this market-driven repricing is a strategic moment to reassess Broadcom's long-term value proposition.

Okta’s AI Moment May Be Bigger Than Investors Realize

Reported by Thomas Hughes. Article Posted: 6/16/2026.

Key Points

- Okta's fiscal Q1 2027 results showed revenue of $765 million, growing 11.2% year-over-year, driven largely by rising agentic AI demand.

- OKTA shares surged more than 30% following the earnings release, reaching a four-year high, with analyst consensus price targets rising 18%.

- Institutions own more than 85% of Okta shares and shifted from distribution to accumulation in Q2, while the company's debt-free balance sheet supports ongoing share buybacks.

- Special Report: Elon’s “Hidden” Company

Okta’s (NASDAQ: OKTA) fiscal Q1 2027 earnings report changed the narrative, revealing that the company’s strength and cash flow are being driven by AI-related demand. While AI is disrupting SaaS stocks, the disruption appears to be favorable, contrary to expectations, with cybersecurity at the forefront. The need is simple: AI must be secure at every level. Without security, AI is untrustworthy at best and dangerous at worst, and Okta is central to securing the global tech ecosystem.

Okta’s cloud-native, vendor-neutral approach to identity security means no vendor lock-in and gives it the largest, broadest addressable market among its peers. The system also integrates seamlessly, has nearly 100% uptime, and offers easy-to-use features that support single sign-on for employees and instant onboarding and offboarding for HR teams.

SpaceX will crumble without these 5 companies (Ad)

The SpaceX IPO is drawing near, but the real opportunity may lie in 5 lesser-known companies providing the critical infrastructure SpaceX depends on to operate.

Goldman Sachs and Morgan Stanley are reportedly already building positions in one of these names. Another is a resource miner that Elon Musk's broader empire - including Tesla - relies on. Lance Ippolito has detailed all five inside his free SpaceX Investing Blackbook.

Download the free SpaceX Investing Blackbook before these names go mainstreamThe takeaway is that organizations and enterprises that need to secure identities and access, including agentic AI, can do so with Okta regardless of which vendor provides the technology being secured.

Regarding agentic AI, it drives an exponential increase in access requests, which in turn drives demand for Okta’s services.

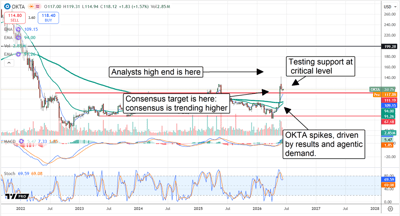

Okta’s AI-Driven Price Spike Supported by Analysts

Okta’s price spike itself is telling. The stock surged by more than 30% in the week of the release, indicating strong support at a cluster of moving averages. That cluster is significant, suggesting a market with aligned forces and a firm floor in the price action.

OKTA’s price has broken to a 12-month high and is now at a four-year high, indicating shifting market dynamics and a high probability of a trend reversal. As of mid-June, profit-taking has capped gains, but support remains at the high end of the previous range, setting the stage for another rally this summer.

Analyst trends are also central to the stock’s outlook, having strengthened following the Q1 release. MarketBeat tracked 25 revisions in the first week, and all but four were price-target increases. Three of the four outliers were reaffirmed targets, aligning with a forecast for consensus-or-better pricing, while the single downgrade was offset by a price-target increase to an above-consensus level.

The critical takeaway from the analyst data is that the consensus of fresh targets is just over $118, an 18% increase from the pre-release level, including the new high target of $150. The $118 consensus implies modest upside relative to the critical support target, while the $150 high suggests that another multiyear high could be set. In this scenario, the consensus trend provides support for price action, while the high end leads the market. Assuming upcoming releases extend the trends revealed in Q1, analysts’ price-target forecasts will continue strengthening and leading this market higher.

Institutional data suggest downside risk is limited this summer. The group owns more than 85% of the stock, providing a solid support base, and it shifted from distribution in Q1 to accumulation in Q2. The shift aligns with the April stock price bottom, strengthening it as a support target, and supports the May and June advance. The likely outcome is that this group retains its bullish posture in 2026, potentially accelerating accumulation as subsequent reports are released.

Okta Builds Momentum in Q1: Raises Guidance, but Outlook Remains Cautious

Okta had a solid quarter in Q1, with revenue of $765 million, up 11.2% year over year and just ahead of MarketBeat’s reported consensus. Strength was driven by agentic demand and reinforced by forward-looking metrics that suggest acceleration in upcoming quarters. Remaining performance obligation, a measure of contracted business, grew by 16%, suggesting that Q2 and full-year guidance updates were cautious. Management expects growth to continue and exceed consensus, but only by 9% in the current quarter and 9.5% for the year.

Margins and earnings were also strong. The company managed costs and spending effectively, resulting in adjusted earnings growth that exceeded forecasts by more than 600 basis points. More importantly, strong earnings and cash flow bolster the capital return outlook, particularly through aggressive share buybacks. Q1 activity reduced the share count by more than 2.2% on average, providing investors with significant leverage; the Q1 results and cash flow suggest that pace could continue in upcoming quarters and may even accelerate.

Okta’s balance sheet shows no red flags in 2026. The company operates without debt, has ample cash, and offers value for investors. Q1 highlights include increased cash and equivalents, reduced liabilities, and steady equity despite reinvestment and buybacks. Looking ahead, the likely outcome is that cash flow and free cash flow will continue to support growth and capital returns while maintaining fortress-like balance sheet metrics.

This email is a paid advertisement sent on behalf of Investors Alley, a third-party advertiser of DividendStocks.com and MarketBeat.

If you need assistance with your newsletter, please feel free to contact MarketBeat's U.S. based support team at contact@marketbeat.com.

If you no longer wish to receive email from DividendStocks.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC.

345 North Reid Place, Suite 620, Sioux Falls, South Dakota 57103. United States of America..

No comments:

Post a Comment