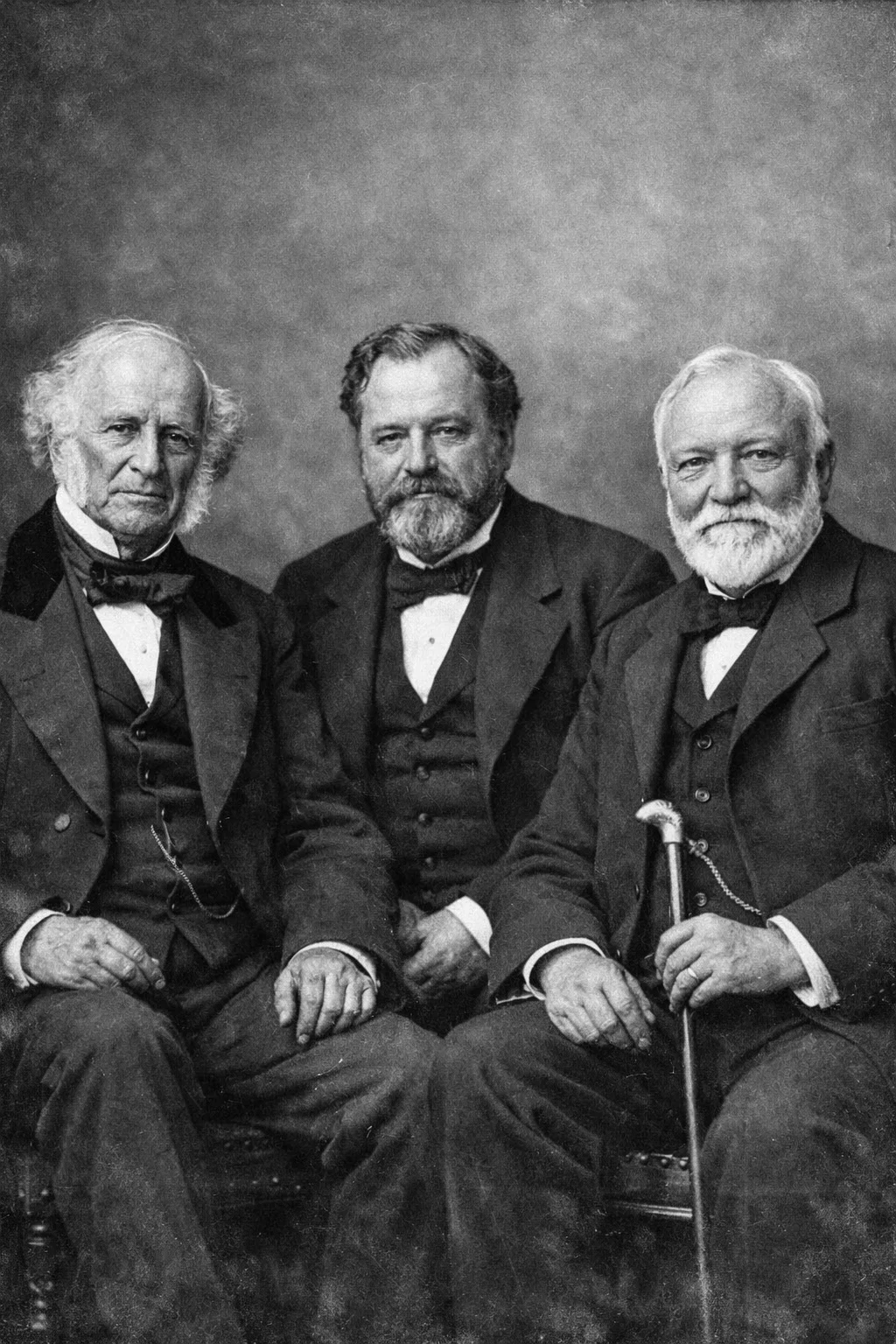

In the 1800s, the most powerful men in America decided to build something.

Cornelius Vanderbilt, Leland Stanford, and Andrew Carnegie.

They poured money into iron and steel, stretching across the entire continent.

The project cost roughly $10 billion, in today’s money - about $300 billion.

They built a railroad that forever changed the trajectory of the United States.

Today… four of the most powerful men on the planet have a very similar goal.

Jeff Bezos (AMZN), Mark Zuckerberg (META), Sundar Pichai (GOOG), Satya Nadella (MSFT)...

They’ve decided to build something too… not with iron or steel…

But the digital infrastructure of the next American economy.

And they’ve already committed $700 billion to build it this year alone.

When adjusted for inflation, more than double what the entire railroad system cost… in the first year of a decade-long project.

The last time men this powerful decided to reshape America's infrastructure, it created some of the biggest fortunes in history.

And this time around… the opportunity is even bigger.

Chris Rowe has put together a quick briefing on this new infrastructure project…

And what it means for several small companies at the heart of the project.

Bill Spencer

Sigma Lithium Proves Shorts Wrong: Market Reversal Underway

By Thomas Hughes. Article Published: 3/31/2026.

Key Points

- Sigma Lithium is on track for hypergrowth, cash flow, and improved balance-sheet health, bolstering the argument that its recent reversal is indicative of a better stock performance ahead.

- Analysts and institutional data reflect accumulation and a strengthening support base for the Canada-based mineral exploration and development company.

- Short-sellers pose a risk that may cap gains in the near term, but analyst forecasts suggest nearly 47% potential upside over the next 12 months.

- Special Report: Elon Musk already made me a “wealthy man”

Lithium prices are enjoying a strong run, up more than 122% over the past year. But many stocks of companies that mine the soft, silvery metal or process it into battery-grade lithium have yet to catch up.

That's particularly true for Sigma Lithium (NASDAQ: SGML), which looks like a compelling buy according to most market indicators — aside from short sellers who have recently begun to cover.

Elon Musk’s $1 Quadrillion AI IPO (Ad)

$1 quadrillion would be enough to send a $2.8 million check to every man, woman, and child in America. That is the scale of what analysts are calling the biggest AI IPO in history.

And right now, you can claim a stake before the company goes public, starting with just $500.

Elon Musk is predicting this investment could climb 1,000x from here. Early access is available today.

Claim Your Stake NowThe main obstacle was an operational shutdown that has since been resolved. Brazilian regulators temporarily closed the Grota do Cirilo mine over a waste-pile issue, which the company has addressed.

Now Sigma Lithium is back in production, and the key takeaway from its Q4 2025 results is that the lithium company is not only operational but also profitable and positioned for strong growth over the next two years.

Sigma Lithium Has Solid Quarter, Guides for Strength

Despite earlier operational challenges, Sigma Lithium reported a solid Q4 on March 30.

Lithium production and processing generated $31 million in operating cash flow, enabling meaningful debt reduction and support for the company’s strategy.

Management expects cash from operations to grow more than 10% in the current quarter, then to more than double sequentially in the company's second quarter, approaching $100 million for that period. Over the longer term, management forecasts roughly 200% production growth over two years as Phase II and Phase III come online, with all-in sustaining costs declining and earnings improving.

Sigma Lithium’s balance sheet reflects these actions. While cash, assets, and equity declined, that drop was driven by inventory sales and the cash uses they enabled. The company has paid down substantial debt, reducing trade leverage sharply and cutting total leverage by about 35%. The expectation is that rising cash from operations, per guidance, will replenish the cash balance, support further deleveraging, and improve long-term equity metrics.

No analyst revisions were recorded within the first few hours after the release, but the initial market response was optimistic.

Management is focused on cash generation, production ramps, and cash-flow guidance. Debt reduction also remains a priority, helping to shore up support.

MarketBeat tracks six analysts on the stock who together yield a consensus Hold rating. The split is even: two Hold, two Buy, and two Sell.

Price targets imply cautious optimism: the low-end provides a market floor at $13.90, and consensus suggests roughly a 40% upside as of late March.

Short Sellers Versus Institutions: Sell-Side Activity Drives SGML Volatility

Initial market reactions suggest that short sellers are covering positions, though some appear to be repositioning at higher price levels.

While the stock briefly popped more than 20%, gains were capped near the 150-week exponential moving average (EMA), a key long-term pivot. The 150-week EMA reflects long-term buy-and-hold sentiment; moving above it signals a shift from distribution to accumulation and is bullish.

Short sellers could cap the market around this level, but institutional buying may prevent sustained suppression. MarketBeat data shows institutions own about 65% of the stock, providing a strong support base with accumulation expected into 2026.

Institutions have been net buyers on balance for five consecutive quarters, including Q1 2026, with activity ramping sequentially. Over the trailing 12 months, institutions bought roughly $2.50 for every $1 sold — a ratio that may improve now that the company has turned a corner. The business developments have helped to de-risk the outlook, which is also strengthening.

Price action since the news has been favorable despite potential resistance near $13. The roughly 15% pop showed support at short-term EMAs and highlighted traders' and speculators' interest. This price action aligns with a bottoming process and could lead to a full reversal later this year.

Clearing the long-term EMA and the $13 level would confirm an inverse head-and-shoulders pattern, setting the stage for a more sustainable rally.

Merck Just Made a Big Bet on a New Cancer Growth Engine

By Jessica Mitacek. Article Published: 3/31/2026.

Key Points

- Merck is set to acquire Terns Pharmaceutical for $6.7 billion, adding its promising leukemia treatment to its growing hematology and cancer pipeline.

- This is Merck’s third multi-billion dollar deal in a year, a bolt-on strategy projected to drive a $70 billion commercial opportunity by the mid-2030s.

- With an average five-year gross margin of 73% and 14 consecutive years of dividend increases, Merck remains a top-tier performer with a Moderate Buy rating.

- Special Report: Elon Musk already made me a “wealthy man”

While the health care sector has struggled this year, that hasn’t been the case for all of Big Pharma.

Shares of New Jersey-based Merck & Co. (NYSE: MRK) have outperformed the sector and the broad market with a gain of more than 12%.

Elon Musk’s $1 Quadrillion AI IPO (Ad)

$1 quadrillion would be enough to send a $2.8 million check to every man, woman, and child in America. That is the scale of what analysts are calling the biggest AI IPO in history.

And right now, you can claim a stake before the company goes public, starting with just $500.

Elon Musk is predicting this investment could climb 1,000x from here. Early access is available today.

Claim Your Stake NowThe drugmaker’s stock recently got a boost when Merck announced it would acquire Terns Pharmaceuticals—a deal that bolsters its oncology pipeline and reinforces Merck’s reputation as a serial acquirer.

That mergers and acquisitions (M&A) activity has played a major role in the company’s steady growth and market-cap expansion, with Merck’s market value now more than $296 billion, ranking it third behind Eli Lilly (NYSE: LLY) (~$830 billion) and AbbVie (NYSE: ABBV) (~$370 billion).

Merck’s Terns Acquisition Is a Pivotal Oncology Play

On March 25, Merck announced it had reached terms to acquire Terns, a clinical-stage oncology company developing therapies including TERN-701, an oral allosteric BCR–ABL1 inhibitor for treating chronic myeloid leukemia.

According to the press release, Merck will acquire Terns for $53 per share in cash, giving Terns an approximate equity value of $6.7 billion. The deal further builds Merck’s presence in hematology with what the company describes as a “potential best-in-class candidate for the treatment of certain patients with chronic myeloid leukemia.”

The definitive agreement marks Merck’s third multi-billion-dollar acquisition in the past year. Although still in clinical stages, TERN-701 has shown promising activity, with “encouraging rates of molecular response and deep molecular response,” including responses in patients with high disease burden who had received multiple prior lines of therapy.

M&A Activity Has Helped Support Merck’s Earnings and Dividend Profile

Merck’s ability to secure the Terns deal underscores its central role in the pharmaceutical industry and supports an impressive earnings track record. The company has missed analyst estimates only once in the past 19 quarters, dating back to Q2 2021.

When the company reported Q4 2025 financials on Feb. 3, it posted earnings per share (EPS) of $2.04 versus expectations of $2.01, and revenue of $16.40 billion versus expectations of $16.19 billion. With a forward price-to-earnings multiple of 16.45, Merck’s EPS is forecast to grow nearly 10% over the next year, from $9.01 to $9.90.

In his earnings call, CEO Rob Davis attributed the company’s steady growth to new product launches, progress in key clinical programs, and added scale in respiratory and infectious diseases from the Verona Pharma and Cidara Therapeutics acquisitions.

"As a result of this progress, we now have line of sight to over $70 billion of potential commercial opportunity by the mid-2030s, $20 billion more than just a year ago and more than double consensus 2028 peak Keytruda revenue of $35 billion," Davis said.

While those revenue forecasts are attractive to shareholders and prospective investors, the key takeaway is the rapid scale Merck has achieved through its acquisition strategy.

That M&A activity has become a hallmark for the company. The Verona Pharma and Cidara Therapeutics deals—valued at $10 billion and $9.2 billion, respectively—were followed by the Terns announcement, valued at $6.7 billion.

Merck continues to pursue bolt-on acquisitions to diversify and strengthen its oncology, immunology, and infectious disease pipelines.

Integrating these biotech companies into its portfolio accelerates growth and expands Merck’s market share while minimizing hurdles as it enters new markets.

In turn, Merck has maintained a five-year average gross margin above 73%.

Those high and expanding margins indicate strong pricing power and operational efficiency, which together allow Merck to sustain and grow its dividend, currently yielding 2.84% (or $3.40 per share annually).

Dividends are common among mature health-care companies, but Merck stands out: the company has increased its payout for 14 consecutive years and posts a five-year dividend growth rate of 5.75%.

How Wall Street Feels About Merck

Based on the 18 analysts currently covering the stock, Merck carries a consensus Moderate Buy rating, with 11 analysts assigning MRK a Buy. With an average one-year price target of $127.13, Wall Street sees potential upside of more than 7%.

Institutional ownership is above average at over 76%, with inflows of nearly $37 billion exceeding outflows of about $19 billion over the past 12 months. Current short interest is just 1.18% of the float—roughly 29 million of the 2.47 billion shares outstanding—suggesting bears are largely keeping their distance.

Merck has been in the green zone on TradeSmith’s financial health indicator for more than six months, and the company scores higher than 93% of those evaluated by MarketBeat, ranking 39th out of 858 stocks in the medical sector.

This message is a paid sponsorship provided by True Market Insiders, a third-party advertiser of The Early Bird and MarketBeat.

If you have questions or concerns about your newsletter, please email our South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from The Early Bird, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Place, Sixth Floor, Sioux Falls, South Dakota 57103-7078. U.S.A..

No comments:

Post a Comment