Dear Reader,

I picked Nvidia in 2017….

Before it jumped as high as 3,852%…

And I just revealed the exact day this AI boom will end.

And if you’re wondering how that’s possible…

Well, I’m using an investment secret that correctly predicted the end of every major boom over the last century…

It predicted the end of the roaring 20s boom on October 31st of 1929… right before the great depression crash…

It predicted the end of the Reagan Bull Market in the 1980s on September 1st of 1987… right before the black Monday crash…

It predicted the end of the dotcom boom on February 1st 2000…

It predicted the end of the housing bubble bull market on January 2nd 2008…

And it predicted the end of the Post-Financial Crisis Recovery in February 3rd 2020… right before the Covid crash…

This same investment secret…

Is now pointing to the exact day this AI boom will end (click here to see it.)

Stay sharp,

JC Parets, CMT

Founder, TrendLabs

RingCentral's Cash Flow Hit a Record—And It's Fueling Bigger Returns

Authored by Nathan Reiff. First Published: 2/28/2026.

Key Points

- Cloud-based communications firm RingCentral is up 23% in the last year but remains a Hold, with analysts skeptical about the company's ability to continue its rally.

- Still, a promising Q4 2025 earnings period brought top- and bottom-line wins as well as impressive AI ARR growth.

- The company's pivot to agentic AI tools presents ample room for continued growth, but risks remain.

- Special Report: [Sponsorship-Ad-6-Format3]

The end of 2025 was bright for cloud-based communication technology firm RingCentral Inc. (NYSE: RNG). Though still a relatively small player in the industry with a market capitalization of about $3 billion, RingCentral's agentic AI strategy is nascent yet poised for significant gains. The company recently impressed across several financial and growth metrics and even announced its first-ever dividend.

Despite a nearly 23% gain over the last year and a spike after the company's late-February Q4 2025 earnings report, investor caution remains. Only four of 15 analysts rate RNG a Buy, producing an overall Hold rating. Wall Street's consensus price target of $34.04 sits about 4% below the current share price.

Buy this stock tomorrow? (Ad)

Not a Single "Mag 7" on This Legendary Investors List

A renowned former hedge fund manager – friends to some of the biggest investors in the world – just released a new list of his favorite AI stocks... and not a single Magnificent 7 name made the cut. Instead, an AI stock you've likely never heard of just flagged as "near-perfect" in his new investing scoring system.

How should investors reconcile RingCentral's encouraging results with that caution? For those willing to accept the risks of a smaller, up-and-coming company in a competitive industry, RingCentral shows several signs that it could continue its growth trajectory.

RingCentral's Financial Position Remains Stable & Growing

RingCentral's Q4 year-over-year (YOY) revenue growth of 4.8% was modest, but the company still beat analyst expectations on both top- and bottom-line results. Those gains were driven by solid customer growth across multiple product categories and rising interest from prospective clients.

The firm's financial strengths extend beyond earnings and revenue. It generated a record full-year free cash flow of $530 million for 2025, and its full-year GAAP operating margin turned positive, reaching 4.8%. The influx of cash allowed RingCentral to double its share buyback authorization to $500 million. The firm has also announced its first dividend payment of $0.075, payable on March 16.

These developments suggest RingCentral's growth may be sustainable. Management's 2026 guidance is optimistic: it expects 4.5% to 5.5% subscription growth, free cash flow of $580 million to $600 million, and a non-GAAP operating margin of 23% to 23.5%. The company also plans to reduce gross debt to $1 billion as part of a push toward an investment-grade credit rating.

The Role of Agentic AI in RingCentral's Growth Trajectory

RingCentral's agentic voice AI strategy targets business-to-consumer (B2C) applications, with the aim of helping business clients answer calls more quickly, handle a larger volume of customer inquiries with higher quality, and pursue more leads.

Early results in the AI landscape have been promising. The company nearly tripled its pure AI annual recurring revenue (ARR). AI product attach rates—a measure of AI add-on sales alongside other RingCentral products—more than doubled YOY and now account for roughly 10% of ARR. AI customers also show stronger retention and higher spending than non-AI users.

Growth in AI for RingCentral is accelerating and enabling the company to expand its AI offerings. The flagship AI Receptionist (AIR) product has about 8,300 customers, a 44% YOY increase. While that is an impressive trajectory, there remains substantial room for continued expansion of the AI user base.

What's in Store for RingCentral Investors

Despite the positive developments highlighted in the recent earnings presentation, there are reasons for caution. Revenue growth has slowed in recent quarters, and RingCentral faces intense competition from much larger players with advanced AI capabilities, including Microsoft Corp. (NASDAQ: MSFT) and other tech giants.

Even with improving free cash flow and shareholder-friendly actions, RingCentral still carries a substantial debt load. That debt could become problematic if the company encounters setbacks in its efforts to become a leading provider of agentic AI communications for business clients. Similarly, prioritizing AI products to the detriment of its traditional cloud-communications offerings could narrow its addressable market.

MCD and TXRH: 2 Low-Risk Restaurant Stocks With Upside

Authored by Dan Schmidt. First Published: 2/17/2026.

Key Points

- The restaurant industry has become a key indicator for the K-shaped economy.

- Winners and losers are beginning to emerge based on the perceived value they offer to both higher-end and lower-end customers.

- McDonald's and Texas Roadhouse continue to grow comps despite the tough environment thanks to their value-oriented focus that keeps diners coming back.

- Special Report: [Sponsorship-Ad-6-Format3]

The restaurant sector has often been central to debates about a K-shaped economy. While consumer sentiment diverges from actual consumer behavior (especially in the retail sector), the food service industry quickly reveals those divergent trends. The upper end of the "K" continues to indulge, while more cost-conscious consumers are trading down and seeking value to stretch their dollars.

In that environment, two restaurant chains are standing out for different reasons. Both McDonald’s Corp. (NYSE: MCD) and Texas Roadhouse Inc. (NASDAQ: TXRH) are growing comparable sales and taking share from competitors. Below we explain why these two operators have thrived amid a challenging dining environment and why their stocks could outperform the restaurant industry this year.

McDonald's Continues to Dominate the Fast Food Market

Nvidia CEO Issues Bold Tesla Call (Ad)

While headlines focus on Tesla's car sales, tech analyst Jeff Brown says the real story is Tesla's role in a $25 trillion AI revolution — one that Nvidia's CEO himself has called a "multi-trillion-dollar future industry" — and he's uncovered a little-known stock 168 times smaller than Nvidia that could be positioned to ride this breakthrough.

Click here now to see the full reportThe recent earnings reports from McDonald’s and Wendy’s Co. (NASDAQ: WEN) highlighted how fast-food players are differentiating themselves.

McDonald’s reported Q4 2025 results last week and beat expectations on both earnings per share (EPS) and revenue, delivering 9.7% year-over-year (YOY) sales growth.

Global same-store sales topped estimates with 5.7% YOY growth, including 6.8% growth in the United States. By contrast, Wendy’s Q4 2025 report showed a 5.5% YOY revenue decline and an 11.3% drop in U.S. same-store sales. How has McDonald’s managed nearly 7% U.S. sales growth while other quick-service restaurants struggle?

Value — consistently delivered. McDonald’s projects operating margins above 40% in 2026, which gives it the flexibility to pursue a Value Leadership strategy.

Unlike the short-lived promotions run by some rivals, McDonald’s Value Menu 2.0 is a permanent element of its offering. Extra Value Meals returned last September, and earlier this year the company launched the McValue platform, featuring $5 Meal Deals and BOGO-for-$1 offers. The Grinch Meal holiday promotion produced the largest single-day sales figure in the company’s history.

Meanwhile, the McDonald’s app—about 200 million active users strong—drives repeat visits, and a marketing push around chicken items like the McCrispy helps offset beef-price inflation. The company also plans to open roughly 2,600 new restaurants this year while some competitors, such as Wendy’s, close underperforming locations.

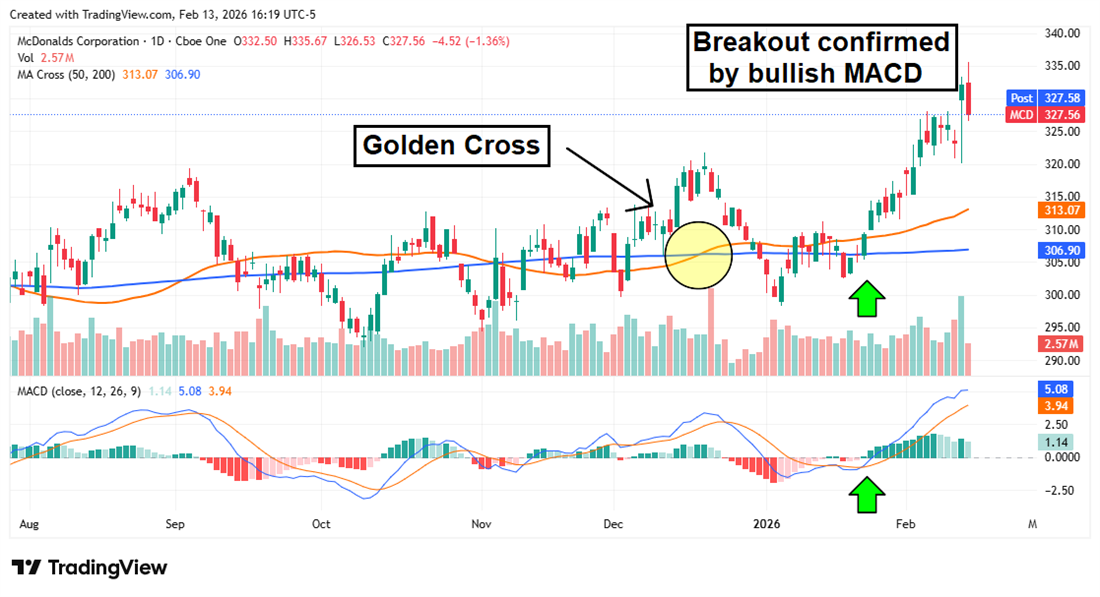

The breakout in MCD shares began well before last week’s results. A bullish crossover in the Moving Average Convergence Divergence (MACD) indicator coincided with the stock rising above both the 50-day and 200-day simple moving averages (SMAs), signaling strong upward momentum. If lower-income consumers continue to trade down for value, McDonald’s appears well-positioned to keep growing sales, supported by both fundamental and technical catalysts in 2026.

Texas Roadhouse Grows Market Share Despite Commodity Headwinds

Soaring beef prices have loomed over Texas Roadhouse shares for much of the past year. Beef costs have risen faster than inflation since the COVID-19 pandemic, and the surge over the last two years has unnerved restaurant operators and investors alike.

The increase has been driven in part by cattle shortages, which pushed live cow and steer prices to record levels—a trend likely to persist into 2027.

Despite that headwind, Texas Roadhouse continues to see same-store sales grow faster than many casual-dining rivals.

Texas Roadhouse’s barbell strategy delivers value for cost-conscious guests while offering premium steaks and upsell options for diners willing to spend more.

In its Q3 2025 report, the company posted comps of 6.1% and nearly 13% YOY revenue growth despite a 224-basis-point increase in food-and-beverage costs. Management raised menu prices by only 1.7%—a deliberate margin sacrifice designed to retain value-oriented customers.

Customer experience is another key to Texas Roadhouse’s durability. Traffic stability matters for fast-casual chains that rely on repeat visits. Large portions, brisk service, efficient digital kitchen operations, and many add-ons and upgrades create the feel of a special night out without an excessive bill. Customers often report that the restaurant is "worth it" for date nights and family dinners because the value and experience meet expectations.

TXRH performance so far in 2026 suggests the doldrums of 2025 may be behind it. The stock rose for 11 consecutive trading days to start the year, breaking through the 200-day SMA that had blocked earlier breakout attempts. That win streak was followed by consolidation, during which the Relative Strength Index (RSI) cooled to more neutral levels while the 50-day and 200-day SMAs converged.

With a Golden Cross appearing imminent, the 50-day SMA could act as support for the next leg higher. That level has already been tested and held, and the share price is now approaching the 50-day moving average—potentially an attractive entry point for new investors. A near-term catalyst arrives when the company reports Q4 2025 results after the market closes on Feb. 19.

This email communication is a paid sponsorship for Trend Labs, a third-party advertiser of InsiderTrades.com and MarketBeat.

If you need help with your account, please feel free to email our South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from InsiderTrades.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Place, Sixth Floor, Sioux Falls, S.D. 57103-7078. U.S.A..

No comments:

Post a Comment