Dear Reader,

Dr. Mark Skousen here.

I've worked for the CIA.

I've personally met four US presidents.

I've spent 45 years studying the markets — calling Black Monday six weeks before it happened... predicting the fall of the Berlin Wall... pinpointing the exact bottom in 2009.

But what I'm about to share with you is the boldest prediction of my career.

After meeting Elon Musk face-to-face at a private gathering of Wall Street elites, I'm now staking my reputation on one date.

March 26, 2026.

Mark it on your calendar right now!

That's when I believe Elon will announce the SpaceX IPO — what Bloomberg is calling "the biggest listing of ALL TIME."

I have an "access code" that lets you grab a pre-IPO stake before it happens.

But I'm only willing to share it with 500 people today. After that, you my never get the chance again.

Click here to see how to claim your “SpaceX access code”.

Yours for peace, prosperity, and liberty, AEIOU,

Dr. Mark Skousen

Macroeconomic Strategist, The Oxford Club

P.S. I don't make predictions lightly. When I put my name on something, I mean it.

Click here before the 500 spots are gone.

MCD and TXRH: 2 Low-Risk Restaurant Stocks With Upside

Reported by Dan Schmidt. Posted: 2/17/2026.

Key Points

- The restaurant industry has become a key indicator for the K-shaped economy.

- Winners and losers are beginning to emerge based on the perceived value they offer to both higher-end and lower-end customers.

- McDonald's and Texas Roadhouse continue to grow comps despite the tough environment thanks to their value-oriented focus that keeps diners coming back.

- Special Report: [Sponsorship-Ad-6-Format3]

The restaurant sector has often been at the forefront of the debate on the K-shaped economy. While consumer sentiment continues to diverge from actual consumer behavior (especially in the retail sector), the foodservice industry is a setting where divergent trends become apparent quickly. The upper end of the "K" continues to indulge, while more cost-conscious consumers at the bottom are searching for value to stretch their dollars.

In this environment, two restaurant companies are standing out for different reasons. The numbers speak for themselves: McDonald’s Corp. (NYSE: MCD) and Texas Roadhouse Inc. (NASDAQ: TXRH) are growing comparable sales and taking share from competitors. Below, we explain why both have thrived in a challenging dining environment and why their stocks could outperform the industry this year.

McDonald's Continues to Dominate the Fast-Food Market

Silver $309? (Ad)

Silver: 20% + 68%

Tim Plaehn just found a Silver ETF that delivers monthly income (up to 20% in annual distributions) plus share appreciation (68% in 5 months). The precious metal has become one of the best investments for growth AND income right now.

The recent earnings reports from McDonald’s and Wendy’s Co. (NASDAQ: WEN) highlighted how players in the fast-food industry are separating themselves.

McDonald’s reported Q4 2025 results last week and beat expectations on both earnings per share (EPS) and revenue, delivering 9.7% year-over-year (YOY) sales growth.

Global same-store sales exceeded expectations with a 5.7% YOY increase, including 6.8% growth in the United States. By contrast, Wendy’s Q4 2025 report showed revenue down 5.5% YOY and U.S. same-store sales falling 11.3%. How has McDonald’s managed to grow U.S. sales at nearly a 7% clip while other quick-service restaurants (QSRs) struggle?

Value — and more value. McDonald’s projects operating margins above 40% in 2026, which gives it the flexibility to pursue its Value Leadership strategy.

Unlike the limited-time promotions used by some competitors, McDonald’s Value Menu 2.0 is a permanent fixture. Extra Value Meals were reintroduced last September, and earlier this year the company launched the McValue platform, which includes $5 Meal Deals and Buy One, Get One for $1 offers. The Grinch Meal holiday promotion drove the biggest single-day sales figure in the company’s long history.

Additionally, the McDonald’s app has about 200 million active users, which helps drive repeat visits. A marketing focus on chicken items such as the McCrispy also reduces sensitivity to beef-price inflation. The company plans to open another 2,600 stores this year, while competitors like Wendy’s are closing underperforming locations.

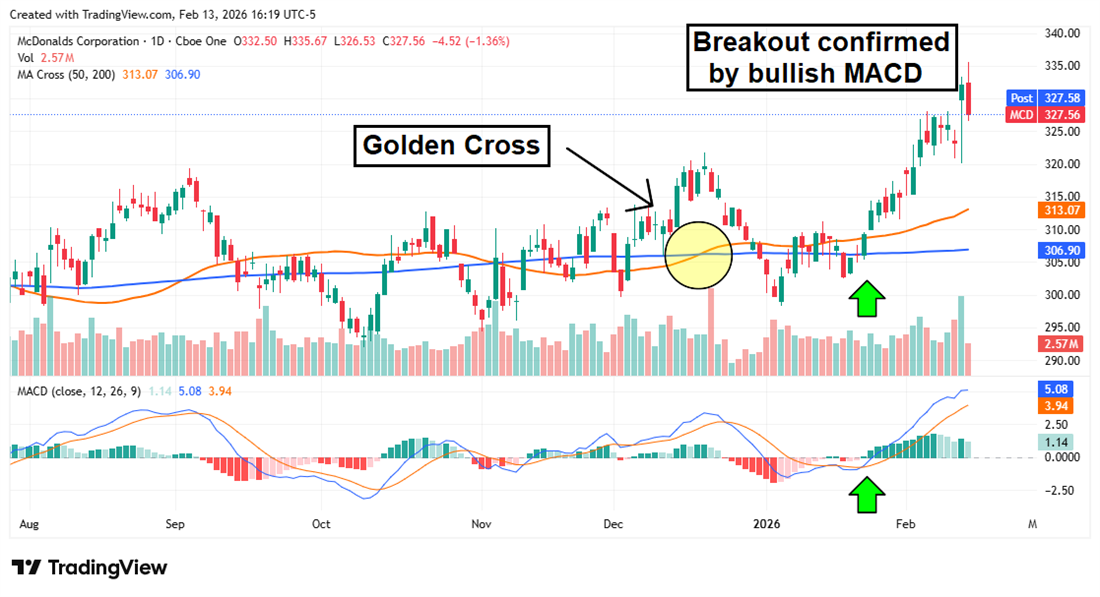

The breakout in MCD shares began well before last week’s earnings. A bullish crossover in the Moving Average Convergence Divergence (MACD) indicator coincided with the stock rising above the 50-day and 200-day simple moving averages (SMAs), signaling strong upward momentum. If lower-income consumers continue to trade down for value, McDonald’s is well-positioned to keep growing sales, supported by both fundamental and technical catalysts in 2026.

Texas Roadhouse Gains Share Despite Commodity Headwinds

Soaring beef prices have cast a shadow over Texas Roadhouse for most of the past year. Beef costs have risen faster than general inflation since the COVID-19 pandemic began, and the surge over the last two years has unnerved restaurant owners and investors alike.

The increase has been driven in part by cattle shortages, which pushed live cow and steer prices to record levels — a trend that is likely to persist into 2027.

Despite this headwind, Texas Roadhouse continues to grow same-store sales faster than many casual-dining rivals.

Texas Roadhouse’s barbell business strategy offers value for cost-conscious customers while also providing premium steaks and upcharge options for diners willing to splurge.

In its Q3 2025 report in November, the company reported comps of 6.1% and nearly 13% YOY revenue growth despite a 224 basis-point increase in food and beverage costs. Texas Roadhouse raised prices by only 1.7% to absorb much of that pressure — a deliberate margin sacrifice to retain value-oriented diners.

Customer experience is a key advantage for Texas Roadhouse. Traffic durability matters for fast-casual chains that depend on repeat visits. Large portions, quick service, streamlined digital kitchens, and a range of add-ons and upgrades create the feel of a special night out without breaking the bank. Many customers say the restaurant is "worth it" for date nights and family dinners because its value and experience meet expectations.

TXRH’s performance so far this year suggests the doldrums of 2025 may be behind it. The stock opened 2026 with an 11-day winning streak, breaking through the 200-day SMA that had previously capped rallies. That streak was followed by consolidation, during which the Relative Strength Index (RSI) cooled to more neutral levels while the 50-day and 200-day SMAs converged.

With a Golden Cross appearing imminent, the 50-day SMA could become support for a renewed rally. That level has already been tested and held once, and the share price is now approaching the 50-day moving average. This could present an attractive entry point for new investors, especially with a catalyst coming when the company reports its Q4 2025 results after the market closes on Feb. 19.

Defense Stocks Are Soaring—AeroVironment's Earnings Could Close the Gap

Reported by Chris Markoch. Posted: 3/2/2026.

Key Points

- AeroVironment stock has dropped roughly 15% in 30 days and trails the SPDR S&P Aerospace & Defense ETF by a wide margin, even as defense spending tailwinds accelerate.

- Revenue through the first half of fiscal 2026 surged 145% year over year, and the company posted a record $3.5 billion in quarterly contract awards.

- Adjusted gross margins fell to 27% from 41% a year ago, and the margin recovery timeline is the key variable heading into March 3 earnings.

- Special Report: [Sponsorship-Ad-6-Format3]

Many aerospace stocks are outperforming the S&P 500 nearly two months into 2026. That's evident in the performance of the SPDR S&P Aerospace & Defense ETF (NYSEARCA: XAR), which is up about 16.2% while the S&P is up just over 1%.

That makes AeroVironment Inc. (NASDAQ: AVAV) a relative laggard in the sector. AVAV is up roughly 5.5% year-to-date, but a sharp selloff over the past month has dragged its short-term performance lower.

Nvidia CEO Issues Bold Tesla Call (Ad)

While headlines focus on Tesla's car sales, tech analyst Jeff Brown says the real story is Tesla's role in a $25 trillion AI revolution — one that Nvidia's CEO himself has called a "multi-trillion-dollar future industry" — and he's uncovered a little-known stock 168 times smaller than Nvidia that could be positioned to ride this breakthrough.

Click here now to see the full reportMore concerning for some investors: XAR is up over 22% in the last three months while AVAV is down more than 8% over the same period. That discrepancy will be in focus as AeroVironment prepares to report earnings on March 3.

Growing in a High-Growth Sector

Most proposals heard in a State of the Union address are rhetorical and often change significantly during the legislative process. Still, policy priorities can signal increased spending in certain areas—something that matters for defense contractors like AeroVironment.

AeroVironment specializes in three main areas:

- Unmanned Aerial Systems (UAS)

- Tactical missiles and precision loitering munitions

- Electric vehicle charging and scalable energy systems

All three are part of the next-generation defense technologies the Trump administration has proposed funding as it seeks to rebuild U.S. defense capabilities. That commitment is already showing up in AeroVironment's revenue.

Through the first two quarters of AeroVironment's 2026 fiscal year, revenue is up 145% year-over-year (YOY).

In its Q2 FY2026 earnings report, AeroVironment guided to full-year revenue between $1.95 billion and $2.0 billion, which would more than double first-half results. The strong top-line performance was driven by demand for the company's drone and precision-strike products, and the company set an all-time record with $3.5 billion in contract awards during the quarter.

Additionally, those guidance figures don't factor in a geopolitical risk that could further boost demand: the potential for U.S. military action involving Iran, which would likely employ products and services AeroVironment provides.

Can Earnings and Margins Catch Up?

For many growth stocks, valuation hinges on when revenue growth translates into stronger earnings. For AeroVironment, that question centers on margins.

Adjusted gross margins fell to 27%, down from 41% in the same quarter last year. Three factors contributed:

- Implementation of a major new Oracle financial system mid-quarter, which created one-time inefficiencies and extra costs.

- A shift in the revenue mix toward lower-margin services following the BlueHalo acquisition.

- A prolonged U.S. government shutdown that delayed product shipments, including some international sales, hurting higher-margin product revenue.

Management expects margins to recover into the high 30% range by Q4, citing a ramp-up in product revenues, stabilization of the software transition, and the flow of pent-up government orders.

If that outlook holds, it would support analysts' forecasts for roughly 31% earnings growth over the next 12 months, which would help justify the company's current valuation of about 15x sales.

Bullish Sentiment Could Signal an Earnings Beat

AeroVironment is covered by 23 analysts and has a consensus rating of Moderate Buy, with 20 of 23 analysts rating the stock Buy. The consensus price target is $367, about a 42% increase from the AVAV share price at the time of writing. Institutional buying has also outweighed selling by nearly a 2:1 margin over the last 12 months.

The consensus forecast for adjusted EPS is $0.73, while the whisper number is about $0.66, implying some analysts view the consensus as somewhat optimistic. Even using the whisper number, however, EPS would more than double year-over-year from the prior period—a level of YOY earnings growth that has not yet appeared in AeroVironment's first two quarterly reports this fiscal year.

This email message is a paid sponsorship provided by The Oxford Club, a third-party advertiser of InsiderTrades.com and MarketBeat.

This ad is sent on behalf of The Oxford Club. 105 W Monument St, Baltimore, Maryland 21201. If you would like to optout from receiving offers from The Oxford Club please click here

If you need assistance with your newsletter, please don't hesitate to email MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from InsiderTrades.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC.

345 North Reid Place, Suite 620, Sioux Falls, South Dakota 57103. United States of America..

No comments:

Post a Comment