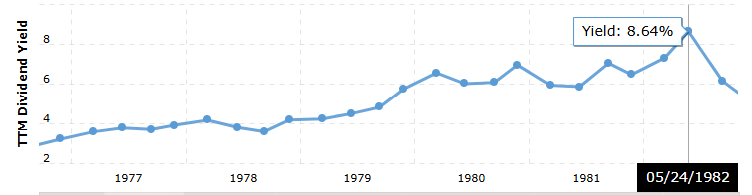

Back in the day, you could park your cash in a stock and yield hefty 8% dividend checks…

Giving you capital gains and cash flow to offset rising costs.

A standard $250k retirement account would’ve seen healthy market returns.

But in today’s market… you’re lucky to get much more than 1% in dividends.

So chasing dividends might look like a dead game… if you don’t know a smarter way to find solid stocks.

Picking the right stocks keeps you on the right track…

And gives you more shots to reap returns over time.

That’s why I had to get these 5 dividend-investing cheat sheets to you.

After more than a decade trading the markets, and having contacts which include a former hedge fund manager, a trading champion, and a former bank VP…

I believe everything you’ll see inside will give you a special look at how to go after dividend stocks.

You’ll get to see every single detail I look for before I even touch any stock for dividends…

In fact, you’ll get the two dividend stocks I personally put $50,000 of my own money into.

No reckless guarantees when it comes to trading, of course.

But before you load up on another dividend stock next…

Check out these cheat sheets… free.

By clicking the link above you agree to periodic updates from ProsperityPub and its partners (privacy policy)

IonQ Just Delivered the Quarter That Changes the Quantum Narrative

Reported by Jeffrey Neal Johnson. Posted: 2/26/2026.

Key Points

- IonQ beat revenue expectations in the quarter and raised its forward guidance well above Wall Street expectations.

- The company maintains a substantial cash position that insulates operations from dilution while enabling aggressive investment in strategic growth.

- New acquisitions in sensing and manufacturing have positioned the company to secure major national security contracts and expand its commercial platform.

- Special Report: [Sponsorship-Ad-6-Format3]

Wall Street was caught off guard on Thursday, Feb. 26, as shares of IonQ (NYSE: IONQ) rallied, climbing more than 19% to clear the $40 level. The gain in IonQ's share price followed the company's fourth-quarter and full-year 2025 earnings report, which beat analyst expectations and shifted the narrative for the broader quantum computing sector.

For years, quantum computing was often characterized as a long-term science project—high potential but little current revenue. IonQ's latest results challenge that view. The company reported fourth-quarter revenue of $61.9 million, beating its own guidance midpoint by 55% and marking a 429% year-over-year increase.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

This appears to be a financial inflection point. Investors are now looking at a business generating meaningful revenue today rather than solely promising breakthroughs down the road. The market's reaction suggests IonQ is transitioning from a research lab into a scalable commercial platform.

Doubling Down: Revenue Forecast Signals Hypergrowth

While the recent quarter was impressive, the stock's rally is driven largely by the outlook. Management surprised the market by raising full-year 2026 revenue guidance to $225 million–$245 million.

To put that in context, the forecast sits well above prior Wall Street consensus. It implies IonQ expects to nearly double annual revenue again in 2026 after tripling revenue in 2025.

Key Financial Highlights:

- Q4 Revenue: $61.9 million (Up 429% YOY)

- Fiscal Year 2025 Revenue: $130.0 million (Up 202% YOY)

- Fiscal Year 2026 Outlook: $225 million - $245 million

This accelerating growth curve is uncommon in hardware-focused companies. It points to rising demand for IonQ's offerings as commercial and government clients move from pilots to large-scale deployments. While some analysts remain cautious about valuation multiples, this revenue momentum forces a re-evaluation. In a market hungry for growth, IonQ is delivering results that are difficult to ignore.

A $3.3 Billion Fortress: The Cash Advantage

Scaling deep-technology businesses is expensive. IonQ is not yet profitable on an adjusted EBITDA basis and projects an adjusted loss of $310 million–$330 million for 2026. Normally, a burn rate of that magnitude would raise concerns about dilution and financial strain.

But IonQ entered 2026 from a position of strength: it ended 2025 with pro-forma cash, cash equivalents, and investments totaling roughly $3.3 billion.

Why This Matters:

- No Dilution Risk: Unlike many quantum peers racing against a liquidity clock, IonQ has the capital to fund operations for years without issuing new equity.

- Interest Income: A cash pile this size generates meaningful interest income in the current environment, helping offset operating losses.

- Strategic Flexibility: The war chest lets IonQ invest aggressively in supply chains, talent, and acquisitions while competitors may be forced to cut costs.

This balance-sheet strength creates a significant strategic moat. It reduces the bankruptcy risk in the bear case and lets investors focus on the growth story.

Vector Atomic & SkyWater: Defense Wins That Change the Game

The revenue surge is not just due to faster machines; it reflects IonQ's move to a Quantum Platform strategy. The company is selling integrated solutions that combine computing, networking, and sensing rather than merely providing access to experimental hardware.

The Vector Atomic Acquisition

Completed in the third quarter of 2025, the Vector Atomic deal brought advanced quantum sensing and timing technologies in-house. That matters because GPS jamming and other disruptions are immediate threats in modern warfare; Vector Atomic's technology enables precise navigation and timing without relying on satellites.

That strategic value was reinforced when IonQ was selected for the Missile Defense Agency's (MDA) SHIELD IDIQ contract, demonstrating the technology's maturity for national-security applications and moving it into active defense budgets.

The SkyWater Technology Deal

The pending acquisition of SkyWater Technology is equally strategic. Securing a U.S.-based manufacturing supply chain aligns IonQ with national priorities around onshoring critical technologies. Owning manufacturing increases scalability and trust, positioning IonQ as a stronger contender for sensitive government programs like the Golden Dome initiative.

Why the Stock Could Keep Climbing

Beyond the fundamentals, market mechanics are amplifying the move. IonQ has been a popular short, and ahead of the earnings report many traders were betting against it.

The Setup:

- Short Interest: Approximately 25.14% of IonQ's floating shares are currently sold short.

- Days to Cover: The short ratio is about 3.7, meaning it would take nearly four days of average trading volume for short sellers to buy back their positions.

When a highly shorted stock posts a big earnings beat and raises guidance, it creates a powder keg. Rising prices force mark-to-market losses on short positions, prompting cover buying that pushes the stock even higher.

With a 19% jump in a single session, many short sellers are now underwater. If the stock sustains these levels, continued volatility is likely as positions are unwound — a dynamic that can drive the stock toward the higher price targets some bullish analysts have set.

Separating From the Pack

IonQ has made a decisive statement. By pairing triple-digit revenue growth with a robust balance sheet and critical defense contracts, the company is distinguishing itself within the quantum sector.

Risks remain — notably the path to long-term profitability and the timeline for fault-tolerant computing — but strong commercial execution provides a firmer floor for the stock. With bullish firms like Rosenblatt issuing price targets as high as $100 and short sellers rushing to cover, the market appears to be recognizing IonQ not just as a research experiment, but as the sector's first genuine commercial heavyweight.

Will the Super Mario Movie Make It Showtime for Nintendo Stock?

Reported by Chris Markoch. Posted: 3/7/2026.

Key Points

- Nintendo sold 15 million Switch 2 consoles in months, but NTDOY stock still needs a catalyst to break resistance.

- The upcoming Super Mario movie sequel could boost high-margin IP revenue and revive investor sentiment.

- Strong cash reserves and a dividend provide downside support as investors watch for a technical breakout.

- Special Report: [Sponsorship-Ad-6-Format3]

Mario and Luigi are two of the most iconic characters in the Nintendo Co. Ltd. (OTCMKTS: NTDOY) universe. Nintendo is counting on the brothers to help it capitalize on their popularity with the upcoming "Super Mario Galaxy" movie, scheduled for release in April.

The film follows the 2023 Super Mario Bros. Movie, which surprised some observers by becoming a box-office hit and boosting sales of Nintendo intellectual property (IP).

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

It's not surprising, then, that Nintendo hopes the sequel will be as popular — or even more so — than the original. The movie's release is timed to arrive roughly one year after Nintendo launched its Switch 2 console.

In its most recent earnings report, Nintendo highlighted cumulative global sell-through of 15 million Switch 2 units as of the fourth week of December 2025, making it the fastest-selling dedicated video game platform the company has released.

The Year of Super Mario Becomes a Strategic Push

Ahead of the movie, Nintendo is set to release Super Mario Bros. Wonder, a title exclusive to the Switch 2. That's one of several initiatives planned for the 40th anniversary of Super Mario Bros.

This fits Nintendo's broader strategy of leaning into its IP as a revenue stream that can help smooth the lumpiness of console sales. IP revenue still represents a small share of total sales; for example, in the first nine months of the company's 2026 fiscal year, Nintendo reported ¥54.5 billion in IP-related revenue.

That amounted to about 3% of the company's overall sales over that period. While a modest slice of revenue, IP income tends to flow directly to the bottom line.

Tariffs, AI, and Geopolitical Risks Add Uncertainty

Even before the Switch 2 launched, Nintendo faced challenges from tariffs and has mitigated some of those pressures by shifting production to Vietnam.

Concerns also grew about a potential slowdown in Nintendo's earnings, which are increasingly affected by memory-chip prices. Supporting that view, the company reported declining year-over-year (YOY) operating margins through the first three quarters of its 2026 fiscal year.

That is the downside. The upside is that the Switch 2, like its predecessor, enjoys a multi-year sales window. Even after brisk initial demand, there remains a large addressable market that could receive a boost when the new Mario movie hits theaters.

Another worry is how artificial intelligence (AI) might change the gaming sector. Some fear Nintendo could lose revenue as individuals create games using agentic AI. While user-generated AI creations will grow, many consumers will likely prefer polished, professionally made experiences. That dynamic puts Nintendo in a good position, particularly if it leverages AI to accelerate internal game development.

Since the earnings report, a further concern has been the conflict in the Middle East involving the U.S., Israel and Iran. That could delay some Switch 2 shipments, which move by sea.

NTDOY Stock Needs Technical Confirmation

Nintendo stock has been a volatile investment over the past 12 months. The 52-week range for NTDOY is $13.05 to $24.92. The 52-week high coincided with a two-month surge that peaked in mid-August after the June release of the Switch 2. Since then, the chart has shown a generally bearish pattern, although this does not look like a classic "falling knife"; the stock appears to have found a bottom around the earnings report.

When a meaningful turnaround might occur is unclear. The 50-day simple moving average (SMA) has acted as resistance and stalled upward momentum in early March. Investors would want to see a breakout above that level on strong volume to confirm a reversal.

The best-case scenario for Nintendo is an improving U.S. economy, which would lift consumer discretionary stocks broadly and could prompt consumers who delayed buying a Switch 2 to become buyers. A swift, orderly resolution of geopolitical tensions and clearer tariff dynamics would also strengthen the case for the business.

Those developments could take a quarter or more to play out. In the meantime, Nintendo pays a steady dividend and holds more than $15 billion in cash on its balance sheet, alongside a market capitalization of roughly $73 billion as of this writing.

This email is a paid sponsorship from ProsperityPub, a third-party advertiser of InsiderTrades.com and MarketBeat.

If you need assistance with your account, feel free to contact MarketBeat's U.S. based support team at contact@marketbeat.com.

If you no longer wish to receive email from InsiderTrades.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Place, Suite 620, Sioux Falls, S.D. 57103. USA..

No comments:

Post a Comment