Last century, the world's power was forged in oil refineries.

Today, that leverage has shifted to rare earth processing.

We are at a historic Rockefeller Moment, where the company that controls the midstream controls the future of global industry.

While others focus on the "dirt" of mining, REalloys (NASDAQ: ALOY) is building the refineries.

Digging minerals out of the ground is relatively easy. Turning them into finished metals and alloys for fighter jets, drones, missile guidance systems, and advanced radar is something else entirely.

That step, where strategic independence is actually won or lost, barely exists outside China.

By advancing the first integrated North American pathway from mining to finished magnets, the company is working to secure a vulnerable domestic supply chain.

Every critical step happens on North American soil - with no Chinese chemicals, technology, or capital.

When it comes to rare earths, 1% reliance on China is 100% reliance on China.

Western defense production cannot depend on a supply chain that can be shut off at any time.

REalloys is building one that can't.

Read the full REalloys (NASDAQ: ALOY) breakdown.

Tomorrow Investor

Diamondback Sees Resilient Demand Despite Cautious Guidance

Reported by Chris Markoch. Article Published: 2/26/2026.

Key Points

- Diamondback Energy’s disciplined production outlook signals a supply environment that could help support higher oil prices into 2026.

- Strong free cash flow is funding dividend growth and share repurchases, reinforcing the company’s shareholder-return story.

- FANG stock remains technically constructive, with analysts projecting moderate upside as energy sentiment improves.

- Special Report: [Sponsorship-Ad-6-Format3]

Diamondback Energy Inc. (NASDAQ: FANG) stock has almost recovered all its pre-market losses following its Q4 2025 earnings report on Feb. 23. The headline numbers were mixed, with a slight earnings miss offset by a topline beat. However, the company issued cautious guidance that may have dampened initial enthusiasm.

It's a reminder that investors tend to reward companies that underpromise and overdeliver — once they actually overdeliver. Still, there was a lot to like in Diamondback's report, including a more optimistic view on the supply-demand outlook for crude oil in 2026.

Buy this stock tomorrow? (Ad)

Not a Single "Mag 7" on This Legendary Investors List

A renowned former hedge fund manager – friends to some of the biggest investors in the world – just released a new list of his favorite AI stocks... and not a single Magnificent 7 name made the cut. Instead, an AI stock you've likely never heard of just flagged as "near-perfect" in his new investing scoring system.

Diamondback believes demand will remain resilient. However, its initial 2026 guidance is cautious, projecting output roughly in line with the final three months of 2025. That forecast may not fully account for potential crude-price appreciation in the coming months.

Disciplined Production Could Support Higher Oil Prices

As of this writing, the April contract price of West Texas Intermediate (WTI) crude oil is $65.94 — about 20% higher than at the start of the year and roughly 40% above some analysts' expectations.

Rising crude prices have lifted the energy sector, but persistent concerns about a supply glut still weigh on oil producers, particularly those responsible for getting oil out of the ground.

In its report, Diamondback noted that demand has remained resilient, suggesting December 2025 may have helped put a floor under crude oil prices.

Several items in Diamondback's presentation support the case for a sustained move higher in crude. First, the company's 2026 production guidance of 500–510 Mbo/d represents only modest growth from 2025 levels, signaling a disciplined, industry-wide posture that could keep supply from overwhelming demand.

Second, Diamondback's scenario analysis shows that even at $70 per barrel the company expects to generate over $5.5 billion in free cash flow. That suggests management views meaningful upside from current prices as a realistic base case, not a stretch target.

There is also a structural gas story that could indirectly support oil prices. Diamondback is aggressively expanding its long-haul gas pipeline commitments, raising its forecast from roughly 350,000 MMBtu/d today to 800,000 MMBtu/d by Q4 2026. That expansion would reduce the WAHA pricing drag that has historically weighed on Permian producers' realizations. As that headwind fades, the economics of Permian production improve, reinforcing the case for continued capital discipline across the basin. Fewer wells drilled industry-wide would mean tighter supply, which tends to push prices higher.

Dividend Growth Reinforces Long-Term Investor Appeal

The cyclical nature of energy — and oil in particular — helps explain why many companies in the sector pay attractive dividends.

A highlight of Diamondback's report was its announcement of a 5% increase in its quarterly dividend. This marks the seventh consecutive year of dividend increases for the company.

That dividend appears to be well supported by the company's growing free cash flow (FCF).

The company says the dividend is sustainable as long as crude oil prices remain above approximately $37 per barrel.

Diamondback also announced it repurchased approximately 2.9 million shares in Q4 and has about $2.3 billion remaining on its authorized $8 billion share repurchase program.

Technical Indicators Point to Consolidation, Not Reversal

On Feb. 20, the last trading day before its earnings report, FANG stock popped to its 52-week high, the culmination of a rally that began at the start of the year.

That rally mirrors moves across many energy stocks, which have been range-bound for several years as demand hasn't kept pace with record output. In that context, any small miss — like the slight earnings shortfall here — was likely to trigger a pullback.

Volume is slightly above average on the day, and the initial slip appears to have been driven by algorithmic trading. Traders began buying the dip midway through the session.

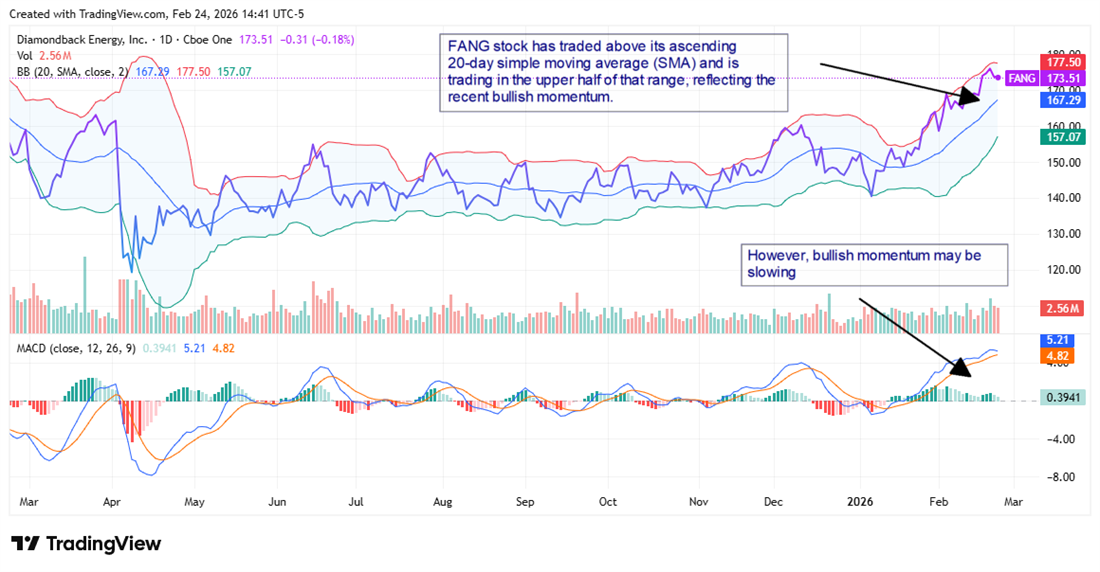

FANG has remained above its rising 20-day simple moving average (SMA). The Bollinger Bands are also notable: the upper band sits at $177.50 and the lower band at $157.07, and the stock — at $173.51 — is trading in the upper half of that range, reflecting recent bullish momentum.

The moving average convergence/divergence (MACD) also paints a broadly constructive picture: the MACD line at 5.21 remains above its signal line at 4.82, though the narrowing gap suggests near-term momentum may be fading. Momentum appears to be slowing, which could mean the stock pulls back toward the SMA — currently around $167.29 — before its next move.

The Diamondback Energy analyst forecasts on MarketBeat give the stock a consensus price target of $187.33, roughly an 8% upside from its current price. Sentiment has been bullish year-to-date and remained so after the earnings release, with TD Cowen upgrading FANG to a Strong Buy.

Axon Got Caught in the SaaS Crash—Its Earnings Say That Was a Mistake

Reported by Leo Miller. Article Published: 2/26/2026.

Key Points

- Axon shares surged after Q4 earnings, snapping a months-long selloff that had cut the stock roughly in half from its all-time high.

- The broader SaaS panic dragged Axon down alongside pure software names, but the company's hardware-integrated model may make that comparison a poor one.

- Analysts still see meaningful upside even after trimming their price targets post-report.

- Special Report: [Sponsorship-Ad-6-Format3]

After getting battered in the second half of 2025 and early 2026, shares of defense company Axon Enterprise (NASDAQ: AXON) have suddenly rebounded. Following its Q4 financial results on Feb. 24, Axon shares jumped nearly 18% the next day.

Axon hit an all-time high closing price near $871 last August. Before this earnings report, the stock had fallen roughly 50% from that peak.

Silver $309? (Ad)

Silver: 20% + 68%

Tim Plaehn just found a Silver ETF that delivers monthly income (up to 20% in annual distributions) plus share appreciation (68% in 5 months). The precious metal has become one of the best investments for growth AND income right now.

Even after the recent rally, many Wall Street analysts remain bullish on the company.

So, what drove Axon's steep sell-off, and are the concerns about the firm really warranted?

Axon's Sky-High P/E, SaaS Fears Come to Roost

Axon's forward price-to-earnings (P/E) ratio was extremely elevated — it peaked near 130x in August — and that certainly contributed to the sell-off. The company was also swept up in the 2026 "SaaSpocalypse," which accelerated its decline.

Prior to the latest release, Axon shares were down more than 20% in 2026. Many of the stock's largest single-day drops coincided with the biggest declines across the software industry, suggesting AI-displacement fears that hit the sector broadly also weighed on Axon.

That said, the simultaneous sell-off appears indiscriminate. Investors were selling software-related names en masse rather than assessing AI disruption risk on a company-by-company basis.

Why Axon's Hardware-to-Software Flywheel Provides Protection From AI

Axon benefits from a simple reality: law enforcement depends on physical intervention. AI can't physically restrain or arrest someone, which limits AI-disruption risk among Axon's core customers, law enforcement agencies.

Yes, Axon has a sizable software business that could theoretically face AI-related competition. But hardware remains central to its strategy. Consider the product that made Axon relevant in the first place: tasers. These are physical devices the company has developed for more than three decades — an AI startup can't replicate them with "vibe-coding."

Taser sales grew 32% in Q4 2025 and accounted for about one-third of Axon's full-year revenue, keeping a large portion of the business relatively insulated from AI disruption.

Also, Axon's software is tightly integrated with its hardware. Body cameras capture video that's stored on its digital evidence management platform, generating recurring subscription revenue. Other software products rely heavily on data produced by those cameras.

For example, Draft One creates an initial draft of an officer's incident report from body camera audio, saving time compared with fully manual report writing and allowing officers to focus more on preventing and investigating crime.

To displace Axon's software, a competitor would likely need to replace its body-cam ecosystem as well. That would require agencies to rip out established systems, retrain personnel, and risk scrutiny if new systems mishandle evidence. Axon's long-standing relationships and trust with agencies make that a substantial barrier.

As Axon collects more data from its devices, its software should only improve. That accumulated device data gives the company a head start against would-be competitors.

Analysts Eye +20% Upside After Axon's Big Beats

Axon's latest results reinforce the strength of its business. The company beat expectations on both sales and adjusted earnings per share (EPS), with revenue up 39%. Future contracted bookings — the value of signed contracts yet to be fulfilled — rose 43% to $14.4 billion. That backlog is large compared with the $2.8 billion in total revenue Axon generated in 2025, though it is not guaranteed revenue.

Axon also posted a highly impressive net revenue retention rate of 125%, meaning existing customers increased their spending by 25% year over year — a sign that Axon's offerings are delivering growing value.

By 2028, Axon is targeting revenue of $6 billion, implying roughly 29% annual growth over the next three years. The company also aims to expand its adjusted EBITDA margin by 250 basis points to 28%.

The MarketBeat consensus price target for Axon sits near $763, which would imply more than 45% upside from recent levels. After the company's report, analysts lowered many price targets; the average of those updated targets is closer to $654, still implying roughly 25% upside. Those reductions largely reflect adjustments following the stock's sharp fall, not an unfavorable read of the earnings results themselves.

Overall, Axon's outlook looks promising, and fears about AI-driven disruption to this business appear overstated.

This email content is a paid advertisement for The Tomorrow Investor, a third-party advertiser of InsiderTrades.com and MarketBeat.

This message is a paid advertisement for REalloys (NASDAQ: ALOY) from The Tomorrow Investor and Think Ink Marketing. MarketBeat Media, LLC receives a fixed fee for each subscriber that clicks on a link in this email, totaling up to $4,500. Other than the compensation received for this advertisement sent to subscribers, MarketBeat and its principals are not affiliated with either The Tomorrow Investor or Think Ink Marketing. MarketBeat and its principals do not own any of the stocks mentioned in this email or in the article that this email links to. Neither MarketBeat nor its principals are FINRA-registered broker-dealers or investment advisers. The content of this email should not be taken as advice, an endorsement, or a recommendation from MarketBeat to buy or sell any security. MarketBeat has not evaluated the accuracy of any claims made in this advertisement. MarketBeat recommends that investors do their own independent research and consult with a qualified investment professional before buying or selling any security. Investing is inherently risky. Past-performance is not indicative of future results. Please see the disclaimer regarding REalloys (NASDAQ: ALOY) on Think Ink Marketing' website for additional information about the relationship between Think Ink Marketing and REalloys (NASDAQ: ALOY).

If you need assistance with your subscription, please don't hesitate to email our U.S. based support team at contact@marketbeat.com.

If you no longer wish to receive email from InsiderTrades.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Place #620, Sioux Falls, S.D. 57103-7078. USA..

No comments:

Post a Comment