Dear Reader,

I started rating the safety of banks in the early '70s.

Over the last 50+ years, I've warned my readers about the bank failures of the 1980s and 1990s, the Dot-Com Bust, the 2008 housing collapse and more.

But today, I'm writing to you with a different kind of warning. One that genuinely frightens me.

This time, the threat to your money isn't coming from reckless Wall Street bankers. It's coming directly from the Federal Reserve itself.

Through a program outlined in the Federal Reserve Docket No. OP-1670 — known as "FedNow" — the government is quietly rewiring the entire American banking system.

Simply stated, the Fed is building a centralized hub that will process every transaction in the U.S. … giving it the ability to track every transfer, bill pay, purchase or donation you make in real time.

That, in turn, could give them unprecedented power to cut off your access to your savings if they decide you're not in "compliance" with whatever their policy agenda dictates at the time.

Or maybe even confiscate your savings when the need arises like it happened in Cyprus in 2013.

In all my decades studying the U.S. economy and banking system, I've never seen anything as scary as this.

If you value your financial privacy …

If you believe your money belongs to you and not Washington …

Now's the time to act.

I've spent the last few months putting together 4 specific, legal steps to "Fed-proof" your checking and savings accounts.

I urge you to take this threat seriously.

Review these 4 steps immediately, right here.

Good luck and God bless!

Martin D. Weiss, PhD

Weiss Ratings Founder

P.S. The Fed is counting on the fact that ordinary Americans won't read a 93-page document until it's too late. I've read it and that's why I'm begging you to act while you still can. Get the 4 "Fed-proof" steps right now.

Workday, Seriously, It's Time to Buy This SaaS Leader

Author: Thomas Hughes. Published: 2/26/2026.

Key Points

- Workday is on track to hit multiyear lows amid a fear-driven sell-off; its stock oversold to deep value territory.

- AI disruption fears are overblown; this company is growing and cementing itself as an AI automation leader.

- Institutions buy as price action declines, and even analyst trends reveal the value.

- Special Report: [Sponsorship-Ad-6-Format3]

Workday's (NASDAQ: WDAY) stock decline did not end after its Q4 2025 earnings — it pushed to multi‑year lows, creating a more attractive opportunity for investors. Although guidance missed consensus and AI disruption fears persist, the miss was small, guidance remains solid, and disruption may not unfold the way the market expects.

AI‑first companies may try to enter Workday's territory by turning models into full HR and finance software, but incumbents like Workday are embedding AI into their existing platforms. Because they are deeply integrated into enterprise workflows and data, they may be harder to displace than the market fears.

Silver $309? (Ad)

Silver: 20% + 68%

Tim Plaehn just found a Silver ETF that delivers monthly income (up to 20% in annual distributions) plus share appreciation (68% in 5 months). The precious metal has become one of the best investments for growth AND income right now.

The analyst response to the earnings release was generally negative. Jefferies downgraded the stock to Hold and several firms trimmed price targets, noting the abrupt CEO change: co‑founder and Executive Chairman Aneel Bhusri is returning to lead the company through its next phase.

Workday Accelerates Growth and Profitability in Q4 2025

Workday delivered a solid Q4, with revenue growth accelerating sequentially to 14.5%. Revenue of $2.53 billion topped MarketBeat's reported consensus by 40 basis points, driven by subscription strength (up 15.7% year‑over‑year), and that strength carried through to the bottom line.

Margins also improved: GAAP and adjusted operating margins widened by several hundred basis points. Adjusted operating margin expanded by 420 basis points, contributing to a 32% increase in operating income and a 28% rise in adjusted earnings — about 650 basis points better than expectations on the margin side.

Guidance was the primary concern: Q1 and full‑year 2026 revenue forecasts came in below consensus. Still, the company projects 13% topline growth in Q1, 12.5% for the year, and a healthy adjusted operating margin. Price action may reset, but it is unlikely to stay depressed for long. WDAY's consensus target sits roughly 100% above critical support levels, and even the low end of the range suggests upside.

Institutional Support and Share Buybacks Underpin WDAY Rebound Outlook

Two factors supporting a potential rebound are Workday's capital returns and strong institutional ownership. Capital returns are driven entirely by share repurchases, which steadily reduce the share count. 2025 repurchases trimmed the float by roughly 0.4%, helping improve shareholder leverage, and institutional investors are adding to positions.

Institutions own more than 90% of the stock and have been accumulating for seven consecutive quarters, including the first two months of Q1 2026. Net flows in Q1 2026 were about $1.15 bought for every $1 sold — modest but bullish — and the increase in buying to offset selling suggests institutions may continue purchasing despite the "tepid" guidance.

Workday's balance sheet reflects the impact of buybacks, acquisitions, and growth investments, but it shows no red flags. Cash balances remain healthy and flat year‑over‑year, and a dip in current assets is offset by an increase in total assets. Liabilities are up, which compressed equity, but leverage remains light — roughly two times cash and under 0.5 times equity — leaving an easy path to reduce debt and improve equity through 2026.

Catalyst for Workday Stock: Yes, They Exist

Catalysts for Workday in 2026 include sustained revenue growth, improving cash flow, and the potential to outperform conservative guidance. Management cited macroeconomic uncertainty and longer deal‑closing timelines, which led to a cautious outlook. If Workday consistently beats quarterly expectations, guidance and analyst sentiment could improve, prompting a rebound. Trading near $115, WDAY sits at levels not seen since the depths of the COVID‑19 panic, which increases the reward potential for patient investors.

Why eBay's Depop Acquisition Matters More Than the Earnings Beat

Authored by Chris Markoch. Originally Published: 2/20/2026.

Key Points

- eBay’s Q4 beat and GMV acceleration support a comeback narrative, even as the stock remains pressured by broader “AI trade” sentiment.

- Advertising and recommerce are emerging as durable growth engines, while Depop adds a targeted Gen Z/Millennial wedge.

- Depop integration costs, cyclical category tailwinds, and margin pressure remain the main risks to watch.

- Special Report: [Sponsorship-Ad-6-Format3]

Shares of eBay Inc. (NASDAQ: EBAY) rose about 3.8% the day after the company delivered a strong Q4 2025 earnings report. On one level, the results make sense: eBay is a pure-play on consumer spending, which has remained resilient despite conflicting macroeconomic signals. It also fits into the "discount" category of retail stocks that has performed relatively well in a volatile market.

There was a lot for investors to like. Revenue of $2.97 billion exceeded expectations of $2.87 billion. A key metric, gross merchandise volume (GMV), climbed to $21.2 billion — up almost 6% globally and nearly 10% in the United States — suggesting the platform is expanding and attracting more customers.

Silver $309? (Ad)

Silver: 20% + 68%

Tim Plaehn just found a Silver ETF that delivers monthly income (up to 20% in annual distributions) plus share appreciation (68% in 5 months). The precious metal has become one of the best investments for growth AND income right now.

Another headline from the report was the announcement that eBay will acquire Depop, the secondhand clothing marketplace owned by Etsy Inc. (NASDAQ: ETSY), for $1.2 billion in cash. The move is a strategic play to capture more Gen Z and Millennial customers.

Like many stocks with even minimal exposure to artificial intelligence (AI), EBAY had been trading lower in 2026 before the report. One solid quarter won't erase that pressure, but there are several reasons to believe in eBay's comeback.

Ads, Fashion, and the Recommerce Angle

The Q4 report highlighted three specific engines doing the heavy lifting. The first is advertising. On an annualized basis, eBay is approaching $2 billion in ad revenue — a stream that was almost non-existent five years ago.

Total advertising revenue was $544 million in Q4, representing GMV penetration of nearly 2.6%, with first-party ads growing over 17% to $517 million. About 4.8 million sellers adopted at least one promoted listing product during the quarter. The takeaway is that advertising is becoming embedded behavior on the platform, not just an optional feature for power sellers.

The second growth engine is recommerce (pre-owned and refurbished merchandise). This category accounted for more than 40% of the company's GMV in 2025 and grew roughly 10% during the year. It's an area where eBay differentiates itself from Amazon.com Inc. (NASDAQ: AMZN), and one Amazon would find difficult to replicate at meaningful scale.

The third engine is the Depop acquisition. In 2025, Depop generated roughly $1 billion in gross merchandise sales for Etsy, and nearly 90% of Depop's 7 million active buyers are under 34 — a demographic eBay has struggled to attract. Depop also specializes in private-label fashion, one of the fastest-growing segments in retail. If those shoppers migrate to eBay, the platform could gain a credible foothold that drives future revenue growth.

A Marketplace Revamp With Real Teeth—or Temporary Tailwinds?

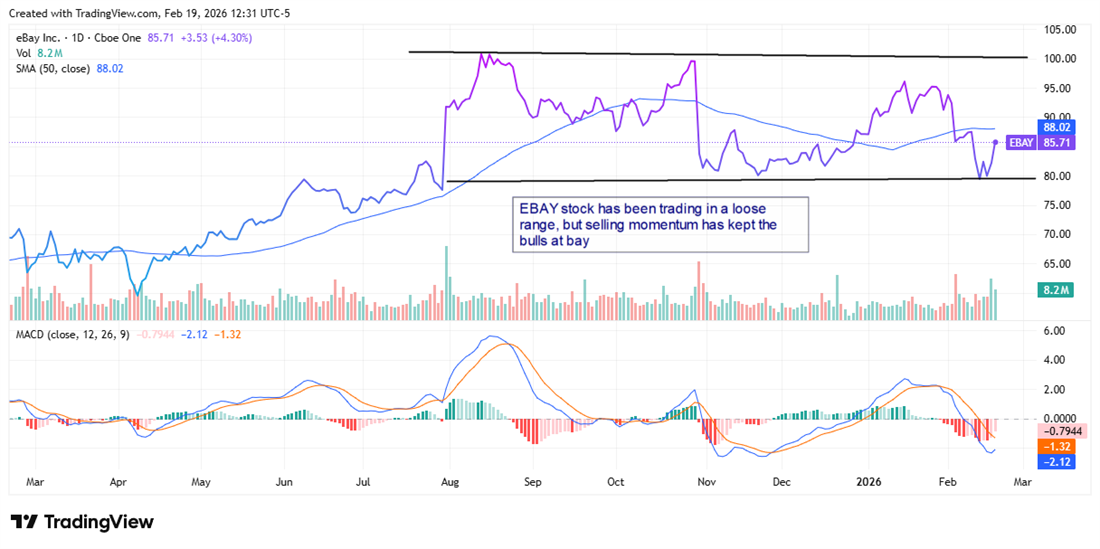

Institutional sentiment on EBAY has been bearish over the last three quarters, with selling outweighing buying by about $2 billion. Some of that selling followed the stock's all-time high in August 2025. Since then, EBAY has traded in a loose range, with support near $80 and resistance around $100.

That said, the eBay analyst forecasts on MarketBeat show analysts have been quick to raise price targets on EBAY. Several of the new targets exceed the consensus price of $96.52 — roughly a 12% premium to the stock price at the time of writing. Needham & Company now has the highest target, raising it to $122 from $115.

Investors should also note the company's dividend. A dividend alone isn't a compelling reason to buy a growth-oriented name like eBay; investors should prefer that the company continue investing in growth, as it is doing with the Depop deal.

Still, the dividend yield of 1.35% is above the S&P 500 average. eBay's annual dividend is $1.16, and the company has raised payouts at an average rate of more than 14% over the past three years. The payout ratio of roughly 25% appears sustainable and is not unduly draining cash.

Risks That Investors Shouldn't Ignore

While the bull case is compelling, several risks merit attention. First, some of Q4's GMV growth reflected commodity-driven categories. Management acknowledged on the earnings call that bullion, collectible coins, and Pokémon trading cards provided meaningful tailwinds in late 2025 — categories that are cyclical and may not repeat at the same pace.

Second, the Depop deal, while strategically logical, comes with near-term costs. eBay expects the acquisition to be a low single-digit headwind to non-GAAP operating income growth and to dilute EPS in the near term, with accretion not forecast until 2028.

Third, non-GAAP gross margin slipped nearly 80 basis points year over year. Sustainable margin expansion in the face of Amazon's logistics heft and Shopify's (NASDAQ: SHOP) seller ecosystem remains the central question weighing on EBAY. Management attributes the dip mostly to scaling managed shipping and Authenticity Guarantee programs — necessary investments that underscore the real costs of protecting trust on a peer-to-peer marketplace.

This email is a sponsored message from Weiss Ratings, a third-party advertiser of MarketBeat. Why did I get this email content?.

11780 US Highway 1,

Palm Beach Gardens, FL 33408-3080

Would you like to edit your e-mail notification preferences or unsubscribe from our mailing list?

If you have questions about your newsletter, please don't hesitate to email our South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

Copyright 2006-2026 MarketBeat Media, LLC.

345 N Reid Pl., Sixth Floor, Sioux Falls, South Dakota 57103-7078. United States of America..

No comments:

Post a Comment