Dear Reader,

If you operate a standard checking or savings account, your money could be moved onto a new government-controlled network called FedNow.

The Fed is calling it a "speed upgrade" for the banking system.

They are telling banks …

"Join our new FedNow network and your customers will be able to send and receive money in seconds. Any time. Any day. Holidays included."

No wonder over 1,500 banks and credit unions have already signed on.

But here's what nobody's talking about …

For the first time in history, every single transaction moving through the US banking system will pass through one centralized "Fed-controlled" hub …

Silently tracking every purchase, transfer, bill payment and donation you make.

Currently, $2 TRILLION worth of transactions go through the traditional network every single day. But soon, it will be funneled through the new network that the Federal Reserve has built, operates and can see in real time.

That's the part buried in the Federal Reserve Docket No. OP-1670.

In fact, on page 84 of the 93-page document, they admit that it will make it easier to track the spending of Americans.

That's why I've put together 4 steps to "Fed proof" your savings before FedNow grants them complete control over your savings.

Discover the 4 simple steps here.

Good luck and God bless!

Martin D. Weiss, PhD

Weiss Ratings Founder

P.S. I've been watching government moves into personal finance for over 50 years. Cyprus savers didn't see it coming in 2013. Canadian truckers didn't see it coming in 2022. Don't let FedNow catch you off guard. See the 4 "Fed proof" steps before it's too late.

Corning's Surprise AI Boom: Is It Already Too Late to Buy?

Author: Nathan Reiff. Originally Published: 2/18/2026.

Key Points

- Shares of Corning, a glassmaker nearly two centuries old, have spiked by 152% in the last year as the company's products have found new demand in the AI space.

- With a major Meta partnership and notable earnings wins, Corning appears on track to enter a new phase as an AI partner.

- Still, rising short interest, insider sales, and concerns about valuation may give investors pause.

- Special Report: [Sponsorship-Ad-6-Format3]

Among unlikely AI stocks, glassmaker Corning Inc. (NYSE: GLW) ranks near the top. The company, with nearly two centuries of history making glass products, may be best known to consumers for its cookware and bakeware. In recent years, though, Corning has become an essential supplier to the tech industry: its glass enables smartphones and other devices, and its fiber-optics business has become increasingly important for data-center connectivity.

Once a burdensome segment, Corning's fiber-optics unit is now a preferred partner for firms working on AI because photonic data transfer can outperform traditional methods for high-speed needs. That shift—highlighted by a headline-making partnership with Meta Platforms Inc. (NASDAQ: META) reportedly worth $6 billion to help outfit data centers—has helped drive GLW shares up roughly 152% over the past year.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Investors may wonder whether it's too late to buy Corning. The company's recent earnings report, sustained institutional interest, and enthusiasm about its AI role remain strong. However, recent insider selling has concerned some investors—and may also present opportunities for others.

Is It Worth Waiting on Corning?

Corning's price-to-earnings (P/E) ratio sits around 72.6, near the highest level of the past year. Its price-to-earnings-growth (PEG) ratio is about 2.3 and its price-to-book (P/B) ratio is roughly 9.3, both suggesting the stock is richly valued after the recent rally.

Those metrics could persuade some investors to wait for a pullback before initiating or adding to a position. At the same time, several operational indicators point to continued momentum for the business.

In Corning's Q4 earnings report, the company beat expectations with EPS of $0.72 and revenue of $4.4 billion, up 14% year-over-year. Earnings grew 26% year-over-year and operating margin reached 20.2%, a key efficiency target hit a full year ahead of schedule.

That progress, together with the Meta agreement, led management to raise its projected incremental annualized sales under its "Springboard" plan. Corning now expects $11 billion in incremental annualized sales by the end of 2028, up from a prior $8 billion target.

Insider Sale Shake-Up, But Path Forward Remains Mixed

Over the past year, 14 Corning insiders have sold shares while none have reported purchases. Insider selling accelerated toward the end of 2025, with about $14 million of sales in the final quarter. The first quarter of the new year is on pace to exceed that level: insiders have already exited roughly $11 million of GLW with several weeks still remaining in the quarter.

Meanwhile, retail traders have increased short interest in GLW by more than 8% in the past month, signaling growing hesitation among some market participants at current valuations. Yet institutional ownership remains strong—nearly 70% of shares are held by institutions, and recent institutional inflows have outpaced outflows.

In short, the market shows both signs of caution (insider sales and rising shorts) and continued confidence (heavy institutional ownership and strong operational results). Individual investors should recognize that institutions often have different time horizons and risk tolerances than retail holders.

Wall Street analysts reflect this mixed view—about two-thirds rate GLW a Buy, but the consensus price target is more than 13% below the current share price, implying potential downside from here. Ultimately, investors must weigh Corning's compelling growth drivers and institutional backing against stretched valuations and recent insider selling when deciding whether to buy now or wait for a pullback.

3 Under-the-Radar Earnings Surprises Could Signal a New Trend

Author: Dan Schmidt. Originally Published: 2/17/2026.

Key Points

- Earnings season is starting to wrap up as more than 75% of S&P 500 companies have reported their latest results.

- Earnings and revenue beats are in line with historical averages, but divergences beneath the surface are creating different winners and losers than 2025's market.

- These three stocks typically fly under the earnings radar in their respective industries, but their positive recent reports deserve a closer look.

- Special Report: [Sponsorship-Ad-6-Format3]

Earnings season is winding down, and more than three-quarters of the companies in the S&P 500 have reported their latest results. According to FactSet, roughly 74% of firms reporting so far have beaten analysts' EPS estimates, and 73% have beaten revenue estimates.

While these overall figures are within the five- and ten-year averages, wide dispersion between winners and losers left aggregate earnings growth essentially flat for the season. Many of last year's success stories have underperformed in 2026, while some laggards have posted dramatic gains. Three companies whose earnings reports don't typically grab headlines still warrant attention for the figures in their most recent reports. Are these one-time standouts or the start of a larger trend?

Applied Materials: Semiconductor Demand and Guidance Power Double-Digit Gains

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

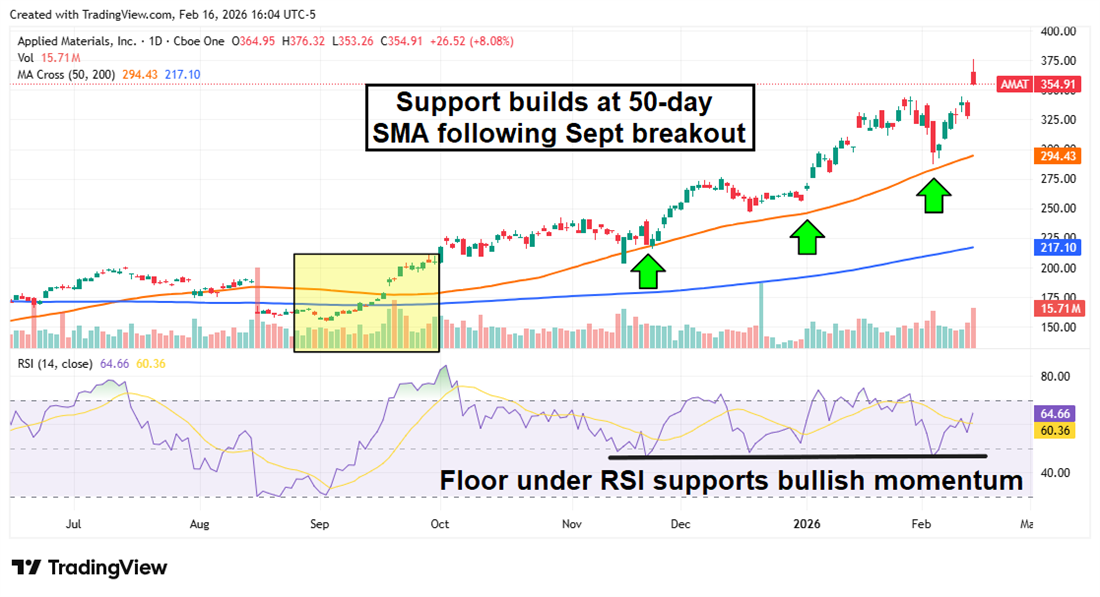

Applied Materials Inc. (NASDAQ: AMAT) is probably the most "on-the-radar" name here given its roughly $280 billion market cap and about $28 billion in annual sales. As a picks-and-shovels play in the semiconductor industry, Applied Materials often reports in the background while NVIDIA Corp. (NASDAQ: NVDA) or Alphabet Inc. (NASDAQ: GOOGL) dominate headlines. This most recent report, however, deserves attention: AMAT shares jumped about 12% after the release on strong guidance and robust equipment demand.

The company reported its fiscal Q1 2026 results on Feb. 12 and beat analysts' expectations on both EPS and revenue, with EPS coming in roughly 7% above forecasts. The commentary that really excited investors came on the conference call, when CEO Gary Dickerson projected 20% sales growth in calendar 2026 — a pace that exceeded even the most optimistic analyst estimates. Most of Applied's revenue comes from its Semiconductor Systems division, which provides equipment for memory and logic manufacturing (flash, DRAM, transistors, etc.). Dickerson guided to Q2 revenue of about $7.65 billion and noted continued rapid growth in the Applied Global Services business.

Price-target increases arrived quickly after the upbeat results, and the stock picked up two upgrades from Hold to Buy at Summit Insights and KGI Securities. The average target among the 17 analysts who raised their estimates is now $435, implying roughly 20% upside from current levels.

AMAT shares have been in an uptrend since September, when price crossed both the 50-day and 200-day simple moving averages (SMAs). The 50-day SMA has acted as reliable support on pullbacks. The Relative Strength Index (RSI) remains below the overbought threshold of 70 despite the earnings-driven pop, suggesting this rally could have staying power.

Advance Auto Parts: Turnaround Efforts Starting to Show Results

Advance Auto Parts Inc. (NYSE: AAP) may finally be returning to investability after losing more than 50% over the last five years. The past 12 months were particularly turbulent for the company (and the automotive sector broadly): it reported a steep loss in Q4 2024 and then faced tariff headwinds following the administration transition. CEO Shane O'Kelly has focused intensely on cutting costs and getting "back to basics," and those efforts are beginning to show results.

Advance Auto Parts' Q4 2025 results beat expectations. Revenue modestly topped analyst projections ($1.97 billion vs. $1.95 billion expected), and EPS of $0.86 was more than double the consensus. Same-store sales grew about 1% for the year, and management closed 17 underperforming locations. Management's 2026 guidance also helped the stock: it forecasts 1–2% comps (comparable-store sales), roughly 45% gross margins, EPS between $2.40 and $3.10, and roughly $100 million in free cash flow generation.

Some profit-taking followed the release, since the stock had already climbed nearly 50% year-to-date. Still, the technical picture remains constructive: the share price has cleared both the 50-day and 200-day SMAs, and the Moving Average Convergence Divergence (MACD) shows a bullish crossover with the MACD line rising above the signal line and histogram during the breakout.

Rivian: Narrowing Losses Point to 2026 Catalysts

Friday the 13th was anything but scary for Rivian Automotive Inc. (NASDAQ: RIVN). The company beat both top- and bottom-line estimates in its Q4 2025 report. Year-over-year (YOY) revenue fell about 25% due to the expiration of EV tax credits, but sales still topped expectations and the company narrowed its loss to $0.66 per share.

Smaller losses were driven by roughly a $5,500 increase in average vehicle selling price, while the cost of vehicles sold declined by about $9,500 on average. The quarter marked the company's first year of positive gross profit, and the more affordable midsize R2 model is slated to begin deliveries in Q2 2026. Rivian expects to sell between 62,000 and 67,000 vehicles in 2026, with the low end implying about a 47% increase over 2025 volume.

RIVN shares rallied as much as 20% in a volatile session after the report, though the intraday gain later retraced. The stock now sits at the 50-day SMA, which previously acted as support when shares rallied late in 2025. A bullish MACD crossover adds to the positive technical picture, but a successful R2 rollout will likely be necessary to sustain the momentum into 2026.

This email communication is a sponsored email for Weiss Ratings, a third-party advertiser of MarketBeat. Why did I receive this message?.

11780 US Highway 1,

Palm Beach Gardens, FL 33408-3080

Would you like to edit your e-mail notification preferences or unsubscribe from our mailing list?

If you have questions or concerns about your newsletter, please email our South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

Copyright 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Pl. #620, Sioux Falls, S.D. 57103. U.S.A..

No comments:

Post a Comment