Three times over the last 30 years.

That’s how often I’ve received the signal to go “all-in” on gold.

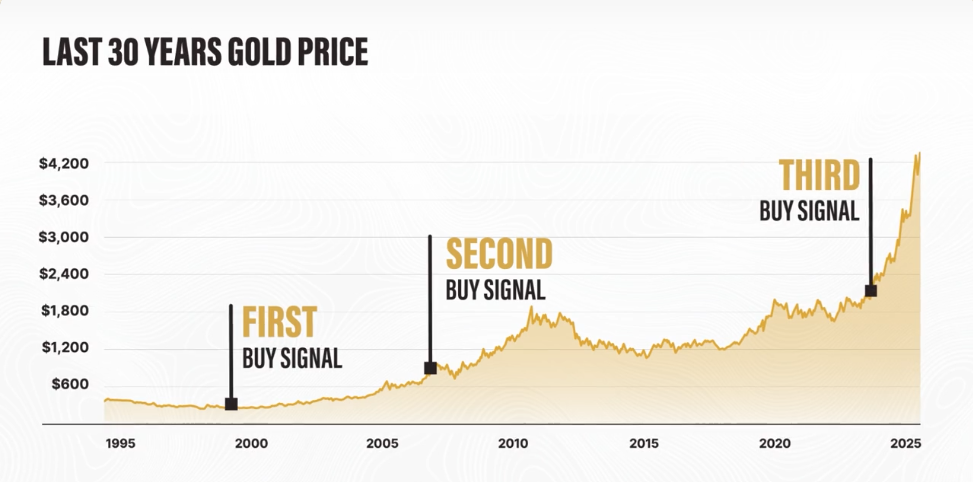

The first time was back in the 2000s…

The dot-com mania was nearing its peak, money was flooding into any and all tech stocks, and equity valuations were trading at nosebleed levels.

I was in my mid-20’s. Just starting my first business.

And although I didn’t have much capital to spare, I scrounged together as much money as I could to load up not on tech stocks… but on gold coins.

At the time, gold was despised by Wall Street.

Goldman Sachs called it “a 19th-century asset.”

One of Merrill Lynch’s top investment analysts said that it was only for “grandmothers and conspiracy theorists.”

And two of America’s leading economists at the time called it a “barren asset.”

Yet, I chose to go in at under $300 an ounce.

My second signal came in 2008 when, amidst the chaos of the financial crisis, gold prices dropped briefly below $800 an ounce… and I once again went “all-in” on gold.

And a little over a year ago, I did it again…

I moved roughly 50% of my liquid net worth into gold and Bitcoin:

Three “all-in” decisions… Each of which seemed crazy to most at the time.

But for me… it was the most obvious move to make.

Why?

It’s all thanks to an incredible secret I learned from famed economist Kurt Richebächer - the last of the true Austrian economists.

What he taught me has been incredibly accurate at predicting the price of gold over the years.

It’s helped me make an absolute killing each of the three times I went “all-in.”

And right now, it is again predicting a shocking new price for gold in the near future.

Click here to see my full prediction for gold now.

Good Investing,

Porter Stansberry

As Berkshire Exits Its Kraft Heinz Position, Is the Stock a Sell?

Submitted by Jordan Chussler. Posted: 1/27/2026.

Summary

- Newly entrenched Berkshire Hathaway CEO Greg Abel has decided to share the company’s 28% stake in consumer staples giant Kraft Heinz.

- The move comes after shares of KHC, which are down more than 3% year-to-date, lost 21% in 2025.

- Kraft Heinz has seen top-line contraction for eight consecutive quarters, resulting in analysts assigning the stock a consensus Reduce rating.

Last week, it was reported that newly installed Berkshire Hathaway (NYSE: BRK.B) CEO Greg Abel has initiated the process to sell the company's nearly 28% stake—or approximately 325 million shares—in consumer staples giant Kraft Heinz (NASDAQ: KHC).

The move, which came less than one month after Abel succeeded Warren Buffett, follows KHC shares sliding more than 3% to start the year after a 2025 performance that saw the stock fall by more than 21%.

Central banks are lying to you about gold (Ad)

Jerome Powell says gold is not money. The Fed says inflation is under control and the dollar is strong. But look at what they do. Central banks bought more gold last year than any time since 1967. China dumped $100 billion in U.S. debt, then bought gold. Poland, Hungary, Singapore, and Turkey are all loading up. In 2022, the U.S. froze Russia's money and showed the world that assets can be seized. Now major nations want out. There's only one asset no one can freeze: gold.

Get the name and ticker of one stock positioned for this shift.But for income investors whose dividend portfolios have relied on the company's strong yield for years, does Berkshire's exit—which marks the end of a 10-year position—make Kraft Heinz an automatic sell?

The Root of Kraft Heinz's Issues

Strictly by earnings, KHC has mostly delivered: the last time the company missed expectations was Q4 2018. But meeting earnings estimates does not necessarily equate to sustained profitability.

In Q2 2025, Kraft Heinz posted a loss of more than $7.8 billion tied to a $9.3 billion non-cash impairment charge, along with falling sales as inflation remained elevated.

The company, whose roots date back to 1869 (Heinz) and 1903 (Kraft), has relied on aggressive cost-cutting for years, including the controversial zero-based budgeting approach. A decade after the Kraft-Heinz merger, the food conglomerate is still struggling to work down the debt it took on in that deal.

To put that challenge in perspective: as of Q3 2025, Kraft Heinz carried more than $19 billion in long-term debt, far exceeding its cash position of $2.1 billion.

At the same time, a weak labor market, shifting consumer confidence, and ongoing U.S. dollar devaluation have pushed cash-strapped consumers away from name brands toward private-label (store brand) alternatives.

Can KHC Reverse Course?

In September 2025, Kraft Heinz announced plans to split into two scaled, independent companies. The division—tentatively named Global Taste Elevation Co. and North American Grocery Co.—is expected to be finalized in the second half of 2026.

Global Taste Elevation will focus on sauces and condiments, while North American Grocery will concentrate on meals and snacks. Management says the split will create more focused, scalable businesses.

But the plan has its critics, including Warren Buffett, who voiced disapproval in part because the split is not subject to a shareholder vote.

Over the long term, the two publicly traded entities—each with its own ticker—could help address problems that have dogged Kraft Heinz since the mega-merger. In the near term, however, a turnaround appears unlikely.

Although the company does not report full-year and Q4 2025 results until Feb. 11, it would not be surprising to see quarterly revenue contract for a ninth consecutive quarter. That persistent weakness has contributed to a negative net margin of 17.35%, indicating Kraft Heinz is currently spending more than it earns.

Meanwhile, a dividend payout ratio of roughly -43% shows the company is not generating enough earnings to cover its dividend, raising the risk of future cuts. Kraft Heinz's dividend currently yields an attractive 6.59%, or $1.60 per share annually, but income investors should be prepared for that yield to be reduced given the payout shortfall.

What Wall Street Thinks About Kraft Heinz?

Sentiment on Kraft Heinz is tepid. Of the 23 analysts covering the stock, one rates it a Buy, 17 rate it a Hold, and five rate it a Sell. Overall, KHC carries a consensus Reduce rating.

The average 12-month price target is $26.16, implying roughly 11% upside from where the stock is trading today. The company scores below about two-thirds of the firms evaluated by MarketBeat and ranks 73rd of 149 stocks in the consumer staples sector. Compounding concerns, Kraft Heinz's financial health sits in the Red Zone, according to Tradesmith, where it has been for more than 19 months.

Institutional ownership remains high at more than 78%, but that percentage is likely to fall once Berkshire Hathaway completes its sale of KHC shares. Short interest of 4.37% suggests bearish investors are watching for further downside in the year ahead.

This email is a paid sponsorship sent on behalf of Porter & Company, a third-party advertiser of MarketBeat. Why was I sent this email message?.

If you have questions or concerns about your subscription, please don't hesitate to contact MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Place #620, Sioux Falls, S.D. 57103. U.S.A..

No comments:

Post a Comment