Our research team was updating client portfolios last week when one of our analysts flagged something in the latest Treasury reports.

"Look at this," she said, pointing to her screen.

The numbers were worse than we thought.

We knew the debt hit $38.43 trillion.

But she'd calculated the daily growth rate: $8.03 billion per day, every day.

Then she showed me the interest payments: Over $1 trillion annually now.

Growing faster than any other government expense.

"My parents have everything in bonds and CDs," she said quietly. "They think they're safe. But if this continues..."

She trailed off, but we both knew what she meant.

The math is simple but brutal: The government can't pay these interest costs without printing money.

Printing money devalues every dollar your parents saved.

We've never seen data this concerning.

We decided people deserve to know what we found.

That's why we compiled The Big Beautiful Bubble Report. It includes:

- Why traditional "safe" investments are the riskiest now

- How the latest spending bill created artificial asset prices (wonder why real estate is so high? This reveals it)

- Trump's precious metals strategy that protects retirement funds

- Steps to transfer accounts before the devaluation accelerates

Because the numbers don't lie. The USA is in a bit of a pickle financially. Don't you think it is time you made a plan?

Download The Big Beautiful Bubble Report FREE

To your safe retirement,

Shanon Davis

CEO, American Alternative Assets

Why eBay's Depop Acquisition Matters More Than the Earnings Beat

By Chris Markoch. Date Posted: 2/20/2026.

Key Points

- eBay’s Q4 beat and GMV acceleration support a comeback narrative, even as the stock remains pressured by broader “AI trade” sentiment.

- Advertising and recommerce are emerging as durable growth engines, while Depop adds a targeted Gen Z/Millennial wedge.

- Depop integration costs, cyclical category tailwinds, and margin pressure remain the main risks to watch.

- Special Report: [Sponsorship-Ad-6-Format3]

Shares of eBay Inc. (NASDAQ: EBAY) are up about 3.8% the day after the company delivered a strong Q4 2025 earnings report. In many ways, the results make sense: the company is a pure play on consumer spending, which has remained resilient despite conflicting macroeconomic signals. And eBay fits into the "discount" category of retail stocks that have performed relatively well in a volatile market.

There was a lot for investors to like. Revenue of $2.97 billion exceeded expectations of $2.87 billion. A key metric, gross merchandise volume (GMV), climbed to $21.2 billion, up almost 6% globally and nearly 10% in the United States. That suggests the platform is expanding and attracting more customers.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Another highlight was the announcement that eBay will acquire Depop, the secondhand clothing marketplace owned by Etsy Inc. (NASDAQ: ETSY), for $1.2 billion in cash. The move is a strategic attempt to capture more of the Gen Z and Millennial customer base.

Like many stocks with even minimal exposure to artificial intelligence (AI), EBAY had been trading lower in 2026 ahead of the report. One strong quarter won't erase that trend, but there are several reasons to believe in eBay's comeback.

Ads, Fashion, and the Recommerce Angle

The Q4 report highlighted three specific engines doing the heavy lifting. The first is advertising. On an annualized basis, eBay is approaching $2 billion in ad revenue — a revenue stream that was almost non-existent five years ago.

Total advertising revenue was $544 million in Q4, representing GMV penetration of nearly 2.6%. First-party ads grew more than 17% to $517 million, and about 4.8 million sellers adopted at least one promoted listing product during the quarter. The takeaway is that advertising is becoming an embedded behavior on the platform, not just an optional tool for power sellers.

The second growth engine is recommerce (pre-owned and refurbished merchandise). This category accounted for over 40% of the company's GMV in 2025 and grew about 10% during the year. That distinction sets eBay apart from Amazon.com Inc. (NASDAQ: AMZN), and it's a segment Amazon will be hard-pressed to replicate at scale.

The third engine is the Depop acquisition. In 2025, Depop generated roughly $1 billion in gross merchandise sales for Etsy. Nearly 90% of Depop's 7 million active buyers are under 34 — a demographic eBay has historically struggled to attract. Depop also specializes in private-label fashion, one of the fastest-growing segments in retail. If those shoppers migrate to eBay's platform, the deal could deliver a meaningful and credible foothold in a younger cohort and help drive revenue growth.

A Marketplace Revamp With Real Teeth—or Temporary Tailwinds?

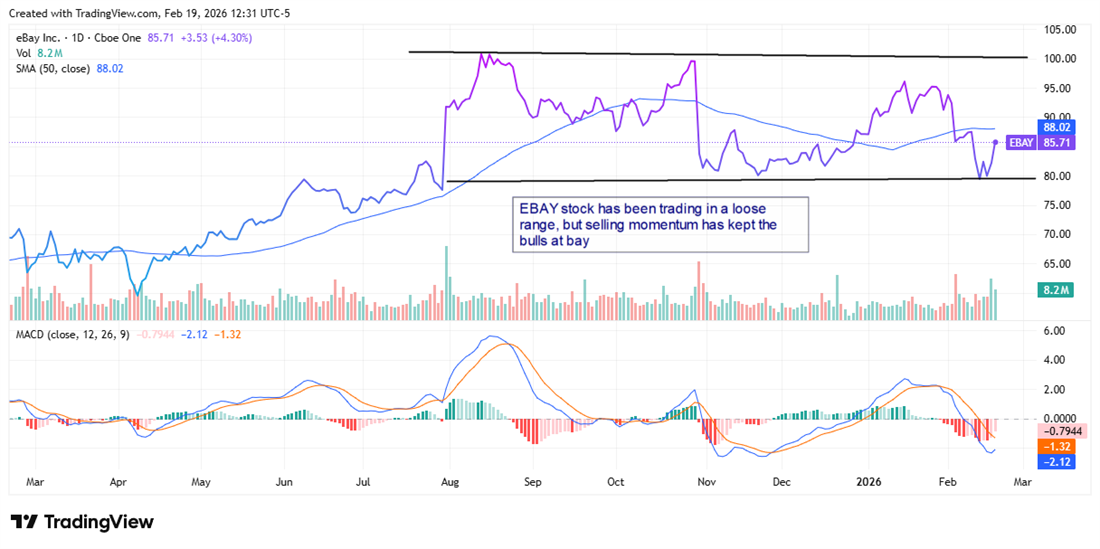

Institutional sentiment toward EBAY has been bearish over the past three quarters, with net selling of about $2 billion. Some of that selling followed the stock's August 2025 all-time high; since then, EBAY has traded in a loosely defined range with support around $80 and resistance near $100.

However, the eBay analyst forecasts on MarketBeat show analysts have been quick to raise price targets. Several of the new targets exceed the consensus price target of $96.52, which is about 12% higher than the stock price at the time of writing. The most optimistic target comes from Needham & Company, which raised its price target to $122 from $115.

Investors should also consider the company's dividend. A dividend alone isn't a reason to buy a growth-oriented stock like eBay — investors want to see the company investing in growth, which the Depop deal demonstrates.

That said, the dividend yield of 1.35% is above the S&P 500 average. The company has increased the payout to $1.16 at an average annual rate of more than 14% over the past three years, and the payout ratio of just over 25% looks sustainable and not overly burdensome on the company's cash flow.

Risks That Investors Shouldn't Ignore

While the bull case is compelling, investors should keep several risks in mind. First, some of Q4's GMV growth was commodity-driven. Management noted on the earnings call that bullion, collectible coins, and Pokémon trading cards provided meaningful tailwinds in late 2025. These categories are cyclical and unlikely to repeat at the same pace.

Second, the Depop deal—while strategically sensible—comes with near-term costs. eBay expects the acquisition to represent a low single-digit headwind to non-GAAP operating income growth and to dilute EPS growth, with accretion not expected until 2028.

Third, non-GAAP gross margin slipped by nearly 80 basis points year over year. Sustainable margin expansion against Amazon's logistics network and Shopify's (NASDAQ: SHOP) seller ecosystem remains the central question weighing on EBAY stock. The margin dip was primarily due to scaling managed shipping and Authenticity Guarantee programs — necessary investments that underscore the real costs of maintaining trust on a peer-to-peer marketplace.

Shipping Shock: ZIM Shareholders Secure Massive Cash Exit

Submitted by Jeffrey Neal Johnson. Article Posted: 2/18/2026.

Key Points

- ZIM shareholders are positioned to receive $35 per share in cash under its announced acquisition by Hapag-Lloyd.

- The deal’s structure includes a proposed spin-off of Israel-focused assets, aiming to address regulatory and national security concerns.

- ZIM’s trading price below the offer creates a merger arbitrage spread, reflecting timing and approval risk.

- Special Report: [Sponsorship-Ad-6-Format3]

Shareholders of ZIM Integrated Shipping Services (NYSE: ZIM) woke up to a transformed investment landscape on Feb. 17, 2026. After months of speculation and a volatile year for the shipping sector, the company announced a definitive agreement to be acquired by German shipping giant Hapag-Lloyd (OTCMKTS: HPGLY). The all-cash transaction is valued at approximately $4.2 billion, a figure that instantly reshapes valuation models across the logistics industry.

The market reaction was swift. ZIM shares jumped more than 30% to about $29.94 on heavy volume—nearly ten times the daily average—as investors focused on the offer price: $35 per share.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

For long-term holders, the acquisition is a sizeable win. The $35 offer represents a 58% premium over the stock's closing price on Feb. 13, 2026, and an even more striking 126% premium over the unaffected share price from August 2025. That latter metric underscores how much value management has unlocked relative to where the market valued the company six months ago.

But this deal is more than a typical merger; it is a strategic exit. The shipping industry is notoriously cyclical, prone to boom-and-bust swings that can erode shareholder equity. By securing a high-value cash buyout now, management has effectively insulated investors from future volatility, converting a fluctuating ticker into a definitive cash payout.

Consolidate or Die: The Strategy Behind the Spend

The size of Hapag-Lloyd's premium is a clear signal to the broader logistics sector. Major carriers are moving to consolidate capacity and acquire high-quality assets ahead of a potential cyclical downturn. ZIM's recent financial reports reflect this cooling: revenue fell 36% year-over-year in the third quarter of 2025, yet the company still commanded a substantial buyout premium.

That disconnect suggests strategic buyers like Hapag-Lloyd are looking beyond near-term revenue declines to asset quality and balance sheet strength. Hapag-Lloyd is buying durable revenue streams and a modern, efficient fleet. Over the last few years ZIM has taken delivery of 46 new vessels, many equipped with Liquefied Natural Gas (LNG) propulsion.

In a regulatory environment increasingly focused on carbon emissions, ZIM's fleet provides Hapag-Lloyd with a ready-made emissions upgrade. Building comparable ships would take years; acquiring ZIM secures them instantly.

Moreover, ZIM's balance sheet gave it significant negotiating leverage. As of Sept. 30, 2025, the company held roughly $3.01 billion in cash and reported a net leverage ratio of about 0.9x. That cash position effectively reduces the acquisition's net cost—subtract the $3 billion in cash from the $4.2 billion purchase price, and Hapag-Lloyd is obtaining the operating business at a markedly lower net price.

Diplomacy and Dealmaking: The 16-Vessel Solution

The primary hurdle in acquiring ZIM was political rather than financial. The State of Israel holds a Special State Share—a so-called Golden Share—that allows the government to veto transactions to protect essential food and security supply lines during times of conflict. For a German acquirer, that posed real regulatory risk.

To address this, the parties engineered a tailored solution: a spin-off entity. A new, separate company, dubbed New ZIM, will be created and sold to FIMI Opportunity Funds, Israel's largest private equity firm. New ZIM will not be owned by Hapag-Lloyd.

New ZIM will take ownership of 16 vessels dedicated to Israeli trade routes, ensuring a domestic owner oversees assets tied to national security interests while Hapag-Lloyd acquires the global commercial network. By structuring the deal this way—and partnering with a well-known local buyer—ZIM's board has converted a potential regulatory veto into a legally binding solution, materially reducing approval risk and unlocking the $35 payout.

Mind the Gap: The Arbitrage Opportunity

Despite the signed agreement and the large premium, ZIM stock is trading near $27.75 while the cash offer is $35, leaving a spread of roughly $7.26 per share.

This is a classic merger-arbitrage spread. The market is discounting the stock—by roughly 26% relative to the current price—because of the time until the expected closing in late 2026 and residual regulatory uncertainty. For patient investors, however, that gap represents an opportunity: buying at today's price and holding to closing would likely yield an attractive return if the deal completes as planned.

Investors are also being paid to wait. ZIM has continued returning capital to shareholders, recently declaring a $0.31 dividend based on Q3 earnings, which provides income during the regulatory review. The primary risk remains deal failure, but the New ZIM structure materially hedges the most probable regulatory objection.

Cash Is King: Locking in the Win

Hapag-Lloyd's acquisition changes the investment story from operating volatility to realized value. Management secured a premium exit that many analysts did not expect, monetizing the company's fleet modernization and cash reserves at a favorable point in the cycle.

While closing will require patience, the New ZIM spin-off lays out a clear, executable path through a complex geopolitical landscape. For shareholders, the focus shifts from tracking freight-rate cycles to watching the transaction close: the $35 cash offer provides a definitive endpoint, locking in significant value in a sector often defined by uncertainty.

This email message is a sponsored message sent on behalf of American Alternative, a third-party advertiser of MarketBeat. Why did I receive this email?.

If you have questions about your subscription, please don't hesitate to contact our U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Pl., Suite 620, Sioux Falls, South Dakota 57103-7078. U.S.A..

No comments:

Post a Comment