Friend,

History rhymes.

March 1968: Central banks ran out of gold.

London shut down for two weeks. Gold went from $35 to $850.

That's 2,329%.

March 1980: COMEX couldn't deliver silver.

They changed the rules. The Hunts got wiped out.

But Silverado Mines ran 3,989%.

March 2020: Swiss refineries closed. Delivery stopped.

The CME made up a new contract on the fly. Karora Resources ran 847%.

See the pattern?

It's always March. The crunch. The rule changes. The chaos.

Every time, paper holders got crushed. Mining stock holders got rich.

The next big delivery month is April 2026. First Notice Day is March 31st.

I've found the one stock set to capture the bulk of this wealth transfer.

>> See My #1 Pick for the Coming Crisis <<

The Buck Stops Here,

Dylan Jovine

Guidance, Not Earnings, Sends Equinix Stock Higher

Author: Chris Markoch. Article Published: 2/12/2026.

At a Glance

- Equinix stock rallied despite an earnings miss as 2026 guidance pointed to accelerating revenue and FFO growth tied to AI infrastructure demand.

- The company’s global interconnection platform positions it as a central hub for AI workloads, cloud access, and edge deployment.

- After a sharp post-earnings move pushed EQIX into overbought territory near analyst price targets, investors may benefit from waiting for a pullback while collecting a growing dividend.

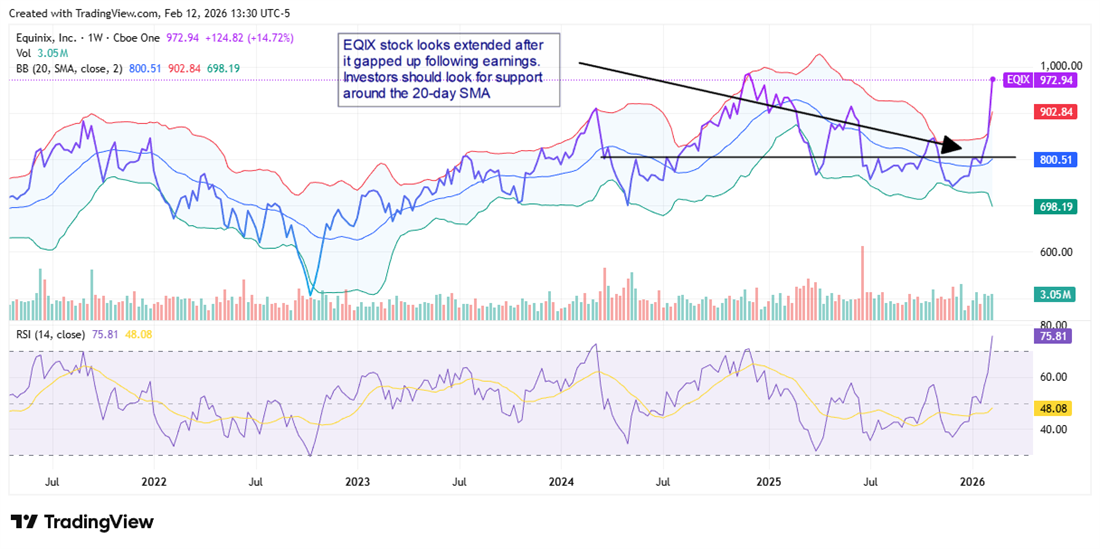

Equinix Inc. (NASDAQ: EQIX) stock is up more than 12% after the company reported earnings following the close of trading on Feb. 11. The real estate investment trust (REIT) missed on both the top and bottom lines, but it was the guidance that has investors bidding the stock higher.

Specifically, Equinix projected full-year 2026 revenue in a range of $10.12 billion to $10.22 billion. That's slightly above the consensus estimate of $10.07 billion and signals that growth is still accelerating.

Three Nobel Prize winners: A convergence is coming (Ad)

Watch Now! Porter Stansberry & Luke Lango join forces to unveil:

The Three Titanic Forces Converging To Unleash A New 1776 Moment

"We have never seen wealth created at this size and speed" MIT Researcher

Funds from operations (FFO) is a critical metric for REITs, and Equinix now projects FFO to grow by 10.5% in 2026—well above the 5% growth estimate it provided in June 2025.

It's easy to see why investors liked what they heard. But after such a strong move higher, is this a time to buy EQIX stock, or is caution the better strategy?

A Hub for AI Infrastructure

Equinix is primarily a data center operator with 280 data centers in 36 countries. The company owns 176 of its 280 data centers, and more than 80% of its recurring revenue comes from either owned properties or leases that expire in 2041 or later.

Equinix specializes in "interconnection"—facilitating direct, private links between businesses, cloud providers, networks, and other digital infrastructure. In the current AI infrastructure buildout, Equinix's data centers act as hubs for several spokes in the AI workflow.

- Network Hub — where you aggregate and access your data

- GPU Colocation — where you train and run your models

- Edge Gateway — where you deploy those models close to end users

Companies can do all three within Equinix's ecosystem, with fast, private connections between each component. It's the difference between having an office, factory, and distribution centers all in the same industrial park versus scattered across different cities.

Equinix's guidance is another example of why some analysts may be underestimating the practical demand drivers behind the AI story.

Can Equinix's Growth Continue to Outrun Estimates?

This is the question investors need to consider if they don't already own EQIX stock. The gap-up after the earnings report has pushed the stock into overbought territory, which argues for short-term caution.

But technical indicators only tell part of the story. Short interest is up slightly in 2026 but remains only about 2% of the stock's float. With 94% of the stock held by institutional investors, significant short pressure seems unlikely.

The stock is trading around $980 per share, a hair below the $1,000 price target Jefferies issued on Feb. 12. MarketBeat's analyst forecasts show the highest price target of $1,050 coming from HSBC.

Combining overbought signals with analyst targets that imply limited upside suggests the next move could be lower, at least in the near term.

Get Paid to Wait

A compelling benefit of many REITs is their dividends. REITs are required to distribute at least 90% of their taxable income as dividends. With a share price approaching $1,000, Equinix yields about 1.96%—not a high yield by conventional measures.

But the payout is still noteworthy. The company recently increased its quarterly dividend to $5.16. If that dividend holds for the full year, it amounts to $20.64 per share annually. Equinix has raised its dividend for 10 consecutive years, with an average three-year growth rate of about 11.11%.

Investors who believe in the company's long-term growth may reasonably expect total returns for EQIX stock to move closer to its 10-year average of roughly 28% over time, though near-term volatility remains possible.

This email content is a paid advertisement for Behind the Markets, a third-party advertiser of MarketBeat. Why was I sent this message?.

If you need assistance with your newsletter, please don't hesitate to email our South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 North Reid Place, Sixth Floor, Sioux Falls, S.D. 57103. U.S.A..

No comments:

Post a Comment