Since September of last year, a small group of traders has been getting three stock picks delivered to their inbox every single week.

They didn’t find it on Reddit. It wasn’t featured anywhere. Most of them stumbled onto it and figured there had to be a catch.

There wasn’t.

While they’ve been quietly collecting tickers every Monday morning, some of those picks went on to return 205%... 161%... 127%... 110%.

69 different winning tickers so far…

They didn’t pay for any of it.

This week’s three names just went out.

Click here to get on the list.

3 Consumer Staples Stocks Breaking Out This Month

Reported by Dan Schmidt. First Published: 2/9/2026.

Key Points

- Investors have started rotating out of volatile tech stocks and into safer assets.

- Consumer staples are often considered a 'safe' sector since its constituients sell necessities like food, household items, and hygiene products.

- These three consumer staples stocks appear to be on the verge of breaking out following a rough performance in 2025.

- Special Report: [Sponsorship-Ad-2-Format3]

A new rotation is underway as investors abandon the tech ship in search of safer assets. AI hyperscalers are still posting solid earnings, but even Mag Seven stocks are selling off after impressive top- and bottom-line beats. As bold AI capital expenditure (CapEx) plans are met with skepticism rather than optimism, the market is shifting toward a risk-off environment, and commodities and sectors like consumer staples look more attractive. If the tech rotation continues to intensify, the three stocks we discuss today offer upside potential along with strong dividend income.

Rotation Into Consumer Staples Is Picking Up Steam

Nothing lasts forever in markets, and the AI trade is starting to wobble more noticeably than it has since the end of the Fed hiking cycle in 2022. AI bellwether NVIDIA Corp. (NASDAQ: NVDA) has gone nowhere for six months, and Oracle Corp. (NYSE: ORCL) has lost about 60% since its September all-time high. Mega-caps like Alphabet Inc. (NASDAQ: GOOGL) and Amazon.com Inc. (NASDAQ: AMZN) sank after earnings despite announcing 2026 CapEx plans that would rival the GDP of some small countries. Data center growth takes time, and hyperscalers are competing for increasingly scarce resources such as energy and memory.

This makes me furious (Ad)

I Called Black Monday. Now I'm Calling March 26!

I predicted the 1987 crash six weeks early. I called the fall of the Berlin Wall. I pinpointed the exact bottom in 2009.

Now I'm staking my reputation on March 26, 2026 - the day I believe Elon will announce the SpaceX IPO.

Bloomberg is calling it "the biggest listing of ALL TIME."

A $1.5 TRILLION valuation... the "wealth-building" moment of the decade.

Today, I'll show you how to get in before the big announcement.

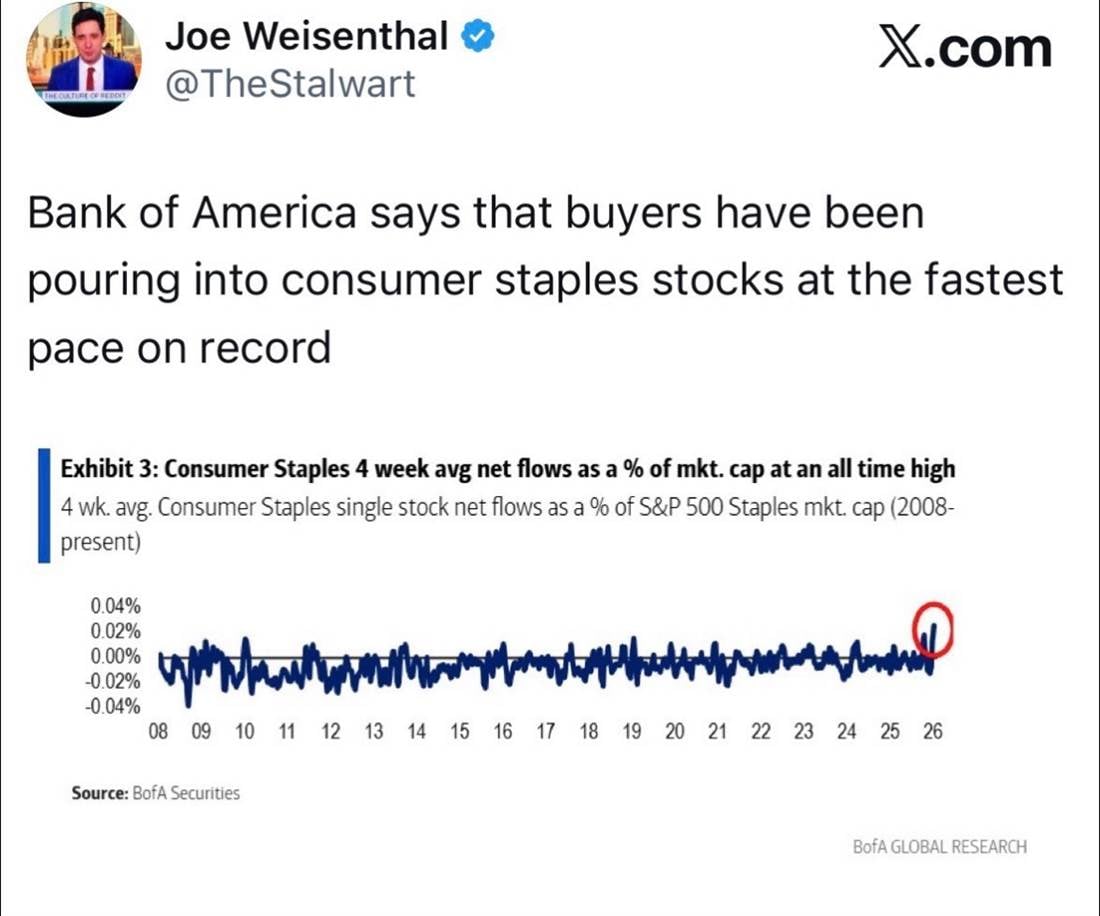

Investors are beginning to seek risk-off assets in case these ambitious plans fail to deliver profits. But the market action in gold and silver over the last few weeks hardly looks like a classic flight to safety. Money may be flowing out of tech stocks, yet it isn't leaving the market entirely, as this post from Bloomberg's Joe Weisenthal illustrates:

Consumer staples usually aren't the target of speculative fervor, so sizable inflows likely mean investors are taking some risk off the table as speculative returns diminish. These are defensive businesses with consistent, predictable sales that typically return a significant portion of profits to shareholders. With cryptocurrencies crashing and the precious-metals trade sputtering, the stampede may visit this sector next.

3 Breakout Consumer Staples Stocks With Strong Dividends

Predictability is a perk of value sectors like consumer staples, but it doesn't always mean sacrificing growth. The three stocks selected here are household names that suffered meaningful drawdowns in 2025. Now that we've entered 2026, each is showing signs of a technical breakout.

Procter & Gamble: Dividend King Making Long-Awaited Technical Breakout

Procter & Gamble Co. (NYSE: PG) just posted its best month in nearly two years, gaining roughly 13% over the past 30 days. Margin improvement helped fuel the move: the company generated 270 basis points of productivity savings in its fiscal Q2 2026 report, helping offset tariff headwinds. The stock also surged above the 200-day simple moving average (SMA) for the first time since early last year, a key technical milestone.

The company maintained its 2026 revenue guidance, which supports another year of dividend increases for this Dividend King. P&G has raised its dividend for 70 consecutive years, yet it allocates only about 62% of earnings and less than half of free cash flow to the payout. The company returned more than $4.8 billion to shareholders in Q2 alone, making PG a reliable place to shelter from market volatility.

Reynolds Consumer Products: Mitigating Tariffs and Commodity Volatility

Reynolds Consumer Products Inc. (NASDAQ: REYN) jumped nearly 10% after its Q4 2025 earnings release on Feb. 4, driven largely by margin resilience despite tariffs and rising input costs. Aluminum is the biggest concern for the maker of Reynolds Wrap foil, as the spot price has climbed nearly 20% since last April. Reynolds, however, maintained roughly 21% adjusted EBITDA margins on $220 million in adjusted EBITDA, successfully offsetting the price increases on its key product. Hefty products also posted a 3% year-over-year retail volume increase.

The daily chart is showing signs of life, with a Golden Cross and support forming near the 200-day SMA. Reynolds offers a roughly 4% dividend yield with a 63.9% dividend payout ratio (DPR). It doesn't have P&G's long history of increases, so Reynolds' dividend behaves more like a bond coupon, but the company appears to have room to sustain the payout — especially if aluminum price pressure eases.

Constellation Brands: Strong Earnings and Stock Breakout Calm Beer Slowdown Fears

Declining beer sales have been a worry for Modelo and Pacifico parent Constellation Brands Inc. (NYSE: STZ), but the company eased those concerns in its most recent quarter. Constellation released its fiscal Q3 2026 earnings last month: revenue fell nearly 10% year over year, yet it was still ahead of expectations. Beer operating margins came in better than expected, helping limit the damage, and the stock is up more than 15% since the Jan. 8 report.

Bullish momentum has been building in STZ since last November, and the stock recently cleared the 200-day SMA after a long downtrend. Constellation looks like an intriguing value play, trading at about 12 times forward earnings and 2.6 times sales. It also uses only roughly 12% of cash flow to cover its 2.46% dividend yield and has increased its payout for five consecutive years.

Amazon Erases a Year of Gains—2 Reasons the Market's Wrong

Author: Sam Quirke. Posted: 2/16/2026.

Key Points

- Amazon shares are down more than 12% this year and over 20% from November’s all-time high, drifting back toward levels last seen nearly a year ago.

- The stock’s RSI has sunk into the low 20s, marking one of its most oversold readings in almost four years.

- Analyst support remains overwhelmingly bullish, with price targets implying close to 60% upside from current levels.

- Special Report: [Sponsorship-Ad-2-Format3]

After months of steady pressure that intensified in recent weeks, Amazon.com Inc (NASDAQ: AMZN) is back to where it was at the start of last March. Shares are down more than 12% year-to-date and over 20% from November's all-time high, effectively wiping out the gains of the past 12 months.

For a company with so much going for it fundamentally, the stock simply can't seem to catch a break. Investors have been rotating out of mega-cap tech, concerns about Amazon's capital expenditure plans have risen, and sentiment across the sector has cooled materially. But beneath the surface, the current setup is beginning to look extreme. Here are two reasons to think the market may have gone too far.

Reason #1: The Stock Is Extremely Oversold

This makes me furious (Ad)

I Called Black Monday. Now I'm Calling March 26!

I predicted the 1987 crash six weeks early. I called the fall of the Berlin Wall. I pinpointed the exact bottom in 2009.

Now I'm staking my reputation on March 26, 2026 - the day I believe Elon will announce the SpaceX IPO.

Bloomberg is calling it "the biggest listing of ALL TIME."

A $1.5 TRILLION valuation... the "wealth-building" moment of the decade.

Today, I'll show you how to get in before the big announcement.

The technical picture is flashing oversold. Amazon's relative strength index (RSI) has slipped into the low 20s, its weakest reading in nearly four years. That degree of oversold pressure is unusual for this stock, particularly given that the company has consistently delivered strong earnings and reinforced its growth story over the same period.

Historically, when Amazon's RSI has reached this type of technical exhaustion — any reading below 30 — it hasn't stayed there long. Extremely oversold readings have tended to mark temporary lows rather than midpoints in a sustained breakdown.

In April of last year, for example, a brief dip below 30 on the RSI preceded a rally of roughly 60%. In August 2024, another sub-30 reading was followed by a comparable move. Going back to November 2022, the rebound was even more dramatic.

History doesn't have to repeat itself, but it often rhymes, and this pattern is worth respecting. When sentiment has been this one-sided in the past, it has signaled an opportunity. If Amazon shares can stabilize in the coming sessions and the RSI starts turning back north, that would be an early sign bullish accumulation has begun.

Reason #2: Analysts Are Not Backing Down

If the technical case is compelling, analysts' fundamental support makes the setup even harder to ignore. Rarely is there such a wide disconnect between what the market is doing to a stock and what analysts say it should be doing.

A slide of this magnitude would normally trigger a cascade of rating downgrades as analysts reassess their views. Instead, many are holding firm. In the past week, teams at Daiwa Securities Group and New Street Research reiterated Buy ratings, and Argus did the same the week before. Price targets among the bullish camp stretch as high as $325, which, with the stock trading below $200, implies nearly 60% in potential upside.

That kind of asymmetry is hard to dismiss for one of the leading mega-cap tech companies. Analysts point to renewed strength in Amazon's AWS business, where growth appears to be accelerating rather than slowing. Combine that with the company's structural moat in e-commerce, diversified revenue streams and expanding advertising footprint, and the long-term thesis remains intact.

Watching for the Turn

Concerns about increased capital expenditure clearly helped catalyze the recent selloff. But at current levels, much of that fear looks priced in. The pullback has pushed Amazon's price-to-earnings (P/E) ratio below 30 for the first time in years, making the valuation materially more attractive than it has been recently. It would be difficult to sustain a bullish stance if analysts were abandoning ship en masse — instead, many are doubling down.

For now, the setup hinges on stabilization. If the stock can hold near current levels and begin carving out a base instead of sliding to fresh lows, the bullish case strengthens quickly. With shares pressing toward their 52-week low, the RSI at multi-year extremes, and analysts calling for as much as 60% upside, the risk/reward profile is hard to ignore.

This email communication is a paid advertisement sent on behalf of True Market Insiders, a third-party advertiser of MarketBeat. Why did I get this email content?.

If you need help with your newsletter, feel free to contact our South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Pl. #620, Sioux Falls, South Dakota 57103-7078. United States of America..

No comments:

Post a Comment