Hi there,

Our investment research analysts are going to be releasing their next investment idea tomorrow morning, around 10:00 AM Eastern time.

It will be first sent to subscribers that sign up to receive American Market News via SMS, then later in the morning to people who subscribe to our email newsletter or read our content on our website.

Don't miss out on your opportunity to be among the first to see our next stock idea. Our last idea was quite popular with our subscribers.

This is a free service from American Market News. If you want to take advantage of this unique research opportunity, just click the link below to be added to our priority distribution list.

Get Research Alerts from American Market News

Jessica Mitacek

Managing Editor

American Market News

3 Stocks to Play the Summer Travel Boom as Demand Surges Again

Written by Dan Schmidt. Originally Published: 2/10/2026.

Summary

- A potential 2026 travel rebound is being fueled by improving demand drivers, including higher-end spending and a business travel recovery.

- Several travel names are already showing technical momentum, suggesting investors may be rotating into the group early.

- Hilton, Delta Air Lines, and Marriott are positioned to benefit if premium travel demand stays resilient.

The world is gearing up for a travel boom in 2026, and investors are starting to take notice. Travel is moving from a lagging sector to a leadership group as demand drivers reaccelerate and visibility improves across airlines and hotels.

With several major events on deck and premium spending holding up, the setup is improving even before peak travel season. The travel industry — once downtrodden — has produced outsized gains to start 2026, driven by several fundamental factors.

Nvidia CEO Issues Bold Tesla Call (Ad)

While headlines focus on Tesla's car sales, tech analyst Jeff Brown says the real story is Tesla's role in a $25 trillion AI revolution — one that Nvidia's CEO himself has called a "multi-trillion-dollar future industry" — and he's uncovered a little-known stock 168 times smaller than Nvidia that could be positioned to ride this breakthrough.

Click here now to see the full reportThree stocks could stand out as potential leaders if the 2026 travel boom materializes.

Global Travel Demand Expected to be Strong in 2026

Pent-up demand, several catalysts, and economic dynamics are converging to create a favorable environment for global travel. Many stocks in this space have already started breaking out, and the outlook has improved over 2025's weak travel season. Some of the key factors that have investors intrigued by travel stocks include:

- Return of Business Travel: You may be tired of hearing about the K-shaped economy, but the phenomenon is helping a previously lagging area of the industry. Business travel is rebounding significantly, resulting in higher spending, as corporate clients tend to occupy the upper tier of the K and opt for premium options. Analysts at Morgan Stanley anticipate corporate travel budgets growing 5% in 2026, while hotel room rates are projected to increase 3.9%.

- Global Sporting Events: 2026 is shaping up to be a big year for international sports, with some of the world's biggest spectator events occurring within a few months of each other. The Winter Olympics in Milan are currently underway, followed next month by the World Baseball Classic (WBC). The biggest event, the 2026 FIFA World Cup, is scheduled for this summer across the U.S., Canada, and Mexico. It's been more than 20 years since the U.S. last hosted a World Cup — the 1994 tournament attracted more than 3.5 million attendees.

- Sector Rotation: Market mechanics are also at play, and the travel industry is a beneficiary. The AI rally is cooling as investors look for safer sectors such as consumer staples and financials. Travel stocks, with several catalysts on the horizon, are a natural landing spot for some of the capital rotating out of tech.

3 Travel Stocks Breaking Out This Month

If a breakout in travel stocks is imminent, it will likely start with these three companies. Each benefits from increased spending by higher-spending clientele and has technical momentum behind its move.

Hilton: Stock Breaking Out of Year-Long Consolidation

Hilton Worldwide Holdings Inc. (NYSE: HLT) is a premium brand with an asset-light business model, making it an intriguing investment in the current market environment.

The company reported more than 515,000 rooms in its pipeline in its Q3 2025 report in October and is targeting 6–7% annual growth in 2026 and 2027.

Management also projects 2–3% growth in 2026 in the key Revenue per Available Room (RevPAR) metric, which was flat in 2025.

The company reports its Q4 and full-year 2025 results on February 11 before the opening bell, and investors will be watching closely for 2026 RevPAR guidance.

Analysts are bullish on the stock ahead of earnings. The stock received five different price-target boosts last week, including new $330 targets from TD Cowen and Goldman Sachs.

The chart also shows strong bullish momentum. Despite forming a Golden Cross over the summer, the stock was stuck in a tight range for most of the second half of 2025 before breaking out above the 50-day simple moving average (SMA) in November. HLT shares have already reached several new all-time highs this year, and there could be more upside if the company reports strong earnings this week.

Delta Air Lines: Corporate Travel Boosting Earnings Growth

Delta Air Lines Inc. (NYSE: DAL) has soared to new all-time highs this year thanks to strong earnings growth driven by corporate travel clients.

The company released its Q4 2025 earnings report on January 13 and posted a slight EPS beat alongside a small revenue miss; management attributed the slowdown in sales growth largely to the government shutdown.

More importantly, the company reported a record $4.6 billion free cash position and projects 20% year-over-year (YOY) EPS growth in 2026, driven by further increases in premium-cabin revenue.

If economy-class travel recovers, the 20% EPS growth estimate could prove modest. The stock's breakout is also backed by several technical signals, including strong support at the 50-day SMA and an uptrending Relative Strength Index (RSI).

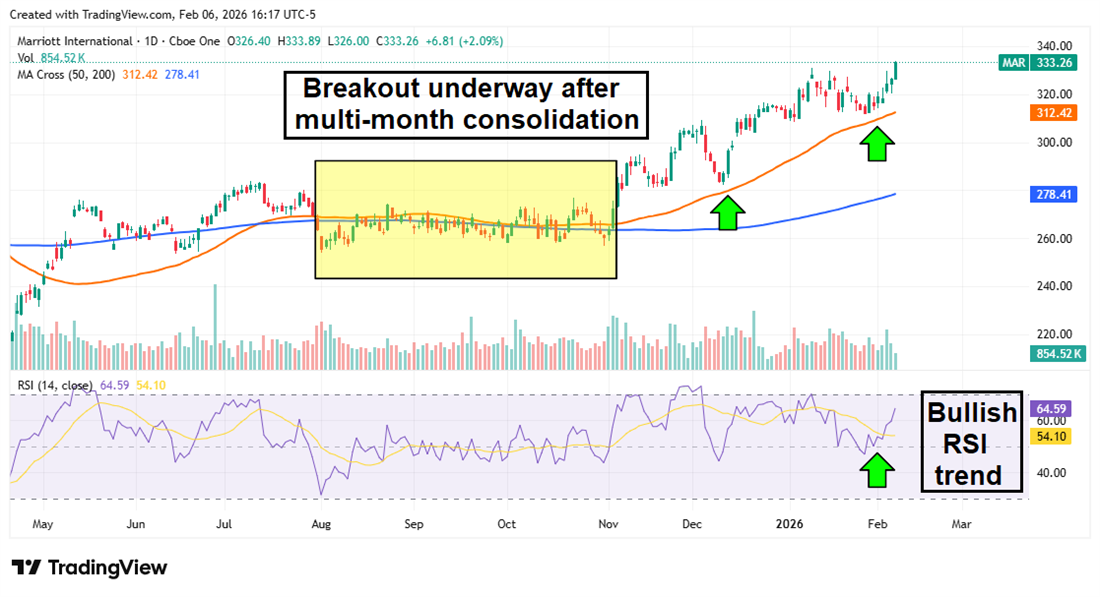

Marriott: High-End Clientele and Loyalty Program Provide Solid Floor

Marriott International Inc. (NASDAQ: MAR) is a global premium hotel brand, and its Bonvoy loyalty program is widely regarded as the industry standard, with nearly 237 million members.

The company projects 2026 revenue to grow more than 6% YOY, and its RevPAR outlook is improving after just 0.5% growth in Q3 2025.

MAR shares spent most of the fall consolidating around the $270 mark in a tight range before breaking out above the 50-day SMA in November.

The 50-day moving average is now acting as support, with the RSI trending upward, providing strong bullish momentum for the rally.

Marriott reported its Q4 results on Feb. 10 and posted a strong revenue beat and a slight earnings miss, but optimistic 2026 guidance sent the stock surging 8% after the release.

Monday.com Hits Rock Bottom: Overdone Sell-Off Ready to Rebound

Authored by Thomas Hughes. Posted: 2/9/2026.

Quick Look

- Monday.com retreated to long-term lows in February as its sell-off overextended on overblown fears.

- Institutions have been accumulating this stock, which may limit downside risk, with shares trading at rock-bottom prices.

- The timing of the rebound is uncertain, as retail market sentiment is driving the action.

If you think AI is the death knell for software stocks, then monday.com (NASDAQ: MNDY) isn't the stock for you. Its software-as-a-service business is often cited as ripe for disruption, setting it up for a slow implosion already priced into the market. However, if you think AI's disruptive power is overstated, monday.com's sell-off looks overblown and an opportunity is arising.

While AI is a disruptive force, the company's Q4 results and guidance show that monday.com remains in high demand. Even if AI meaningfully changes the software landscape, that transition will take years. The more likely scenario is that cloud-based SaaS companies like monday.com will adopt new models, build partnerships with leading AI providers, improve ecosystem compatibility and continue to be a central part of business workflows. The environment will shift and evolve, and leaders like monday.com appear well-positioned to benefit.

MNDY Stock Falls on Cautious Guidance, Spending Increases

Nvidia CEO Issues Bold Tesla Call (Ad)

While headlines focus on Tesla's car sales, tech analyst Jeff Brown says the real story is Tesla's role in a $25 trillion AI revolution — one that Nvidia's CEO himself has called a "multi-trillion-dollar future industry" — and he's uncovered a little-known stock 168 times smaller than Nvidia that could be positioned to ride this breakthrough.

Click here now to see the full reportmonday.com delivered a strong Q4 2025, with revenue up 24.6% to $333.9 million. The top line beat the analyst consensus by about 100 basis points, driven by client wins and increased services penetration. The company's net retention rate (NRR), a measure of revenue growth from existing customers, was 110%, underpinned by strength among larger clients.

NRR for the company's largest customers (defined as those with 10+ users) was 114%, while customers contributing more than $50,000 in annual recurring revenue had an NRR of 116%. The number of customers with more than 10 users rose 8%, while customers contributing more than $50,000, $100,000 and $500,000 in ARR increased by 34%, 45% and 74%, respectively—highlighting the product's traction with enterprise accounts.

Margin news was mixed. The company faced some margin contraction driven by foreign-exchange headwinds and increased spending, but its adjusted results still exceeded consensus by a wide margin—roughly 1,300 basis points relative to analyst expectations. That said, the higher marketing and R&D spend did offset some of the upside.

Spending on marketing and R&D is clearly aimed at sustaining the company's double-digit growth and securing larger customer wins. Management expects elevated spending to continue into 2026, although it said such levels are unlikely to be permanent.

Guidance was the key concern for investors. While the company issued a solid guide—forecasting roughly 20% revenue growth in Q1 and about 19% for 2026—the margin contraction embedded in that guide was below many analysts' expectations.

There is a risk that monday.com's business could underperform guidance, but the internal metrics suggest the company is performing well. Customer growth and penetration remain strong, and indicators such as a 31% increase in current remaining performance obligation (current RPO) and a 37% increase in total RPO point to conservative guidance.

Analysts Indicate a Deep Value Opportunity: Institutions Are Buying

Analyst reactions helped push down monday.com's share price, but the move appears overdone. Trading below $90, the stock sits well under the low end of most analyst target ranges, suggesting a deep-value opportunity. Valuation metrics such as price-to-earnings also support the contention. Even if margin pressure persists through 2026, the company's growth trajectory supports a much higher valuation over the long term. With a catalyst, a rebound of 100% to 300% is possible, and institutional activity is setting the stage for that move.

Institutions, which own more than 70% of the stock, have been net buyers for eight consecutive quarters. Over the trailing 12 months, institutions bought more than $2 for every $1 sold, accelerating to nearly $3 bought for each $1 sold in January 2026. That buying pattern suggests institutions may step in on recent weakness and limit the downside potential. The market floor is likely near long-term lows and will be an important support level to watch. If the stock falls below that critical support and fails to regain traction, broader market dynamics could make a deeper decline more likely.

This message is a paid sponsorship from American Market News, a third-party advertiser of MarketBeat. Why did I receive this email message?.

If you need assistance with your newsletter, feel free to email MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

Copyright 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 North Reid Place #620, Sioux Falls, South Dakota 57103. USA..

No comments:

Post a Comment