Warren Buffett is sitting on $325 billion in cash – his largest hoard ever.

Not because he wants to – but because he can’t find value in the usual places.

Now, as US government spending spirals out of control, Buffett knows he’s losing billions of dollars to inflation.

That’s why I predict Buffett’s next investment will catch millions of people off guard.

It’s not another bank… railroad company… or more shares of Apple.

It’s a gold company. How do I know?

Because the math doesn’t lie:

You can buy the average gold developer for $30 and get back $13 a year —

That’s a 43% ROI annually.

Over 10 years, that’s $130 on a $30 investment.

Tell me where else Buffett can get that.

But there’s one specific miner Buffett likes best:

- It’s the best-managed major gold miner in the industry…

- Has massive cash flow…

- Is trading at a deep discount to fair value…

- Positioned at the heart of Trump’s new mining push…

Don’t wait for Buffett to reveal his position in his 13F filing on February 17th…

Right now, you have the chance to front-run the greatest investor of all time. Go here and I’ll give you the name and ticker – along with details on my top four small miners.

To your wealth,

Garrett Goggin, CFA, CMT

Chief Analyst & Founder, Golden Portfolio

P.S. A lot of investors write in to tell me how much they’ve made in Bitcoin. My reply? Good for you. First off, gold investing is cyclical. You really only want to own gold at one specific time in the cycle. That time is now. Second, the world’s governments are not buying Bitcoin. They’re betting on gold. All of them. Bitcoin (does anyone really know for sure the US government didn’t create it?) will be a good bet… until it isn’t. It may end up doing great. Or it may be eclipsed by any number of tech developments.

Meanwhile, gold will continue to do what it’s done for almost 6,000 years of recorded human history: Protect wealth through chaos. Go here if you want the name and ticker of Buffett’s likely gold play… and details on my top four miners

Axon Got Caught in the SaaS Crash—Its Earnings Say That Was a Mistake

By Leo Miller. Date Posted: 2/26/2026.

Key Points

- Axon shares surged after Q4 earnings, snapping a months-long selloff that had cut the stock roughly in half from its all-time high.

- The broader SaaS panic dragged Axon down alongside pure software names, but the company's hardware-integrated model may make that comparison a poor one.

- Analysts still see meaningful upside even after trimming their price targets post-report.

- Special Report: [Sponsorship-Ad-6-Format3]

After being battered in the second half of 2025 and early 2026, shares of defense company Axon Enterprise (NASDAQ: AXON) staged a sharp recovery. Following its Q4 financial results on Feb. 24, Axon shares jumped nearly 18% the next trading day.

Axon hit an all-time high closing price near $871 last August; before the recent report, the stock had fallen roughly 50% from that peak.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Even after the recent spike, Wall Street analysts remain broadly bullish on the company.

So, what drove Axon's steep sell-off, and are the concerns about the company justified?

Axon's Sky-High P/E, SaaS Fears Came Home to Roost

Axon's forward price-to-earnings (P/E) ratio peaked near 130 in August, and that lofty valuation made the stock vulnerable to a pullback. The company was also swept up in the 2026 "SaaSpocalypse," which accelerated the decline.

Before the latest release, Axon shares were down more than 20% in 2026, and some of the stock's largest single-day drops coincided with broad sell-offs across the software sector. That pattern suggests investors were indiscriminately selling software-related names rather than assessing AI-disruption risk on a case-by-case basis.

Why Axon's Hardware-to-Software Flywheel Limits AI Risk

Axon benefits from a simple reality: law enforcement relies on physical intervention. AI can't physically restrain or arrest someone, which reduces disruption risk for Axon's primary customers — police and other public-safety agencies.

Axon does have a substantial software business that could theoretically face AI competition. But hardware remains central to its strategy. Consider the product that put Axon on the map: Tasers. Those are physical devices the company has developed for decades — something an AI startup can't replace with "vibe-coding."

Taser sales grew 32% in Q4 2025 and accounted for about one-third of the company's full-year revenue, keeping a large portion of Axon's business relatively insulated from AI-driven substitution.

More importantly, Axon's software and hardware are tightly integrated. Its body cameras capture video that feeds directly into Axon's digital evidence management platform, creating recurring subscription revenue. Many of Axon's software offerings depend on the data those cameras produce.

For example, Draft One automatically generates an initial draft of officers' incident reports from body-camera audio, saving time and allowing officers to focus on prevention and investigation rather than paperwork.

To displace Axon's software stack, a competitor would likely need to replace its body-camera ecosystem as well — a costly, disruptive undertaking for agencies that have already invested in Axon's systems, training and chain-of-evidence processes. Established trust and the operational risks of switching make that a tall order.

As Axon accumulates more device data, its software should only improve, giving the company a growing advantage over potential entrants.

Analysts See Meaningful Upside After Strong Results

Axon's latest results reinforced the strength of its model. The company beat sales and adjusted earnings-per-share expectations, reporting revenue growth of 39%. Future contracted bookings rose 43% to $14.4 billion — the value of signed contracts yet to be fulfilled — a sizable backlog versus the $2.8 billion in revenue Axon generated in 2025.

Axon also posted a net revenue retention rate of 125%, meaning existing customers increased their spending by 25% year over year — a signal that Axon's products are delivering growing value.

By 2028, Axon is targeting revenue of $6 billion, which implies roughly 29% annual growth from 2025. The company also aims to expand adjusted EBITDA margins by 250 basis points to 28%.

The MarketBeat consensus price target for Axon sits near $763, implying more than 45% upside. After the earnings release, analysts lowered some targets; the average of those updated targets is near $654, which still implies roughly 25% upside. Those downward adjustments largely reflect recent price weakness rather than a negative read on the report itself.

Overall, Axon's near-term outlook looks constructive, and fears that AI will rapidly displace its core business appear overstated.

MCD and TXRH: 2 Low-Risk Restaurant Stocks With Upside

Submitted by Dan Schmidt. Article Posted: 2/17/2026.

Key Points

- The restaurant industry has become a key indicator for the K-shaped economy.

- Winners and losers are beginning to emerge based on the perceived value they offer to both higher-end and lower-end customers.

- McDonald's and Texas Roadhouse continue to grow comps despite the tough environment thanks to their value-oriented focus that keeps diners coming back.

- Special Report: [Sponsorship-Ad-6-Format3]

The restaurant sector has often been at the forefront of the debate on the K-shaped economy. While consumer sentiment continues to diverge from actual consumer behavior (especially in the retail sector), the food service industry quickly reveals those divergent trends. The upper end of the 'K' continues to indulge, while more cost-conscious consumers at the bottom are searching for value to stretch their dollars.

In that environment, two restaurant chains are standing out for different reasons. The numbers speak for themselves: McDonald’s Corp. (NYSE: MCD) and Texas Roadhouse Inc. (NASDAQ: TXRH) are growing comparable sales and gaining market share. Below, we explain why each has thrived in a challenging dining landscape and why their stocks could outperform the restaurant industry this year.

McDonald's Continues to Dominate the Fast Food Market

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Recent earnings reports from McDonald's and Wendy’s Co. (NASDAQ: WEN) highlighted the growing separation among fast-food players.

McDonald’s reported Q4 2025 results last week, beating both EPS and revenue expectations with 9.7% year-over-year (YOY) sales growth.

Global same-store sales exceeded forecasts with 5.7% YOY growth, including 6.8% growth in the United States. By contrast, Wendy’s Q4 2025 report showed a 5.5% YOY revenue decline and an 11.3% drop in U.S. same-store sales. How has McDonald’s achieved nearly 7% U.S. sales growth while other QSRs struggle?

Value. The company projects operating margins above 40% in 2026, which supports its Value Leadership strategy.

Rather than relying on limited-time promotions, McDonald’s has made value a core offering. Its Value Menu 2.0 is effectively permanent: Extra Value Meals were reintroduced last September, and earlier this year the company launched the McValue platform, featuring $5 Meal Deals and Buy One, Get One for $1 offers. The Grinch Meal holiday promotion produced the biggest single-day sales figure in the company’s history.

McDonald’s app—about 200 million active users—drives repeat visits, and a marketing focus on chicken items like the McCrispy cushions the impact of beef-price inflation. The company also plans to open another 2,600 stores this year, while some competitors like Wendy’s are closing underperforming locations.

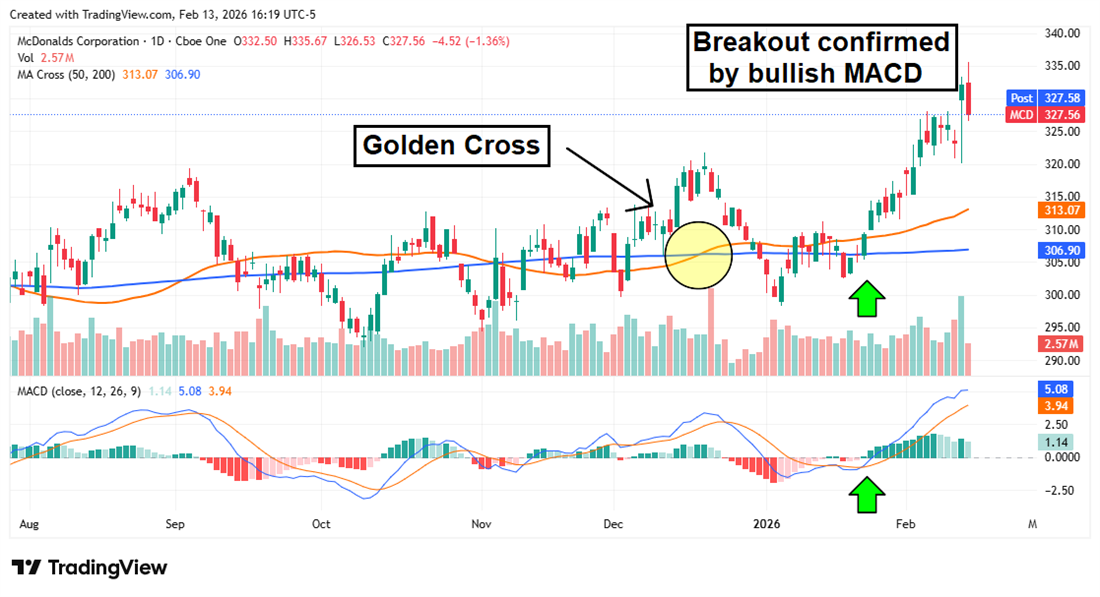

MCD’s breakout started before last week’s earnings. A bullish crossover in the Moving Average Convergence Divergence (MACD) indicator coincided with the stock price moving above the 50-day and 200-day simple moving averages (SMAs), signaling strong upward momentum. If low-income consumers continue to trade down for value, McDonald’s is well-positioned to keep growing sales, with both fundamental and technical catalysts in 2026.

Texas Roadhouse Grows Market Share Despite Commodity Headwinds

Soaring beef prices have clouded Texas Roadhouse’s outlook for much of the past year. Beef prices have risen faster than inflation since the COVID-19 pandemic, and the surge over the last two years has unnerved restaurant owners and investors alike.

The increase is driven in part by cattle shortages that pushed live cow and steer prices to record levels, a situation likely to persist into 2027.

Despite this headwind, Texas Roadhouse continues to grow same-store sales faster than many casual-dining peers.

The company’s barbell strategy offers value to budget-conscious customers while providing premium steaks and upcharge options for diners willing to splurge.

In its Q3 2025 report, Texas Roadhouse posted comps of 6.1% and nearly 13% YOY revenue growth despite a 224 basis point increase in food and beverage costs. Management raised menu prices by only 1.7%, accepting some margin pressure to preserve perceived value and traffic.

Customer experience is a central reason for the company’s resilience. Traffic durability matters for restaurants that rely on repeat business. Large portions, attentive servers, efficient kitchens, and a range of add-ons create a special-night-out feel without an excessive bill. Customers commonly report that Texas Roadhouse is "worth it" for date nights and family meals because the value and experience meet expectations.

TXRH’s performance so far in 2026 suggests the doldrums of 2025 may be fading. The stock started the year with an 11-day winning streak that pushed it through the long-standing 200-day SMA resistance. That streak was followed by consolidation, during which the Relative Strength Index (RSI) cooled to more neutral levels while the 50-day and 200-day SMAs converged.

With a Golden Cross appearing imminent, the 50-day SMA could act as support for a renewed rally. That level has already been tested and held, and the share price is once again approaching the 50-day moving average—an attractive entry point for new investors. A near-term catalyst: TXRH reports its Q4 2025 results after the market close on Feb. 19.

This email message is a sponsored message sent on behalf of Golden Portfolio, a third-party advertiser of InsiderTrades.com and MarketBeat.

If you have questions about your subscription, don't hesitate to contact our U.S. based support team at contact@marketbeat.com.

If you no longer wish to receive email from InsiderTrades.com, you can unsubscribe.

Copyright 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 North Reid Place, Suite 620, Sioux Falls, South Dakota 57103-7078. United States..

No comments:

Post a Comment