Warren Buffett is sitting on $325 billion in cash – his largest hoard ever.

Not because he wants to – but because he can’t find value in the usual places.

Now, as US government spending spirals out of control, Buffett knows he’s losing billions of dollars to inflation.

That’s why I predict Buffett’s next investment will catch millions of people off guard.

It’s not another bank… railroad company… or more shares of Apple.

It’s a gold company. How do I know?

Because the math doesn’t lie:

You can buy the average gold developer for $30 and get back $13 a year —

That’s a 43% ROI annually.

Over 10 years, that’s $130 on a $30 investment.

Tell me where else Buffett can get that.

But there’s one specific miner Buffett likes best:

- It’s the best-managed major gold miner in the industry…

- Has massive cash flow…

- Is trading at a deep discount to fair value…

- Positioned at the heart of Trump’s new mining push…

Don’t wait for Buffett to reveal his position in his 13F filing on February 17th…

Right now, you have the chance to front-run the greatest investor of all time. Go here and I’ll give you the name and ticker – along with details on my top four small miners.

To your wealth,

Garrett Goggin, CFA, CMT

Chief Analyst & Founder, Golden Portfolio

P.S. A lot of investors write in to tell me how much they’ve made in Bitcoin. My reply? Good for you. First off, gold investing is cyclical. You really only want to own gold at one specific time in the cycle. That time is now. Second, the world’s governments are not buying Bitcoin. They’re betting on gold. All of them. Bitcoin (does anyone really know for sure the US government didn’t create it?) will be a good bet… until it isn’t. It may end up doing great. Or it may be eclipsed by any number of tech developments.

Meanwhile, gold will continue to do what it’s done for almost 6,000 years of recorded human history: Protect wealth through chaos. Go here if you want the name and ticker of Buffett’s likely gold play… and details on my top four miners

3 Under-the-Radar Earnings Surprises Could Signal a New Trend

Author: Dan Schmidt. Publication Date: 2/17/2026.

Key Points

- Earnings season is starting to wrap up as more than 75% of S&P 500 companies have reported their latest results.

- Earnings and revenue beats are in line with historical averages, but divergences beneath the surface are creating different winners and losers than 2025's market.

- These three stocks typically fly under the earnings radar in their respective industries, but their positive recent reports deserve a closer look.

- Special Report: [Sponsorship-Ad-6-Format3]

Earnings season is winding down, and more than three-quarters of the companies in the S&P 500 have reported their latest results. According to FactSet, roughly 74% of firms reporting so far have beaten analysts' EPS estimates, and 73% have beaten revenue estimates.

While these overall numbers sit near the five- and ten-year averages, the dispersion between winners and losers kept aggregate earnings growth roughly flat for the period. Many of last year's success stories have underperformed in 2026, while some laggards have posted parabolic gains. Three companies whose earnings reports don't typically make headlines still warrant attention for the strength of their most recent results. Are these one-time standouts or signs of a larger trend?

Applied Materials: Semiconductor Demand and Guidance Power Double-Digit Gains

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

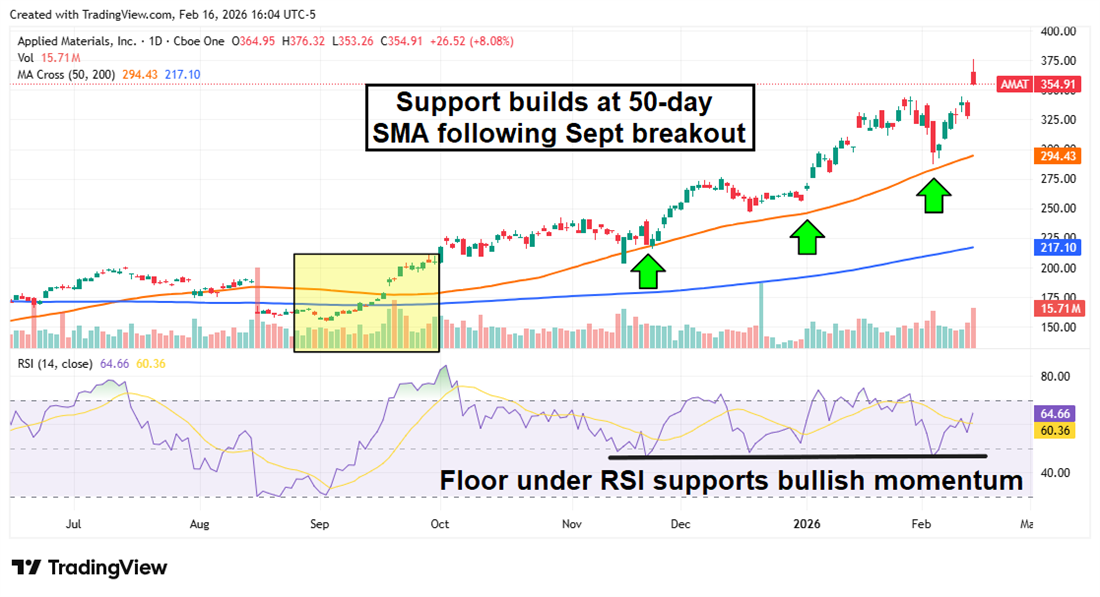

Applied Materials Inc. (NASDAQ: AMAT) is probably the most "on-the-radar" stock here, with a $280 billion market cap and about $28 billion in annual sales. As a picks-and-shovels play in semiconductors, Applied Materials usually reports in the background while NVIDIA Corp. (NASDAQ: NVDA) or Alphabet Inc. (NASDAQ: GOOGL) grab headlines. This most recent report, however, deserves attention: AMAT shares jumped 12% following the release, driven by upbeat guidance and strong equipment demand.

The company reported its fiscal Q1 2026 results on Feb. 12 and beat analysts' estimates on both EPS and revenue, with earnings topping expectations by 7%. The news that truly excited investors came on the conference call, when CEO Gary Dickerson projected 20% sales growth in calendar year 2026 — a figure that exceeded even the most optimistic analyst projections. Most of the company's revenue comes from its Semiconductor Systems division, which sells equipment used in flash memory, logic manufacturing, transistors, DRAM and more. Dickerson forecasted Q2 revenue of about $7.65 billion, with continued rapid growth in the Applied Global Services business.

The target price increases arrived quickly after the optimistic report, and Applied Materials received upgrades from Hold to Buy at Summit Insights and KGI Securities. The average price target among the 17 analysts who revised estimates is now $435, implying nearly 20% upside from current levels.

AMAT shares have trended higher since September, when the price crossed both the 50-day and 200-day simple moving averages (SMAs). The 50-day SMA has acted as solid support on dips. The Relative Strength Index (RSI) remains below the overbought threshold of 70 despite the earnings bump, suggesting the rally may have staying power.

Advance Auto Parts: Turnaround Efforts Start to Show Results

Advance Auto Parts Inc. (NYSE: AAP) may finally be returning to investability after losing more than 50% of its value over the past five years. The last 12 months were particularly tumultuous for the company (and the automotive sector), as the company reported a loss of more than $10 per share in Q4 2024 and then faced tariff headwinds during the presidential transition. CEO Shane O'Kelly refocused the business on cutting costs and getting "back to basics," and those efforts appear to be paying off.

Advance Auto Parts' Q4 2025 results surprised to the upside. Revenue slightly exceeded estimates ($1.97 billion vs. $1.95 billion expected), while EPS of $0.86 was more than double the projected figure. Same-store sales grew 1% for the year, and management closed 17 underperforming locations. The 2026 outlook also helped the stock: management expects 1–2% comps, a roughly 45% gross margin, EPS between $2.40 and $3.10, and about $100 million in free cash flow generation.

Some profit-taking followed the release because the stock had already climbed nearly 50% year-to-date. Still, the technical picture looks constructive: the share price cleared both the 50-day and 200-day SMAs, and the Moving Average Convergence Divergence (MACD) shows bullish momentum with the MACD line crossing above its signal line.

Rivian: Narrowing Losses Provide 2026 Catalysts

Friday the 13th was anything but scary for Rivian Automotive Inc. (NASDAQ: RIVN). The company beat top- and bottom-line estimates in its Q4 2025 report. Year-over-year (YoY) revenue declined about 25% due to the expiration of EV tax credits, but sales still outpaced expectations and the company narrowed its loss to $0.66 per share.

The improved results were driven by a $5,500 increase in average vehicle selling price and a roughly $9,500 reduction in average cost of vehicles sold. The quarter marked the company's first year of gross profit, and the more affordable midsize R2 model is slated to begin deliveries in Q2 2026. Rivian expects to sell between 62,000 and 67,000 vehicles in 2026, with the lower end representing about a 47% increase over 2025.

RIVN shares rose about 20% in a volatile session after the report, though they pulled back from the initial high. The stock now sits near the 50-day SMA, which had acted as support when shares rallied late in 2025. A bullish MACD crossover points to a favorable trend, but sustaining momentum likely depends on a successful R2 rollout and continued improvements in unit economics.

REITs Set for a 2026 Rebound? 7 Top Picks as Rate Cuts Approach

Authored by Bridget Bennett. Originally Published: 2/19/2026.

Key Points

- REITs could be setting up for a 2026 comeback as falling rates flip the macro backdrop that crushed the sector in 2025, with Brad Thomas saying the “REIT rally [is] finally underway in 2026.”

- Five “sleep well at night” picks—Realty Income, Equinix, Public Storage, Equity LifeStyle, and EastGroup—combine durable moats, solid balance sheets, and sector-specific tailwinds.

- Two higher-risk ideas, Americold and Healthpeak, offer deep-value upside tied to execution and catalysts like cost resets, activism, and a planned senior-housing spin-off.

- Special Report: [Sponsorship-Ad-6-Format3]

Real Estate Investment Trusts—or REITs—were written off in 2025. After two straight years of underperformance, the group became one of the market's most avoided corners—largely because rising interest rates are kryptonite for a sector built on leverage and reliant on capital markets.

In a recent conversation with Brad Thomas of Wide Moat Research, the tone was noticeably different. The setup for 2026 is starting to look like the mirror image of what punished REIT investors in 2024 and 2025.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

As Thomas put it, "So now that we're seeing this rates decline… we're seeing the REIT rally finally underway in 2026."

That's already showing up on the scoreboard. Certain property sectors are leading early in the year—farmland REITs are up roughly 24% year to date, data centers around 22%, net lease about 15%, and self-storage about 14%. The point isn't that everything is back. It's that the rotation is beginning, and investors who wait for an "all clear" often wind up paying higher multiples for the same cash flows.

Thomas shared seven REITs he likes most for 2026. The first five fall into the "sleep well at night" bucket—steady businesses with durable moats. The final two are higher-risk ideas with bigger rebound potential if their catalysts play out.

Realty Income: The Monthly Dividend Machine With Scale to Spare

Realty Income (NYSE: O) is one of the most recognizable names in REIT land—and for Thomas it's a foundational holding in net lease.

The company owns more than 15,500 freestanding properties across all 50 states and Europe, and it collects rent from roughly 1,600 customers across 92 industries. Tenants include familiar brands like 7-Eleven, Dollar General (NYSE: DG), Walgreens and FedEx (NYSE: FDX), which reinforces the stability investors seek in a core REIT holding.

Scale matters, but so does balance-sheet strength. Realty Income carries an A credit rating and has increased its dividend for 27 consecutive years, making it a Dividend Aristocrat. That streak spans the Global Financial Crisis and COVID-19.

Even after a strong start to 2026, Thomas still sees value. Shares trade near 15.3x price-to-AFFO (adjusted funds from operations), below the company's longer-term average around 17x, with a dividend yield near 4.9%.

Equinix: The Data Center REIT Where the Network Is the Moat

When the conversation shifted to growth, Thomas went straight to data centers—and specifically Equinix (NASDAQ: EQIX), one of the sector's dominant global landlords.

Equinix operates 273 data centers across 36 countries and 77 markets. The key advantage, Thomas emphasized, isn't just the real estate—it's the ecosystem inside the facilities.

"The real moat is not the building… it's the network inside of that building," he said.

That network effect creates stickiness—moving equipment is expensive, and connectivity relationships aren't easily replicated. It also supports pricing power in major metro markets where demand remains intense. Equinix recently delivered a 10% dividend increase, and management is guiding to strong AI-fueled growth.

The balance sheet is solid (BBB+), leverage is manageable, and shares trade around 24x AFFO—slightly below the company's typical range. The yield is lower at roughly 2.6%, but the growth runway is longer.

Public Storage: The Sticky Self-Storage Giant With Pricing Power

Self-storage is one of those property types that tends to surprise investors—until they've used it. Thomas described it as "sticky," and it's easy to see why.

Public Storage (NYSE: PSA) is the category leader with approximately 3,500 U.S. facilities and a 35% stake in European operator Shurgard. The industry remains fragmented, giving Public Storage ample room to consolidate over time.

The company's edge isn't only scale. Technology has become a competitive weapon in self-storage, and Public Storage's digital operating platform helps optimize pricing and operations at the local level.

Financially, it's built to endure: A-rated credit, strong liquidity, and substantial retained cash flow. Shares trade near 19x AFFO versus a historical average of 22x.

The yield sits around 4%, with expectations that declining rates could improve the broader return profile.

Equity LifeStyle Properties: A "Silver Tsunami" Play in Manufactured Housing and RV Resorts

Equity LifeStyle Properties (NYSE: ELS) isn't the first real estate name many investors think of—and that's part of what makes it interesting.

The company owns and operates 455 properties across 35 states and Canada, focused on manufactured housing communities, RV resorts, campgrounds and marinas. Many are in retirement and vacation destinations, and a large portion of its manufactured housing portfolio is age-qualified.

Thomas framed ELS as a beneficiary of the "silver tsunami"—the demographic wave created as baby boomers age into retirement.

With demand rising and supply constrained in key Sunbelt markets, ELS has been able to leverage pricing power and maintain durable occupancy.

The company recently raised its dividend by 5.3% and has increased payouts for 22 consecutive years. The dividend yield is around 3.2%, and the setup implies mid-teens total return potential if growth and valuation cooperate.

EastGroup Properties: Sunbelt Flex Warehouses Built for Growth

Industrial real estate has been a market favorite for years, but EastGroup Properties (NYSE: EGP) plays a slightly different game than the mega-warehouse landlords.

EastGroup targets "flex" distribution properties—typically 20,000 to 100,000 square feet—in fast-growing Sunbelt markets such as Texas, Florida, Arizona and North Carolina. That niche serves expanding regional businesses that may need to scale space over time.

Operational metrics have been strong: occupancy around 96.5%, solid same-store NOI growth, and funds from operations up 8.8% in the latest quarter. Leverage is low, with debt to total market cap around 14.7%.

Shares trade near 27x AFFO versus a historical norm around 30x.

With analysts projecting growth accelerating into 2027 and 2028, EastGroup offers a blend of quality and upside that fits squarely in a "SWAN" framework.

Americold Realty Trust: A Deep-Value Cold Storage Turnaround With a Big Yield

After covering the high-quality core names, Thomas pivoted to two beaten-down ideas where the payoff depends more on execution and catalysts.

Americold Realty Trust (NYSE: COLD) is a cold-storage REIT operating temperature-controlled warehouses across North America, Europe, Asia-Pacific and South America. The company has about 230 facilities and roughly 1.5 billion refrigerated cubic feet of storage capacity.

Its customer list includes household names like Walmart (NASDAQ: WMT), Conagra (NYSE: CAG), Kraft Heinz (NASDAQ: KHC), General Mills (NYSE: GIS) and Smithfield (NASDAQ: SFD). In other words: demand isn't the issue.

The stock is down sharply because investors have been skeptical about the business's cyclicality and the service component layered on top of the real estate.

Now the story is shifting. A new CEO is in place, an activist investor has pushed for a review of strategic alternatives, and management is exploring asset sales and cost reductions. Thomas pointed to potential SG&A and indirect cost savings in 2026.

The valuation reflects that fear: shares trade around 8.9x AFFO versus a historical multiple above 25x, and the dividend yield is roughly 6.65% with a payout ratio near 65%. It's not risk-free—but if execution improves, the rebound potential is meaningful.

Healthpeak Properties: A Healthcare REIT Catalyst With a Spin-Off on Deck

Healthpeak Properties (NYSE: DOC) is the other higher-risk idea Thomas highlighted, and the catalyst is more corporate-structure than macro.

Healthpeak owns a mix of outpatient medical office buildings, life-science properties and senior housing.

The company recently announced plans to spin off its senior housing assets into a new REIT (Janus Living), with Healthpeak retaining a majority ownership stake and the remaining shares expected to trade publicly.

The logic is straightforward: pure-play senior housing REITs have commanded premium multiples, while Healthpeak's blended portfolio has not. A spinoff could help the market value each segment more appropriately. The complication is life science.

Industry overbuilding coming out of COVID and reduced venture-capital funding have pressured occupancy.

Healthpeak did see life-science occupancy decline in the most recent quarter, but management expects leasing momentum to improve later in 2026, with a meaningful pipeline of space being marketed.

Shares trade around 8.9x AFFO and yield roughly 7.2%, signaling that plenty of risk is already priced in. If the spin-off unlocks value and life science stabilizes, the upside case becomes easier to underwrite.

The 2026 REIT Playbook From Brad Thomas

Thomas's list isn't built around chasing what's already run up. It's based on a simple premise: when the rate environment changes, REIT leadership changes with it—and investors can either position early, or compete later at higher valuations.

The five core names offer stability, balance-sheet strength and durable moats. The final two are discounted for a reason but come with identifiable catalysts that could reshape their return profiles if management delivers.

If the rate-cut cycle continues to unfold, REITs may not stay a "forgotten" sector for long.

This email content is a paid advertisement provided by Golden Portfolio, a third-party advertiser of InsiderTrades.com and MarketBeat.

If you have questions or concerns about your subscription, please don't hesitate to email MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from InsiderTrades.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 North Reid Place #620, Sioux Falls, S.D. 57103-7078. USA..

No comments:

Post a Comment