Axis Capital stock shows strong underwriting and specialty insurance growth, but investors must weigh catastrophe risk and competitive... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

|

|

| Written by Peter Frank

Axis Capital (NYSE: AXS) is not a household name—unless you insure against cyber, marine, aviation, political, or professional risks. But this specialty insurer and reinsurer might be worth considering for your portfolio. After years of repositioning itself around higher-margin lines of business, the company’s efforts are showing up in its numbers. Axis ended last year with record premiums, record underwriting income, and a strong annualized return on average common equity of 19.4%. At the same time, its stock has flirted with all-time highs. Still, it’s not a low-risk holding. Like many insurers, one active hurricane season could erase much of its gains, and the stock’s run-up leaves little room for disappointment. Results Reflect Disciplined Underwriting and GrowthFor Axis, 2025 was a year when things went right. The company earned $979 million in net income, or $12.35 per share, while operating income hit $1 billion. That represented a 10% increase in revenue from the previous year, though net income declined year-over-year after a large income tax expense. For the fourth quarter, the company reported earnings per share of $3.25, well above analyst expectations of $2.97. Quarterly revenue also jumped higher than analysts had expected. Importantly, the company’s combined ratio for the year, a key measure of profitability and strong underwriting in the insurance industry, came in at 89.8%, meaning it spent less than 90 cents on claims and expenses for every dollar it brought in. That figure was the best since 2010. Book value per share climbed 18.3% to $77.20. The numbers are impressive for both financial results and as a signal that the company has grown more disciplined. The insurance segment, which now accounts for three-quarters of its business, posted record gross premiums of $7.2 billion, up 9% from the prior year. Underwriting income in this segment jumped 40% to $597 million, so Axis is writing more business as well as better business. Shift to Specialty Insurance Is Driving ProfitabilityA decade ago, Axis was better known as a reinsurer that insures other insurance companies. Since then, the company has been shifting its focus toward specialty insurance, covering harder-to-price risks in areas like cyber, marine, aviation, and professional liability. Today, its insurance segment has grown from 63% of its overall business to 74%. The success is evident as the insurance segment's combined ratio improved to 86% in 2025, three points better than in 2024. Meanwhile, the company is putting capital to work for shareholders. Axis said it returned $1 billion to shareholders last year through dividends and stock repurchases, and in February, the company declared its regular quarterly dividend and authorized a new $300 million share repurchase program. Analysts have taken notice. The stock now carries a consensus Moderate Buy rating, with an average 12-month price target of $123.70, well above its recent trading range around $100. Its price-to-earnings ratio of about 8X also compares favorably to its peers. Of the 12 analysts setting price targets, nine assign the stock a Buy rating while three assign it a Hold rating. Gross premiums are expected to grow in the mid to high single digits this year. Earnings are expected to grow more than 10%. Catastrophe Risk and Competition Remain ThreatsNo matter how bright the outlook, insurance can be a risky business. Axis covers catastrophe-exposed property, reinsurance portfolios, and specialty casualty lines. An overly strong year of hurricanes or unexpected disasters can erase a year's worth of carefully built profits. That’s simply the nature of the insurance business. Competition adds another layer of risk. When insurance lines are profitable, new capital can compete for the same business, pressuring rates. Axis faces rivals such as RenaissanceRe (NYSE: RNR), Everest Group (NYSE: EG), and Arch Capital Group (NASDAQ: ACGL). If pricing softens and margins compress, the current returns on equity might not hold. Balancing Strong Performance With Inherent VolatilityGiven the market in which Axis operates, it isn't necessarily a company that investors choose and forget about. Specialty insurance is unpredictable. A stumble on underwriting losses, a hit to investment income, or adjusted guidance could pressure a stock that has already had a big run. And Axis is not a high-dividend player, with its current yield under 2%. Still, the company’s stock price has nearly doubled in five years. Axis has an improving underwriting quality, strong book value growth, a still-reasonable valuation at roughly 1.3X book, with analyst consensus pointing at higher prices. For many retail investors, the company could be a strong candidate for a diversified portfolio. It has certainly earned some attention. Just don't forget what kind of company it is.  Read This Story Online Read This Story Online |

Nvidia CEO Jensen Huang says of Elon's latest venture: "What Elon and his team has achieved is singular. It's never been done before."

He revived EVs, revolutionized space, and built the world's largest satellite network. But this AI technology may prove to be the crown jewel of his entire career.

Get the full story on why insiders are calling this his greatest move yet. See the Full Story

|

| Written by Thomas Hughes

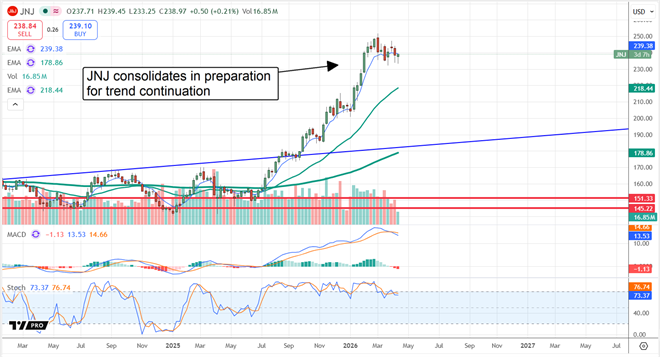

Johnson & Johnson’s (NYSE: JNJ) price action entered consolidation in early March. While it may continue moving sideways or even pull back further, those moves are unlikely, given a convergence of factors. Price action and accelerating growth suggest the March pullback is a continuation signal and a buying opportunity likely to lead to much higher prices down the road. Among the highlights from the recent Q1 earnings release were numerous approvals and pipeline updates, which led management to increase guidance and affirm a double-digit revenue growth pace by the decade’s end. Technically speaking, JNJ’s stock price consolidation bears the hallmarks of a Bull Flag or Pennant formation. These formations mark stopping points within a rally, and bring easily identifiable targets into play when confirmed. Confirmation is primarily through price action; it includes the setting of new highs and subsequent testing of support following the breakout.

The critical resistance point for this market is $250 as of mid-April. If broken and confirmed as support, the initial target for upside advance is about $35, or the magnitude of the rally preceding the pattern. Assuming the company continues executing its strategy and building its revenue base, the bull-case targets equalling the percentage gain of the move preceding the pattern, worth about 17% from the breakout point, come into play. That could put this market in the $290 range within a few months of setting the new high. Johnson & Johnson Pulls Back Following Hot Quarter and Raised GuidanceJohnson & Johnson had a solid quarter, with revenue growing 9.9% driven by organic gains, acquisitions, and foreign exchange tailwinds. The revenue outpaced MarketBeat’s consensus by more than 190 basis points, with strength in both core segments. Innovative Medicine grew by 11.2%, underpinned by strength in the oncology segment, while Med Tech grew at a slower 7.7% rate. Regionally, sales in the United States were solid at up 8.3%, led by a stronger 11.9% gain internationally. Margin and guidance were also bullish, albeit insufficient to spark a rally on their own. The company’s margin compressed significantly due to patent expiration and increased competition for Stellara. The good news is that the impact was only slightly worse than expected and offset by revenue strength. The bad news is that earnings contracted. The bottom line is that $2.70 in adjusted earnings per share is down 2.5% compared to last year, but outpaced the consensus by 2 cents (75 bps), trailing the top-line strength by more than 100 bps. Guidance was tepid, despite the increase, compared to analyst trends. The company raised its fiscal year 2026 forecast to align with the consensus estimate, expecting earnings growth of 7% at the midpoint. The opportunity for investors is that accelerating growth could lead to outperformance in upcoming quarters, and that new approvals could lead to improving margins as the company’s pipeline is monetized. Institutions and Analysts Underpin JNJ’s 2026 Stock Price IncreaseInstitutional activity is noteworthy, as it spiked in Q1, aligning with the stock price increase that pushed it to new highs. With them owning nearly 70% of the stock and the outlook for accelerating business, it is unlikely they will revert to distribution soon, instead sticking to accumulation as the story plays out. Analyst trends have also been bullish, with them lifting price targets and sentiment ratings ahead of the report. As it stands, the group rates JNJ as a Moderate Buy with 67% Buy-side bias, no Sell ratings are logged, and the consensus price target is trending higher. Offering only a slim upside in April, the high-end analyst price target suggests 20% upside is available, aligning with the technical $290 target. Short interest is not a factor in this market, as it remains below 1% and is unlikely to increase. Dividends are among the reasons sell-side interest is so strong. The company’s 2% yield is reliable, grows annually, and is backed up by a healthy balance sheet. The company uses debt to fund cash and capital needs, but maintains a healthy profile and sufficient free cash flow to sustain distributions and growth. As it stands, JNJ has increased its payment for more than 60 years and has the capacity to continue the trend for the foreseeable future. The biggest risks for JNJ are ongoing patent expirations and their impact on revenue and margin. However, the company’s pipeline is robust, with leading candidates expected to drive 5% to 7% in annualized revenue growth over the next four to five years. The company is also focusing on Med Tech, with the Cardiovascular unit specifically driving growth through several platforms. Surgical Robotics is another focus, with the OTTAVA system expected to receive approval by late this year. Surgical Robotics is a fast-growing industry, expected to quadruple in size over the coming decade. Read This Story Online |

There are currently 200 paper claims for every 1 physical ounce of gold in the vaults - and a 90-year-old law set to 'call the bluff' on May 29th.

Dylan Jovine of Behind the Markets has identified a company sitting on $431 billion worth of metal that trades for a fraction of that value today. He calls it the 287-to-1 gap the market is about to correct. Run the numbers yourself - get the ticker and full analysis here

|

| Written by Jeffrey Neal Johnson

A seismic event is shaking the foundations of the artificial intelligence (AI) hierarchy. For months, the consensus on Wall Street was that the AI race was Microsoft’s (NASDAQ: MSFT) to lose. Now, that assumption is being shattered. Reports of a deep fracture in the critical Microsoft-OpenAI alliance are not just industry gossip; they are a public signal of a potential power shift in the multi-trillion-dollar cloud market. A bombshell internal memo suggests that OpenAI's leadership feels constrained by its partnership with Microsoft, leading it to explore Amazon's (NASDAQ: AMZN) cloud services to gain greater reach and flexibility. This development has immediate and significant implications for investors. It challenges the long-held belief that Microsoft had an unbreachable moat in the generative AI race, a narrative that has propped up its valuation. This shift in dynamics is creating a clear investment divergence between the two tech titans, and the market is only just beginning to price in the consequences. The unfolding situation reveals a narrative-shattering story about the true state of the AI cloud wars and which company is better positioned for the road ahead. The $2 Trillion Problem: Microsoft's Single Point of FailureMicrosoft's entire AI strategy has been built on its exclusive access to OpenAI's technology. This created a powerful narrative that propelled its stock to new heights, but that single point of reliance has now become a critical vulnerability. The market's reaction has been swift and unforgiving, suggesting investors are re-evaluating the risks of a strategy tied so closely to a single partner, especially one that now appears to be exploring its options. The numbers tell a compelling story. Since the beginning of the year, Microsoft's stock has declined about 20%, a stark contrast to the broader market. This isn't a simple market correction; it appears to be a direct reflection of waning confidence in Microsoft's AI-driven growth story. This sustained selling pressure is confirmed by Tradesmith technical indicators, which show the stock has been in a Red Zone for over two months, a tangible sign of market doubt. In response, Microsoft's board has initiated a massive $60 billion stock repurchase program. In good times, a buyback signals confidence. In this context, however, it can be viewed as a necessary defensive maneuver. It uses company cash to buy its own shares, which helps support the stock price and manage earnings-per-share calculations at a time when its core growth narrative is facing serious headwinds. The fundamental problem remains: the potential loss of OpenAI's total allegiance exposes a key risk, and Microsoft's perceived moat appears to be evaporating. How Amazon Is Capitalizing on Microsoft's CrisisWhile Microsoft grapples with its partnership crisis, Amazon is emerging as the conflict's silent and decisive winner. The news that OpenAI is looking to Amazon Web Services (AWS) is the ultimate market validation of the platform's technological superiority and open-ecosystem strategy. It cements AWS's role as the indispensable infrastructure provider for the entire AI revolution. For investors, this is a powerful signal. When the world's premier AI company seeks you out to solve its biggest scaling challenges, it's a powerful endorsement that resonates with enterprise customers worldwide. This helps explain the stark divergence in stock performance. In sharp contrast to Microsoft's volatility, Amazon's stock price has posted a steady 7% year-to-date gain and maintains a healthy Green Zone technical status. This positions Amazon as the stable harbor for investors seeking AI exposure without the associated partnership drama. This development reinforces the core of Amazon's growth story. AWS is the established market leader in cloud computing and Amazon's primary profit engine. Attracting the most demanding AI workloads ensures its dominance for the next decade. While Amazon's most recent earnings report showed a minor miss of 2 cents per share, the more critical metric was the powerful 13.6% year-over-year revenue growth. This demonstrates the underlying strength of its business, a strength poised to accelerate as it becomes the go-to platform for a more open AI ecosystem. Why the Smart Money Is Choosing AmazonWhen the fog of this AI civil war clears, the strategic victor becomes apparent. The internal conflict at Microsoft has exposed fundamental risks, while simultaneously validating Amazon’s long-term strategy. For investors, the data paints a clear picture: Amazon's durable, diversified, and open-platform approach makes it the more compelling AI infrastructure play for the foreseeable future. A direct look at valuations is revealing. A company's price-to-earnings (P/E) ratio measures its current share price relative to its per-share earnings. A high P/E often indicates that investors expect higher future growth.

Microsoft's P/E of 24 may seem lower and more attractive, but it reflects a company whose primary growth narrative is now in question. Amazon's higher P/E of 34 is more justified, as it signals investor confidence in its strengthening market position and a clearer, more stable path to AI dominance. Analyst price targets also provide insight. While both companies have a Moderate Buy rating, the context is different. The nearly 50% upside for Microsoft reflects how far the stock has fallen and the significant climb it must make to regain investor trust. Amazon's 15% potential upside represents steady, reliable growth from a position of market leadership. The current turmoil is creating a distinct divergence. While Microsoft is a formidable tech giant, the risks tied to its AI strategy are undeniable. Amazon is quietly capitalizing on the chaos, making it the clearer choice for investors looking to bet on the foundational layer of the entire AI ecosystem. The upcoming earnings reports in late April will be the next battleground, and all eyes will be on the cloud revenue growth figures from Azure and AWS. Read This Story Online |

After 220 Executive Orders in a single year, Chief Strategist Ian King believes President Trump is expected to sign his final one on April 30th - with nearly three full years still left in office.

King says details from an inside White House leak point to a major and unexpected announcement. He's breaking down the full story and what it could mean for investors. Read Ian King's full breakdown of the April 30th leak now

|

|

More Stories

|

|

|

No comments:

Post a Comment